GRI Leads Global Sustainability Reporting in 2025

A new GRI study offers a snapshot of how sustainability reporting is being used by large listed companies worldwide. Its findings show GRI’s continued role in impact reporting, while also pointing to a reporting landscape increasingly shaped by ESRS, ISSB and other frameworks.

The Global Reporting Initiative (GRI) has published The State of Sustainability Reporting: Global Trends in the GRI Standards 2025. According to GRI’s analysis, the GRI Standards are the most widely used sustainability reporting framework among large listed companies. The findings come as companies face new reporting requirements in Europe, uncertainty in the United States, and questions over the burden and complexity of sustainability reporting.

The report points to a layered reporting system in which impact and financial materiality serve different users and information needs.

How the Study Was Built

GRI’s study examines how large listed companies report on sustainability and where the GRI Standards sit within the wider reporting system.

The analysis is based on public reporting by 14,682 publicly listed companies with annual revenue of USD 250 million and above. GRI says this threshold was chosen because it captures companies with significant sustainability impacts and supports geographical and sectoral comparison. The sample focuses on large publicly listed companies and should not be read as representing all large companies or all publicly listed companies globally.

The most recent sustainability report for each company was identified and downloaded in December 2025. For most companies, the reports analysed referred to the 2024 financial year. GRI then used automated text analysis to identify references to GRI and other standards and frameworks.

In the study, a company is treated as using a framework if it refers to that framework in its sustainability disclosures. For the GRI Standards, the report also separates out more formal use, where a company publishes a GRI content index or statement of use. The figures therefore show stated framework reference, not the quality, completeness or assurance of disclosures.

What the Data Shows

According to GRI’s analysis, 87% of large publicly listed companies publish sustainability reports or disclosures. The GRI Standards are referenced by 40% of large listed companies and by companies representing 62% of global market capitalisation. Formal GRI reporters account for 23% of companies and 40% of global market capitalisation.

GRI also finds that use increases with company size. That makes the framework especially relevant for larger issuers and for stakeholders who use sustainability information to assess risk, allocate capital or hold organisations accountable.

A Multi-Framework Market

In global sustainability reporting, one framework is rarely the whole picture. Large companies often combine the GRI Standards with TCFD, SASB, CDP, ISSB, ESRS and TNFD to address different information needs.

GRI’s analysis finds that the GRI Standards lead among sustainability reporting frameworks by number of companies and by market capitalisation. The SDGs are also among the most referenced instruments in the study, appearing in 40% of company disclosures and representing 50% of market capitalisation.

Together, these figures show a market where several frameworks are used side by side. GRI remains widely referenced, while other frameworks add more specific disclosure lenses. For reporting teams, the practical question is consistency across disclosures.

ESRS Сhanges the picture in Europe

The introduction of the European Sustainability Reporting Standards (ESRS) in the EU and EEA has reduced the number of companies using the GRI Standards in that region. At the same time, GRI notes that ESRS means 30 countries now require reporting on sustainability impacts through a double materiality approach.

In the EU, GRI says 68% of companies and 80% of market capitalisation report on impacts using GRI, ESRS or both.

The distinction changes how the European trend should be read. A fall in direct GRI use does not necessarily mean a fall in impact reporting. It may reflect a move from voluntary or market-led use of GRI towards mandatory ESRS-based impact disclosures.

GRI also says the decrease was not limited to its own Standards. References to SASB, CDP, TCFD and the SDGs also fell year on year, suggesting that the change reflects wider market conditions in some jurisdictions.

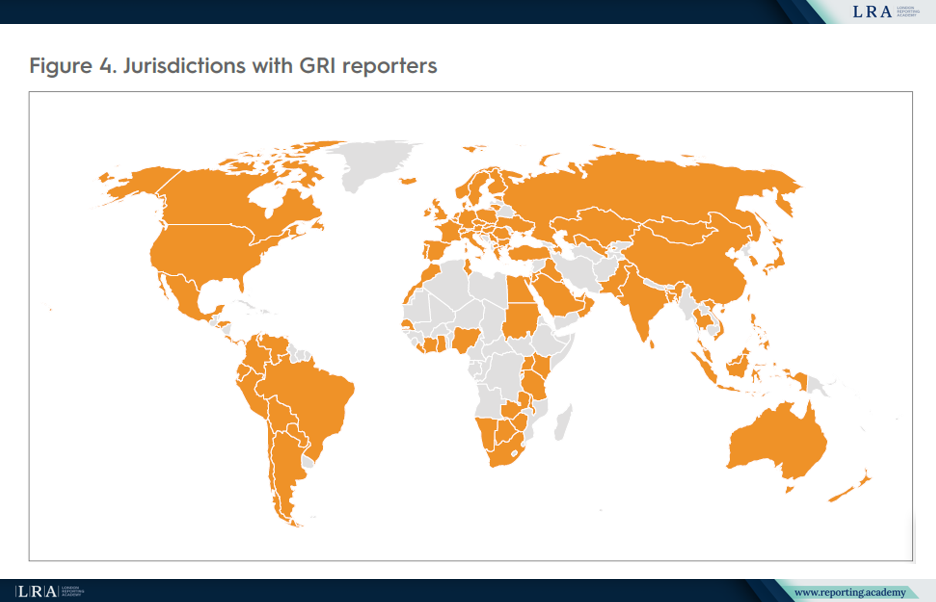

Global Reach and Regional Growth

GRI reporters are headquartered in 107 jurisdictions, giving the framework a broad global footprint. GRI also says sustainability reporting that includes the GRI Standards can already be considered “standard practice” in 45 jurisdictions, using a threshold of 50% of companies reporting with GRI. Outside Europe, North America and Oceania, GRI use is rising in Asia, Africa, the Middle East and Latin America.

The highest GRI reporting rates by number of companies are in Taiwan, China at 95%, Argentina at 82%, Colombia at 79%, Singapore at 76%, Brazil at 71% and Malaysia at 70%. The figures show that impact reporting is being shaped not only by European regulation, but also by market practice in Asia and Latin America.

Sector data adds another layer. In oil and gas and electronics, GRI reporting represents more than 80% of market capitalisation. By contrast, it is below 30% in health services and restaurants. This suggests that GRI carries particular weight in sectors with high impact profiles and strong stakeholder scrutiny.

Source: Jurisdictions with GRI reporters, The State of Sustainability Reporting: Global Trends in the GRI Standards 2025

What Companies Disclose

GRI stresses that Topic Standards are flexible and depend on a company’s materiality assessment. Companies select standards based on their most significant environmental, social or economic impacts.

The three most referenced GRI Topic Standards are:

- GRI 305: Emissions 2016

- GRI 302: Energy 2016

- GRI 403: Occupational Health and Safety 2018

The takeaway is that companies use GRI where the standards align with their most significant impacts, supporting both internal impact management and stakeholder understanding.

What the Study Adds

The study is useful because it captures a shift in the reporting landscape. GRI remains a leading reference for impact reporting, while ISSB is gaining regulatory traction across jurisdictions and ESRS is being reshaped in Europe through simplification.

This points to a more segmented reporting architecture: global momentum around investor-focused sustainability disclosures, continued demand for impact reporting, and a European framework that is becoming more targeted after the Omnibus package.

The main question is no longer whether one standard will dominate. It is how impact, financial and jurisdiction-specific disclosures will fit together without making the reporting system harder to navigate.