SBTi V2.0: The Next Phase of Corporate Net-Zero

Corporate net-zero targets are becoming less about public commitments and more about delivery systems. The focus is shifting to how targets are governed, supported by data and assessed over time.

The Science Based Targets initiative (SBTi) has released Corporate Net-Zero Standard Version 2.0 as a full revision of its corporate net-zero framework. The standard was released on 11 June 2026 and becomes effective on 1 February 2027. For companies, the update makes target delivery more explicit, with stronger links to governance, transition planning, progress reporting and evidence.

The shift is from setting science-based targets as a stand-alone commitment to embedding those targets in governance, transition planning and operational decision-making.

A Revised Framework for Delivery

Corporate Net-Zero Standard Version 2.0 is the foundational cross-sector SBTi standard for companies. It sets requirements for Scope 1, Scope 2 and Scope 3 emissions, covering Scope 3 categories 1–14 under the GHG Protocol Corporate Standard. Scope 3 Category 15 financial activities are addressed through the Financial Institutions Net-Zero Standard, which may apply to financial institutions and may be relevant for other companies with Category 15 emissions.

V2.0 places targets inside a clearer delivery process, linking target base year data, transition planning, annual reporting, end-of-cycle assessment and an implementation hierarchy.

The best-efforts basis is central to this process. Companies are expected to use all available levers, disclose assumptions and dependencies, explain barriers, and show how they are addressing them over time. This is especially relevant for Scope 3, where delivery often depends on suppliers, customers, infrastructure and technologies outside the company’s direct control. It also makes underperformance more visible, because higher emissions at the end of a target cycle lead to steeper reductions and faster action in the next cycle.

SBTi also frames V2.0 as part of a broader shift in its role. In the foreword, it describes moving beyond setting the bar and validating targets towards supporting implementation, sharing learning across its company network and helping surface systemic barriers. This context helps explain why the revised standard places more emphasis on transition planning, progress reporting and implementation.

Status, Obligations and Voluntary Elements

Version 1 remains open for setting targets until the end of 2027 for companies that have planned against it. Companies with existing 2030 targets should start setting targets for the 2030–2035 cycle under V2.0 from 2028. The transition is therefore staged, not immediate.

The standard is precise about obligation. Requirements written with “shall” apply to companies submitting targets for SBTi assessment. “Recommendations” remain good practice rather than requirements. “May” indicates a permitted option, while “can” describes an ability or possibility. Where the standard uses “must”, it refers to external constraints, such as legal or regulatory requirements, rather than a separate SBTi requirement.

The criteria tables need to be read carefully. Criteria marked as CNZS-C# set the main requirements, while sub-criteria marked as C#.# break them into specific conditions. Criteria may also include R#.# recommendations, which identify practices companies are encouraged to follow. Each criterion shows the applicable company category and assessment stage, such as Target Validation or End-of-cycle Assessment.

SBTi validation should not be read as full verification of a company’s climate data or transition plan. The assessment checks whether the company conforms with defined criteria, while responsibility for data accuracy remains with the company and, where relevant, its assurance provider. For transition plans, SBTi checks that a plan exists and includes the required elements; it does not endorse the plan’s overall feasibility.

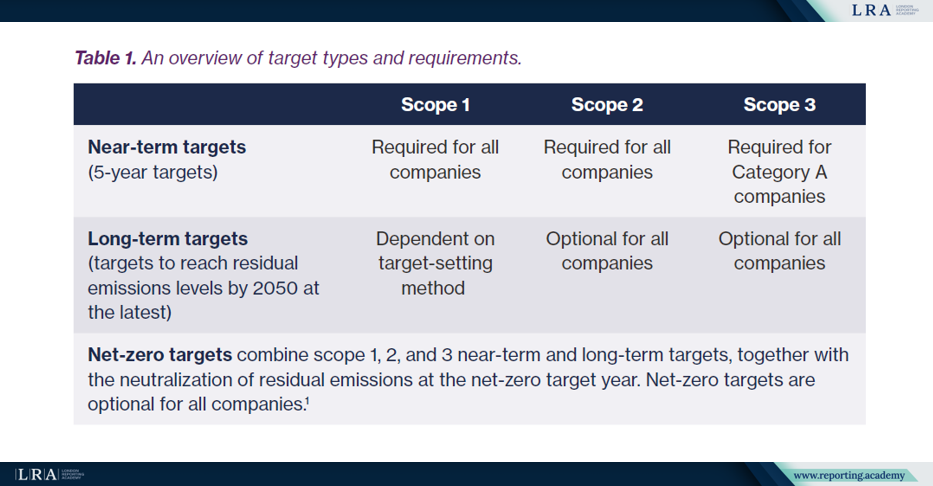

The table below shows the main target-setting split in V2.0. Near-term targets form the mandatory core, while net-zero targets remain optional for all companies. If a company chooses to set a net-zero target, however, it brings the full Scope 1, Scope 2 and Scope 3 net-zero architecture into scope, including neutralisation of residual emissions.

Source: Required and optional target types, SBTi Corporate Net-Zero Standard V2.0.

Scope, Categories and Target Cycles

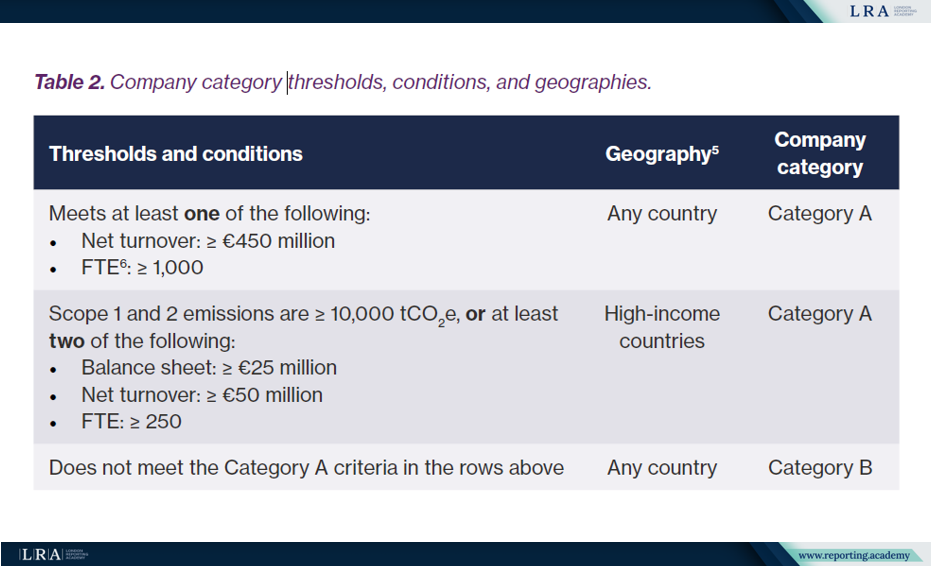

The standard is intended for companies globally. It classifies companies into Category A and Category B by size and geography, using thresholds linked to turnover, employees, emissions and, for some companies, balance sheet size. Some Category A requirements are optional for Category B, including transition plan disclosure, assurance of target base year data and Scope 3 target setting.

Source: Company category thresholds, SBTi Corporate Net-Zero Standard V2.0

A separate fossil fuel boundary applies. Companies with any direct involvement in exploration, extraction, mining and/or production of oil, natural gas, coal or other fossil fuels cannot validate targets at this stage until sector methods or guidance are finalised. The standard separately notes exceptions for companies deriving less than 50% of revenue from the sale, transmission and distribution of fossil fuels, or from providing equipment or services to fossil fuel companies.

Target setting works in cycles. The target base year is the most recent year with comprehensive data, but this is not a reset of the decarbonisation journey. Companies set new targets based on the most recent progress, so gaps are carried forward rather than written off.

How Target-Setting Changes by Scope

V2.0 gives companies more than one route for target-setting. Scope 1 targets can use absolute emissions reduction, emissions intensity reduction or asset transition, with the last route designed for companies whose capital stock does not follow a simple linear pathway. Scope 2 targets can be based on emissions reductions and/or increases in low-carbon electricity, with implementation linked to investment, power purchase agreements, contracts for difference and renewable energy certificates.

Two Scope 2 details matter for preparers. Existing long-term power contracts receive legacy treatment under defined conditions, and Category A companies with large electricity loads must report hourly matching where significant electricity use reaches 10 GWh or more in an activity pool. Voluntary SBTi recognition applies to companies that meet specified hourly matching thresholds.

For Scope 3, Category A companies must cover significant categories, subject to limited and justified exclusions. The standard allows three routes: overarching emissions reduction targets, supplier or customer alignment targets, and category- or activity-specific targets.

Implementation, Claims and OER

V2.0 introduces an implementation hierarchy. Companies should prioritise direct actions in operations and value chains, then actions in shared systems such as grids or supply networks, with sector-level actions available only where lower-level options are constrained.

Market instruments may support action, but they are subject to integrity guardrails including activity matching, system association, conservative quantification, verifiability, temporal alignment and no double counting. This matters for claims: companies need to distinguish actions that change their physical inventory from actions that support wider system decarbonisation.

Ongoing Emissions Responsibility (OER) remains a separate layer. The OER recognition programme has Engaged, Advanced and Leadership levels and remains optional until 2035, after which Category A companies will be required to support eligible carbon removals. The recognition model continues alongside the post-2035 requirements. By the net-zero target year and thereafter, companies with net-zero targets must neutralise residual emissions using eligible carbon removals.

Communications under the Corporate Net-Zero Standard will need to follow the SBTi Claims System when available. This will govern claims about validated targets, progress and recognition programmes, while broader environmental claims remain the company’s responsibility.

Practical Meaning for Reporting Teams

For reporting teams, V2.0 is mainly a coordination exercise. Data and boundaries underpin target architecture, while governance approval and transition planning need to run in parallel before validation. After validation, teams need to connect annual progress reporting, evidence for actions taken, assurance readiness and claims discipline.

The practical task is to keep targets, evidence and disclosures aligned. Teams should be clear about what SBTi has assessed, what the company reports, what has been assured by a third party, and how OER recognition, system contribution claims and net-zero claims differ.

What to Watch Next

The core message for reporting teams is that V2.0 makes delivery evidence more visible.

Targets still matter, but they now sit inside a cycle of governance approval, transition planning, reporting, assurance and reassessment. The best-efforts approach gives companies a way to explain real barriers, but it is not an exemption from accountability. Next areas to watch include the transition from Version 1, SBTi assurance and claims documents, Sector Standards updates and further guidance on market instruments.