EFRAG Previews N-ESRS for Non-EU Groups

EFRAG’s N-ESRS work is moving towards public consultation. The consultation is expected to focus on the content of the standards, the mixed approach, interoperability with IFRS and the internationalisation of EU references.

EFRAG has resumed work on the European Sustainability Reporting Standard for Non-EU Groups (N-ESRS) and launched a call for interest for a field test. Public consultation is expected in the second half of July 2026 and is due to run for 100 days. For non-EU groups with significant EU activity, the immediate task is to assess potential reporting boundaries, the proposed impact-based approach and how existing ISSB reporting may be reused before EFRAG submits its technical advice to the European Commission in January 2027.

The shift is from the full ESRS lens of impacts, risks and opportunities to an impacts-only standard based on simplified ESRS.

Scope and Legal Basis

The legal basis is Article 40a of the Accounting Directive (Directive 2013/34/EU) as modified by Omnibus I Directive (Directive (EU) 2026/470). While Omnibus I significantly narrowed the population of companies expected to report, EFRAG states that the underlying objective remains unchanged: ensuring a level playing field and promoting accountability and transparency regarding the impacts of non-EU companies. The first reports are expected in 2029 for financial year 2028.

The technical detail discussed below comes mainly from EFRAG Secretariat material for the 3 June 2026 SRB public session.

EFRAG estimates that around 1,200 non-EU groups remain in scope, compared with around 10,000 before Omnibus. Before Omnibus, the thresholds were EUR 150 million at group level and EUR 40 million for an EU subsidiary or branch.

The revised criteria are more targeted. They refer to non-EU companies that:

- are not listed on EU regulated markets;

- have EU net turnover above EUR 450 million for two consecutive years; and

- have an EU subsidiary or branch with EU net turnover above EUR 200 million in the previous financial year.

EFRAG also notes that no official list exists. Its preliminary country breakdown points to 350–450 companies from the United States, 150–200 from the United Kingdom, and 100–150 from Switzerland and Japan.

This makes scoping and perimeter-setting a reporting judgement, not just a legal screen. Groups will need a reliable view of EU turnover at group level, the parent’s listing status, the status of EU subsidiaries or branches, and, for any mixed approach, the boundary between global activity and EU-related impacts.

A Narrower Materiality Lens

EFRAG’s current design keeps the ESRS structure: 12 standards in total, including 2 cross-cutting standards and 10 topical standards. The reporting areas also remain familiar: governance, strategy, policies and actions, and metrics and targets. The main edit is to remove financial materiality content, including risks and opportunities, financial effects, resilience and dependencies.

The removal of financial materiality content does not make financial information irrelevant. EFRAG indicates that financial information may still be used where it provides context for understanding impacts.

The value chain also stays in view. EFRAG states that upstream and downstream value chain impacts remain included in the definition of impacts. A non-EU parent therefore cannot treat N-ESRS as a simple EU-operations-only exercise.

Mixed Reporting Depends on Evidence

EFRAG presents three reporting options for companies in Article 40a scope. Under the global N-ESRS approach, impacts would be reported at global level across all topics. Under the mixed N-ESRS approach, climate impacts would remain global, while other topics could be limited to EU-related impacts, subject to conditions and with no final decision yet on exact drafting. The third option is voluntary application of full ESRS by the non-EU parent.

For any mixed approach, EU-related impacts would need to include both customer-based impacts from products and services assumed to be sold or provided in the EU market, and location-based impacts from the undertaking’s activities in the EU. For preparers, the decision is therefore not only whether the group is in scope, but which perimeter can be evidenced.

EFRAG says subsidiaries of a non-EU parent that fall under Article 19a or 29a could benefit from the subsidiary exemption only if the parent applies full ESRS, not N-ESRS.

Field Test as a Preparation Signal

The field test will follow publication of the Exposure Draft and run for 70 days, from mid-July to the end of September. Companies may simulate selected disclosures or the full draft, complete a questionnaire and join follow-up interviews or workshops in October, with EFRAG analysis expected in November.

For preparers, the test points to the controls that will matter early: traceable perimeter decisions, impact data linked to policies, actions, metrics and targets, and controlled cross-references where existing sustainability or financial reporting is reused.

Internationalisation of EU references is also on the consultation agenda. EFRAG is considering expanded provisions in the standards, global references such as ILO where available, and case-by-case use of local legislation. For non-EU groups, this will matter for policy wording, legal mapping and cross-references.

ISSB Reuse Will Be Partial

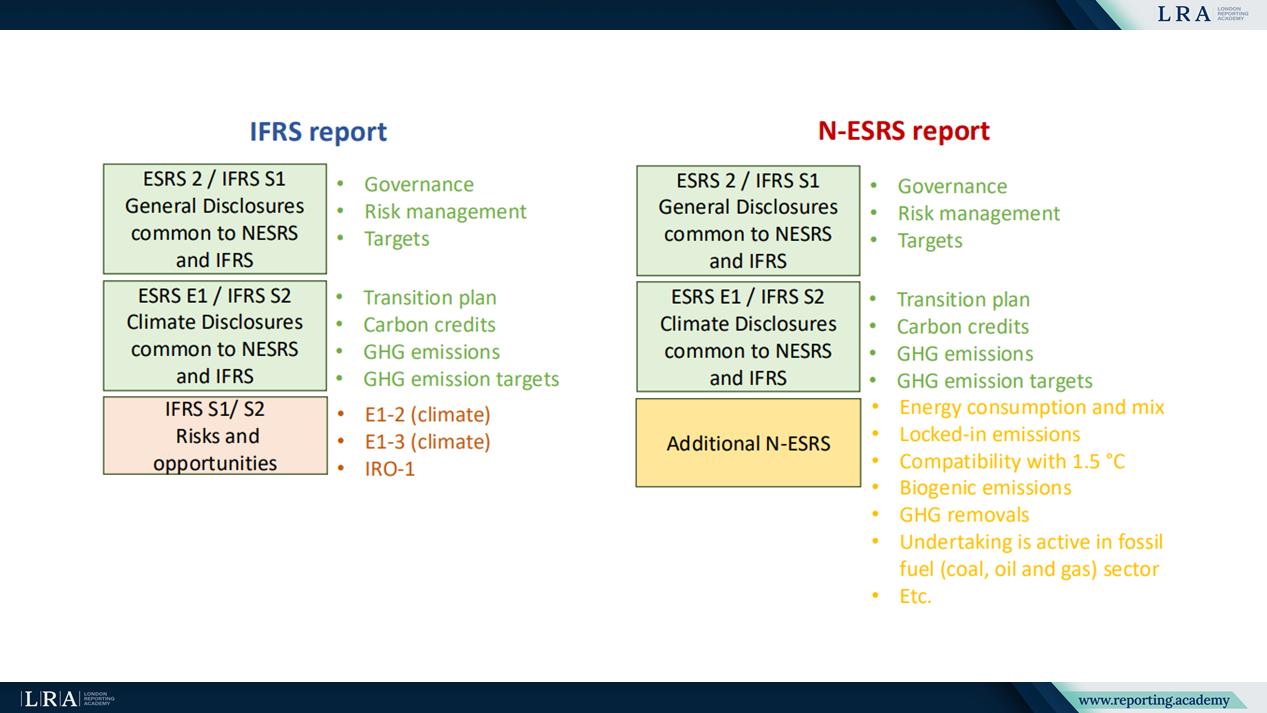

EFRAG treats interoperability with IFRS S1 and IFRS S2 as a workstream and maps common content between ESRS 2 and IFRS S1, and between ESRS E1 and IFRS S2. The shared areas include governance, risk management, transition plans, carbon credits, greenhouse gas emissions and targets.

Source: EFRAG SRB Public Session Presentation on N-ESRS

The reuse case is limited by materiality and content differences. IFRS S1 and S2 include risks and opportunities, while N-ESRS is designed around impacts. EFRAG also identifies additional N-ESRS climate content, including energy consumption and mix, locked-in emissions, 1.5°C compatibility, biogenic emissions, greenhouse gas removals and fossil-fuel sector disclosure.

Incorporation by reference to IFRS reporting is being considered as one way to avoid double reporting. Preparers with ISSB-aligned reports should therefore map reusable content separately from N-ESRS-only impact disclosures.

What to Test Before Consultation

The Exposure Draft should clarify the conditions for the mixed approach, the treatment of EU-related impacts, the use of non-EU references and the mechanics for incorporation by reference. Until then, useful preparation is not full compliance drafting. It is scoping the group, testing whether global or mixed reporting is supportable, checking impact evidence, and deciding where existing ISSB or ESRS material can reduce duplication.

N-ESRS appears narrower than full ESRS, but narrower does not mean a lighter data exercise. Climate remains global under the mixed approach currently described, value chain impacts remain within the impact definition, and incorporation by reference will not close the impact materiality gap by itself.