ECB Links Climate and Nature-Related Risks to Credit and Capital

The ECB’s 2026 update focuses on how banks turn climate and nature-related risk information into prudential decisions. The reports connect client assessment, portfolio steering, collateral valuation and stress testing with the evidence used in sustainability and risk disclosures.

On 8 May 2026, the European Central Bank (ECB) published updated versions of two reports on good practices for climate and nature-related (C&N) risk management and stress testing. The update follows a five-year supervisory programme and precedes the application of the European Banking Authority (EBA) Guidelines on environmental scenario analysis.

Two Reports, One Direction

Good practices for climate and nature risk management covers strategy, governance, risk appetite, client due diligence, risk management and capital adequacy. ECB report on good practices for climate and nature-related risk stress testing focuses on scenarios, data and the transmission of C&N drivers into probability of default (PD) and loss given default (LGD).

After the 2022 thematic review, the ECB set staged deadlines: materiality assessments by March 2023, integration into governance, strategy and risk management by the end of 2023, and inclusion of C&N risks in stress testing and internal capital adequacy assessment processes (ICAAPs) by the end of 2024. By that point, all significant institutions had integrated climate risk into stress-testing frameworks, compared with 41% in 2022. Leading practices for at least some exposures rose from 3% of institutions in 2022 to 56% by the end of 2024.

The examples are illustrative, non-exhaustive and non-binding. The EBA Guidelines on the management of ESG risks have applied to institutions other than small and non-complex institutions since 11 January 2026. The EBA Guidelines on environmental scenario analysis apply from 1 January 2027.

From Materiality to Portfolio Steering

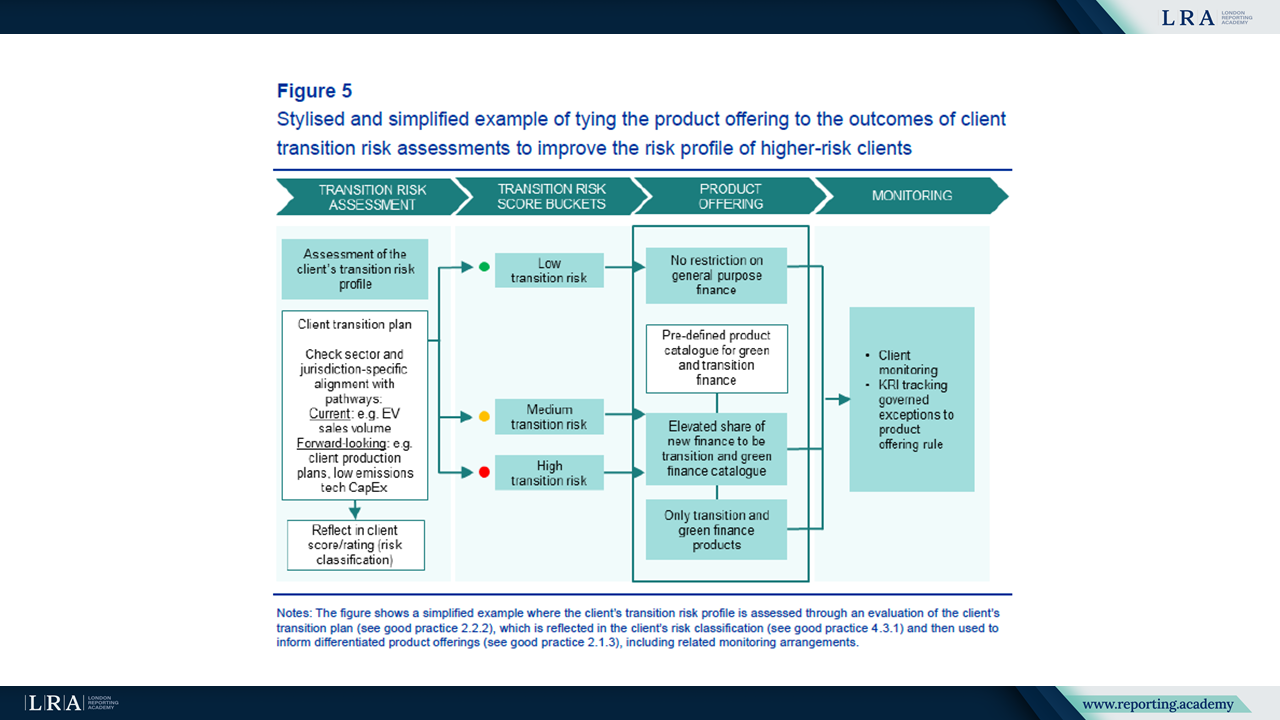

Prudential transition planning is a central strategic addition. The ECB describes banks linking transition risk drivers, strategic targets, risk appetite, risk management tools and transition finance products. Advanced practices use client-specific data and simulations to test whether portfolio trajectories remain aligned with targets.

If trajectories move off course, banks may adjust client engagement, key risk indicators, limits or profitability targets. The ECB illustrates this through a good-practice example where a client transition risk assessment determines the client’s risk bucket, product offering and monitoring arrangements.

Source: Client transition risk assessment and product offering, Good practices for climate and nature risk management.

Materiality assessment is treated as a live process. Good practices combine bottom-up risk events with top-down analysis across sectors, geographies, collateral types, products and single names. Drivers and exposures may sit below thresholds in isolation, then become material in aggregate.

The governance examples refer to the management body, second line and third line roles, with C&N risks embedded in risk appetite, key risk indicators, internal reporting and audit reviews. C&N information needs ownership beyond sustainability where it affects lending, limits, pricing or ICAAP.

Stress Testing Enters PD, LGD and Collateral

The stress-testing report moves from high-level climate sensitivity analysis to granular credit modelling. In 2022, good practices focused mainly on transition risk and PD. Follow-up work shows more banks modelling LGD, acute physical risks and early scenario approaches for nature-related risks.

For transition risk, the ECB points to counterparty-level analysis. Sector variables such as carbon price, gross value added and emissions intensity remain useful, but firms in the same sector can differ by emissions profile, investment needs, transition plan quality and cost pass-through capacity.

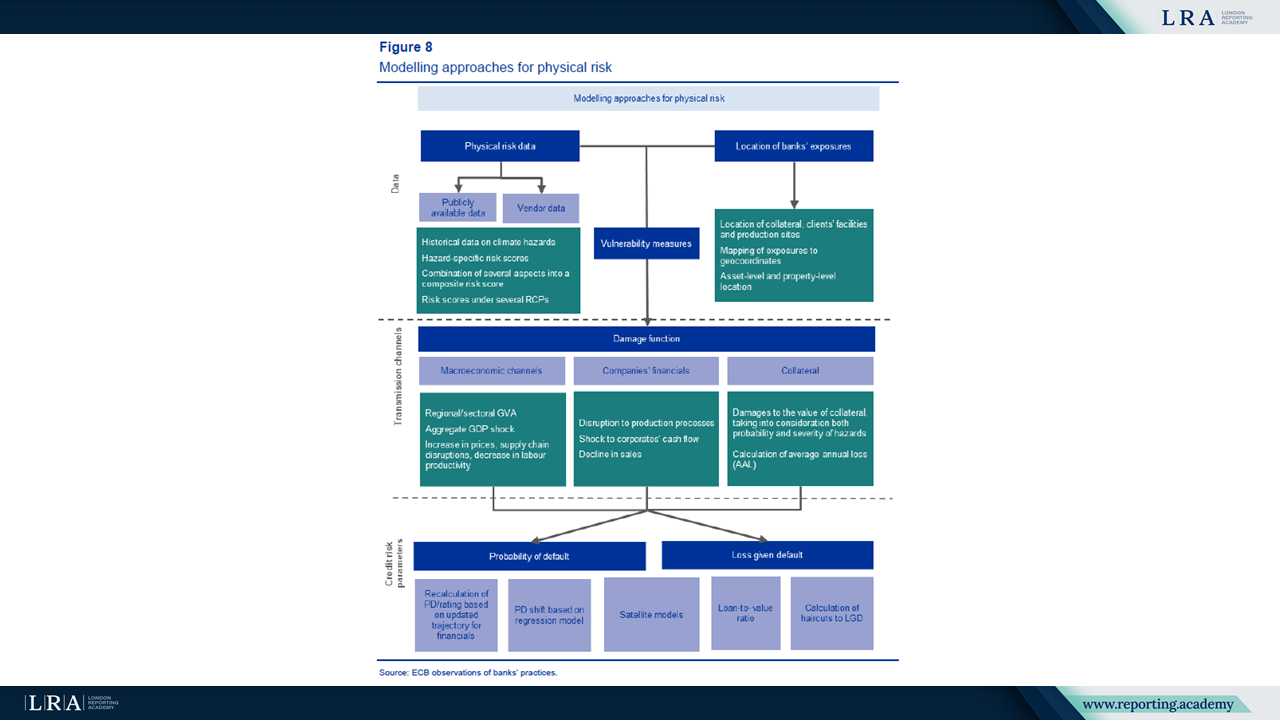

For physical risk, the 2026 update gives more detail on hazard, exposure and vulnerability. Good practices include asset-level geolocation, vulnerability data, damage functions, insurance information and defence measures.

The ECB’s physical risk modelling example shows how hazard data, exposure location and vulnerability measures feed into damage functions and then into PD and LGD estimates.

Source: Modelling approaches for physical risk, ECB report on good practices for climate and nature-related risk stress testing.

Collateral valuation is a stronger theme. Banks are modelling LGD through haircuts to collateral values, asset-level damage estimates and changes in loan-to-value ratios. A newly observed practice is EPC-adjusted LGD for real estate: transition risk is assessed at property level by looking at the EPC class change needed to align with the Energy Performance of Buildings Directive, then reflected in LGD.

Long-term modelling is another 2026 emphasis. Advanced approaches use dynamic balance sheets, sectoral or counterparty-level pathways and client transition plans to test how strategic choices affect credit risk over longer horizons.

Data Remains the Control Point

The stress-testing report largely carries over the 2022 data section, but still identifies gaps in greenhouse gas (GHG) emissions, energy performance certificates (EPCs), geolocation and physical risk data. Weak data can lead to mispriced lending, misallocated resources and overvalued collateral.

Good practices include centralised counterparty registries, NACE mapping, checks against FINREP and COREP, and emissions proxies based first on physical activity, then on economic activity. EPC practices include collection at mortgage origination, use of public registers, valuers collecting EPC information, and statistical or machine-learning models where data are missing.

Nature-related risks Enter the Framework

Nature-related risks receive more attention in the 2026 management report than in the earlier compendium. The ECB says most newly added good practices in that report concern nature risks, reflecting the early stage of methods and the need for practical reference points.

The update covers materiality, risk appetite, sector and client policies, due diligence, client scoring, project finance and capital adequacy. The stress-testing report adds early scenarios, including water scarcity, biomass price increases, environmental taxes, nitrogen-related restrictions and sectoral output shocks linked to biodiversity loss. The ECB notes that reference scenarios and agreed quantification methods remain limited.

Practical Meaning for Reporting Teams

For sustainability and non-financial reporting teams, the reports point to a more evidence-based approach to climate and nature (C&N) disclosures. Policy statements alone will be harder to support where the same risks affect lending, collateral values, pricing or capital adequacy.

The first area is data. Reporting teams should expect closer scrutiny of emissions data, EPCs, geolocation, insurance coverage and client transition information, including how proxies are used and validated.

The second area is consistency. If C&N risks are material in risk appetite, credit assessment, ICAAP or stress testing, the sustainability narrative should not describe them differently from risk and capital disclosures. Where the same assumptions feed both sustainability reporting and prudential risk processes, teams will need a clear audit trail for the figures and judgements used, including how they link to ICAAP and capital adequacy statements.

What to Watch Next

The next formal milestone is 1 January 2027, when the EBA environmental scenario analysis Guidelines apply. The ECB is also developing, with the EBA and national authorities, a framework to include transition and physical risks in the EU-wide stress test.

For reporting teams, the practical issue is whether sustainability data, assumptions and judgements can be reconciled with risk appetite, credit assessment, collateral valuation, ICAAP and stress-testing processes.