TISFD Sets Out a Draft for Social Reporting

Social reporting is gaining a more formal architecture. TISFD’s beta framework brings people-related impacts and dependencies into the same disclosure conversation as governance, strategy, risk management and financial effects.

The Taskforce on Inequality and Social-related Financial Disclosures (TISFD) has released Beta Version 0.1 of its framework for reporting people-related information. The draft comes as inequality, workforce conditions and social impacts are increasingly being treated as factors in business performance, investment analysis and risk management.

The practical shift is from fragmented, difficult-to-compare people-related disclosures to an integrated framework for assessing impacts and dependencies as the basis for risks and opportunities.

TISFD frames the business case against a widening social risk base: more than one billion working people do not earn enough for a decent living, around 2.1 billion workers are in informal employment, and 40% of global employment is exposed to AI. It also links climate pressure to people-related risk, citing 640 billion labour hours lost to heat exposure in 2024.

The Framework in Brief

Launched in early 2025, TISFD is a global, evidence-based, multi-stakeholder initiative driven by financial institutions, business, civil society and labour leaders. It was created to advance the integration of people-related issues into financial disclosures, recognising their relevance to long-term value, resilience and macroeconomic stability.

The consultation is open until 31 July 2026, with further consultation expected before final recommendations are published in 2027.

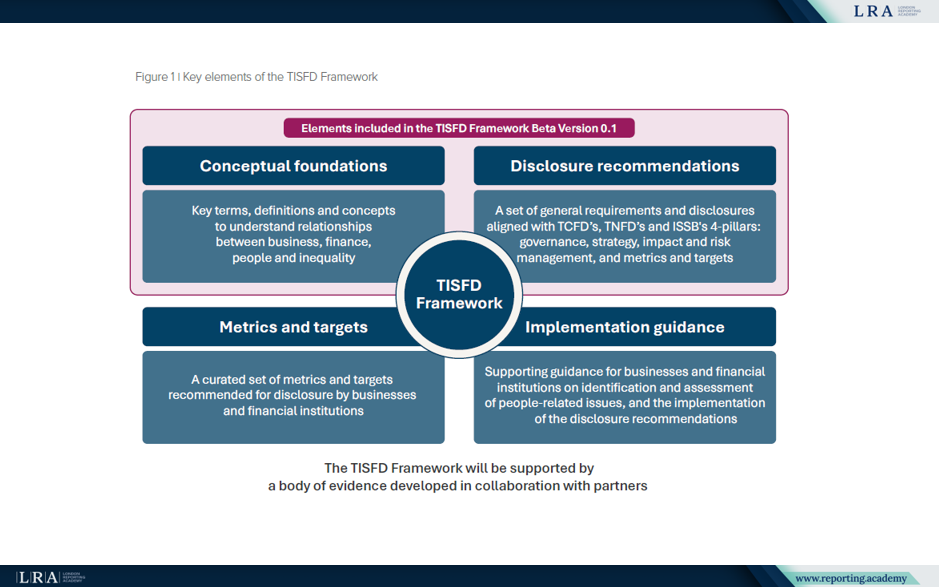

The current version contains conceptual foundations for understanding relationships between business, finance, people and inequality, alongside a first set of draft disclosure recommendations. It also identifies areas still to be developed in later iterations.

At this stage, the draft sets the reporting architecture; measurement, assessment methods and implementation guidance remain open for further development.

Source: Key elements of the TISFD Framework, The TISFD Framework

The framework is designed for businesses and financial institutions as preparers of general-purpose financial disclosures. It is also relevant for financial institutions, policymakers, regulators, supervisors, central banks, labour organisations and civil society as users of information.

The Concepts Behind the Draft

TISFD builds its approach around the “state of people”. The concept brings together human rights, labour rights, well-being, and human and social capital, and looks at both individual and collective aspects of people’s lives. It also distinguishes between horizontal inequalities, such as disparities by gender, race, disability or location, and vertical inequalities, such as gaps between the top and bottom of an income, wealth or health distribution.

The draft anchors people-related disclosure in established expectations on responsible business conduct, including the responsibility to respect human rights and labour rights. It refers to the UN Guiding Principles on Business and Human Rights and the OECD Guidelines for Multinational Enterprises on Responsible Business Conduct as part of this foundation. In practical terms, this makes human rights due diligence, meaningful stakeholder engagement and access to remedy part of the disclosure logic, not a separate compliance exercise.

The state of people lens widens the reporting boundary beyond employees. TISFD asks preparers to consider affected people across the workforce, value chain, communities and end-users, including groups that may face heightened vulnerability.

The operational logic is built around pathways. Impact pathways trace how business activity affects people and inequalities; dependency pathways trace how the organisation relies on human and social resources, from workforce capability to social cohesion and functioning institutions.

TISFD also makes the drivers of impact more concrete. Pay, working conditions, procurement, capital allocation, product design, tax practices and lobbying are presented as decisions through which business and finance can shape people-related outcomes.

The same integrated logic applies to people, nature and climate. The draft connects social reporting with just transition and climate and nature strategies, including cases where environmental action creates trade-offs for workers or communities.

How the Draft Structures Disclosure

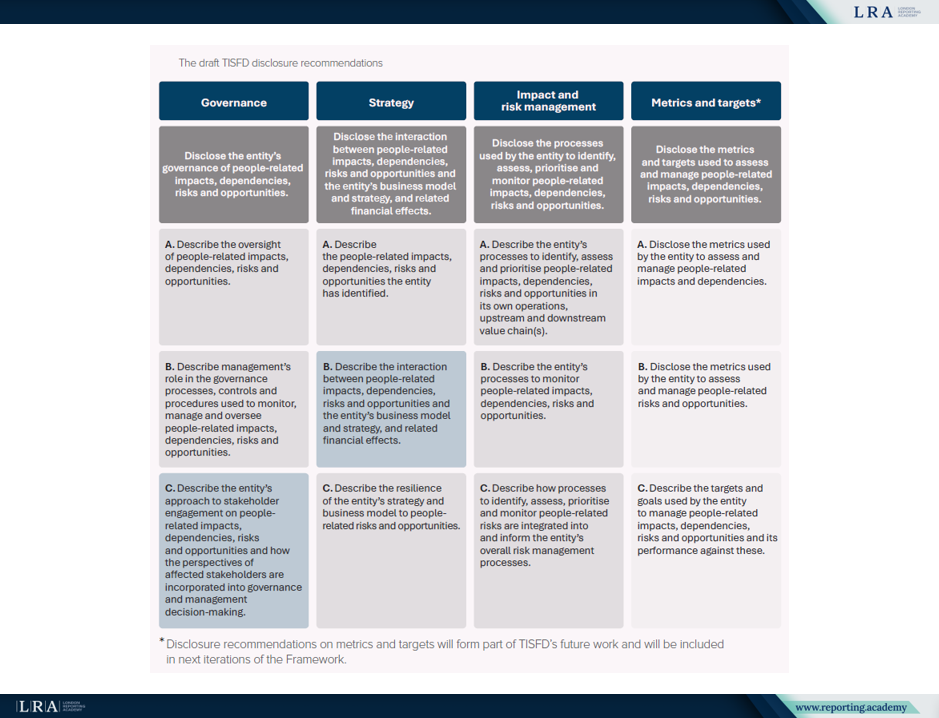

The draft disclosure recommendations are organised around four pillars: governance, strategy, impact and risk management, and metrics and targets. In Beta Version 0.1, the detailed recommendations are developed for governance, strategy, and impact and risk management, while the metrics and targets pillar is identified for future work. Governance focuses on oversight of people-related impacts, dependencies, risks and opportunities. Strategy addresses the interaction between those matters, the business model and strategy, and related financial effects. Impact and risk management covers processes to identify, assess, prioritise and monitor people-related matters across own operations and value chains.

Source: The draft TISFD disclosure recommendations, The TISFD Framework

The recommendations also sit under five general requirements: materiality, system-relevant information, stakeholder engagement, scope and time horizons.

For preparers, these requirements set the conditions for useful disclosure. Reports should explain what is material, what may be relevant to system-level risk, who has been engaged, what assessment boundary has been used and which time horizons apply. Stakeholder engagement is therefore not only an evidence source; it is one of the mechanisms through which entities understand impacts, dependencies and materiality.

Materiality and System-level Risk

Materiality is treated as the foundation for disclosure. The framework states:

“Organisations should disclose material information about their people-related impacts, dependencies, risks and opportunities.”

The draft is designed to accommodate financial materiality, impact materiality and double materiality. Its practical point is that the assessment of impacts and dependencies is a necessary starting point for assessing risks and opportunities, irrespective of the materiality approach applied.

TISFD also widens the discussion beyond entity-level financial effects. Cumulative impacts can affect social cohesion, productivity, demand, macroeconomic performance and financial stability. For diversified investors and financial institutions, these risks can affect the market as a whole and cannot be easily diversified away.

This is where system-relevant information becomes important. The draft uses the term for disclosure on people-related externalities that may matter for system-level risk, even where the route to entity-level financial effects is indirect. Information on impacts and how they are managed can also help users anticipate regulatory, legal, reputational or market risks.

What the Draft Means in Practice

For companies and financial institutions, Beta Version 0.1 provides a way to test whether people-related issues are visible in governance, strategy and risk management.

The draft moves reporting beyond workforce indicators. It asks organisations to consider how they affect and depend on people across their own operations, value chains, consumers, end-users and affected communities, and whether those impacts and dependencies connect to financial risks, opportunities and system-level risk.

Its immediate value is to expose gaps in current reporting architecture before later versions add more detailed metrics, targets and assessment guidance.

Fit with Existing Reporting Architecture

TISFD says the framework supports convergence with ISSB Standards, GRI Standards and ESRS Standards. It also aligns structurally with the Taskforce on Climate-related Financial Disclosures (TCFD) and the Taskforce on Nature-related Financial Disclosures (TNFD).

The point for preparers is interoperability. TISFD is designed to complement existing sustainability and financial reporting standards, so people-related disclosures can be mapped into frameworks many organisations already use rather than built as a parallel reporting exercise.

The connection with climate and nature is not an add-on. TISFD presents it as part of coherent governance and transition strategy, because social conditions can affect the durability of climate and nature plans, and environmental change can worsen people-related impacts and inequalities.

What to Watch Next

TISFD identifies three channels for shaping the framework: the TISFD Alliance, public consultation and pilot testing. The pilots could be especially important in showing how the draft works across sectors, business models and data environments.

For now, the draft’s main contribution is to give companies and financial institutions a clearer way to connect social information with business resilience, financial effects and system-level risk. It remains under consultation, but it already signals a shift in social reporting: from describing people-related issues as separate sustainability topics to treating them as part of long-term value creation and risk management.