EFRAG Publishes Its First VSME-based Report

EFRAG has applied the VSME to its own 2025 sustainability reporting, creating a worked example for organisations considering the voluntary SME standard. The report is most useful where it shows the practical mechanics of first-year reporting: digital tagging, data limitations and policy gaps.

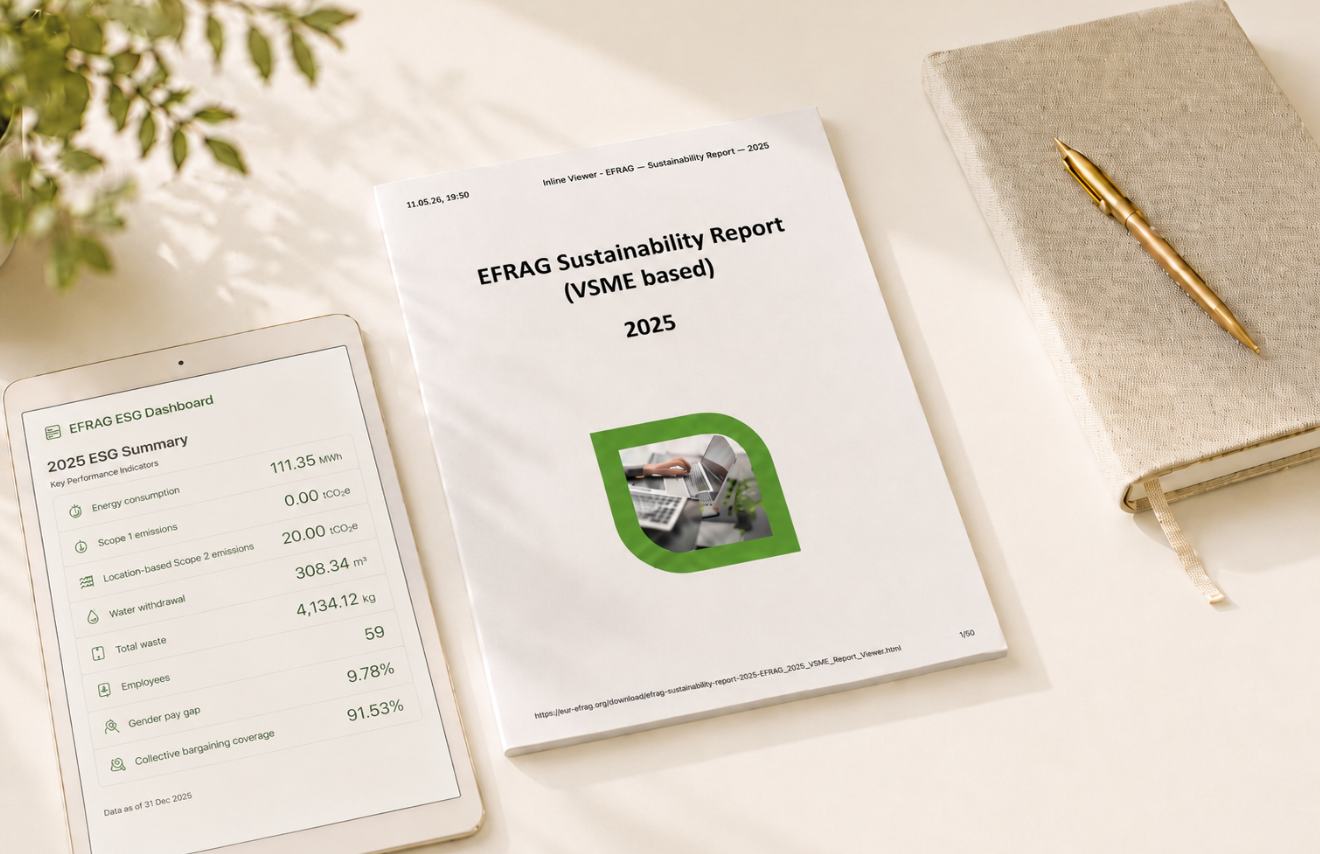

EFRAG has published its first Sustainability Report, covering 2025 and prepared under the Voluntary Standard for SMEs (VSME). For reporting teams, the development is practical: the organisation that developed the VSME and supports implementation of the European Sustainability Reporting Standards (ESRS) has applied the voluntary SME model to its own reporting.

The report can serve as a reference example for organisations preparing their first VSME-based report.

VSME Reporting in Practice

Published on 27 April 2026, the report covers the 2025 reporting year. It sets out EFRAG's ESG performance, current practices and planned initiatives. EFRAG is an AISBL, an international non-profit association, with 59 employees and one Brussels site.

EFRAG prepared the report on an individual basis under Option B, meaning that it used both the Basic and Comprehensive Modules of the VSME. The report has not been subject to assurance.

The digital format is a central feature. EFRAG used its VSME Digital Template and Converter, and the online version is a human-readable Inline XBRL report with an embedded viewer. Its disclosures are tagged to the VSME XBRL taxonomy, and the report contains 115 XBRL facts. This shows how VSME disclosures can be prepared as structured digital data.

What EFRAG Disclosed

EFRAG's environmental disclosures combine metrics, current practices and limitations in the underlying data. The main reported figures are:

- energy consumption: 111.35 MWh;

- Scope 1 emissions: 0.00 tCO2e;

- location-based Scope 2 emissions: 20.00 tCO2e;

- water withdrawal: 308.34 m³;

- total waste: 4,134.12 kg, including 141.96 kg of hazardous waste.

The data caveat is important. Because EFRAG operates from a shared Brussels site, gas, water and waste figures rely on an 11.18% allocation of building-level data rather than direct measurement. EFRAG notes that the waste figure may be excessive, especially for hazardous waste and paper.

The report also describes environmental practices already in place: energy-efficient office space, environmentally preferable commuting, renewable energy-powered server and cloud solutions, reduced paper use, e-waste collection, and return of old IT equipment for reuse, repair or responsible disposal. For 2026, EFRAG plans to improve environmental measurement, engage suppliers and the building administrator, add electric vehicle charging, and introduce an annual “data cleaning day”.

The social disclosures focus on EFRAG's own workforce. Reported figures include:

- 49 permanent and 10 temporary employees;

- 32 women and 27 men;

- 54 employment contracts in Belgium, two in Germany, and one each in Spain, France and Portugal;

- 12.70% turnover;

- no recordable work-related accidents or fatalities;

- 9.78% unadjusted gender pay gap;

- 91.53% collective bargaining coverage;

- 20 average annual training hours per male employee and 45 per female employee.

Governance is presented through EFRAG's due process and internal rules. The report also records gaps: no code of conduct or human rights policy for its own workforce, and no complaint handling mechanism. EFRAG reports no confirmed human rights incidents in its own workforce or in relation to workers in the value chain, affected communities, consumers and end-users. It also discloses a 0.25 gender diversity ratio in the governance body.

For 2026, EFRAG plans to introduce a Code of conduct, AI and cyber security training, and a formal EFRAG Sustainability Policy covering health, safety and well-being. It also plans to designate responsibility for occupational health and safety, formalise training programmes, and develop a complaints handling mechanism for employee-related matters.

Lessons for First VSME Reporters

For organisations preparing a first VSME-based report, EFRAG's example points to three priorities: assign ownership, document evidence and keep narrative disclosures consistent with figures, footnotes and XBRL tags.

The shared-building data is the clearest lesson. Allocated estimates can be used, but they need clear labelling, explanation and later improvement. Before drafting, teams need a defined reporting boundary: what is being reported, which site or entity it covers, and which data is directly measured rather than estimated.

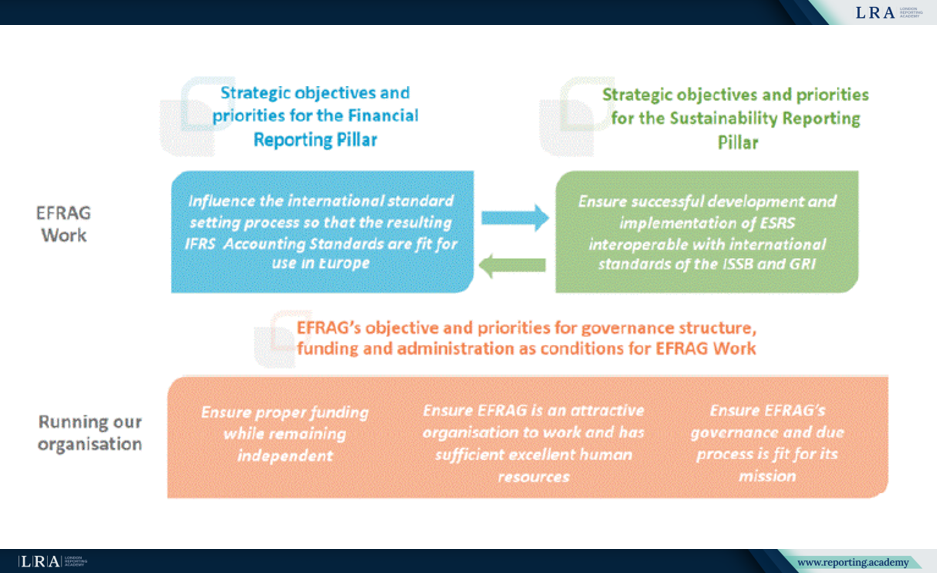

EFRAG's Two-pillar Role

The report places VSME reporting within EFRAG's wider corporate reporting mandate and its 2024-2027 Strategy. EFRAG works through two pillars: a Financial Reporting Pillar, focused on influencing IFRS Accounting Standards from a European perspective and advising the European Commission on endorsement; and a Sustainability Reporting Pillar, focused on developing and supporting ESRS and the VSME.

Source: EFRAG, Sustainability Report 2025

The strategy diagram connects these two pillars. On the sustainability side, EFRAG refers to the development and implementation of ESRS that are interoperable with international standards of the ISSB and GRI. Below both pillars, it identifies governance, funding, independence, human resources and due process as conditions for EFRAG's technical work. The report also notes that EFRAG is funded by the European Union through the Single Market Programme.

What Comes Next

EFRAG says the challenges identified during preparation are common for SME preparers and will inform future implementation support. It also states that the report can be used as a reference for other European AISBLs approaching first-year reporting.

For reporting teams, the value of the report lies in its treatment of boundaries, assumptions and gaps. It does not present first-year reporting as a perfect-data exercise. It shows how limitations can be disclosed and then converted into actions for the next cycle.

The next items to watch are updates to the VSME Digital Template and Converter, future implementation support, and whether EFRAG's 2026 actions strengthen the areas it identified: environmental measurement, supplier engagement, sustainability policy, code of conduct, cyber security training, health and safety ownership, training programmes and complaints handling.