GHG Protocol Publishes Land Sector and Removals Implementation Package

GHG Protocol has moved land-sector accounting from standard-setting to implementation. The new package combines the updated Standard, detailed guidance and reporting tools to help companies account for land emissions, CO₂ removals and related metrics from 2027.

On 30 June 2026, GHG Protocol released the Land Sector and Removals Guidance alongside an updated version 1.1 of the Land Sector and Removals Standard (LSR Standard), a Reporting Requirements Checklist and a Sample GHG Inventory Reporting Template. The package supports implementation before the Standard and Guidance take effect on 1 January 2027.

The Guidance and reporting tools complement the Standard with detailed application support and practical disclosure resources.

From Standard to Implementation

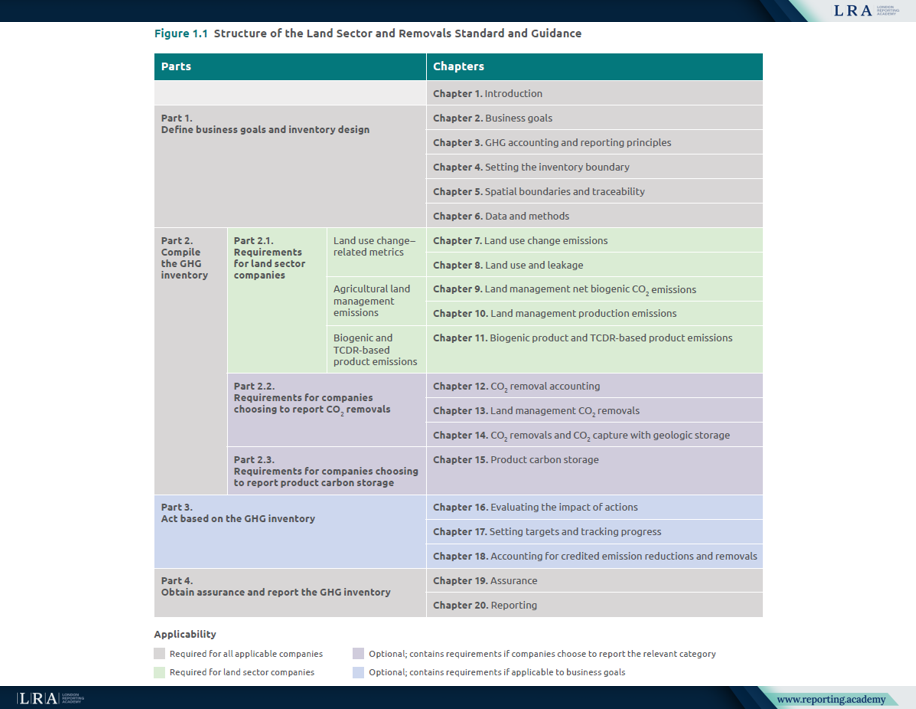

The LSR Standard supplements the GHG Protocol Corporate Standard and Scope 3 Standard and supersedes the previous Agricultural Guidance. It contains 32 requirements for annual, entity-level inventories covering land-sector emissions, CO₂ removals and related metrics. Not all requirements apply to every company; their relevance depends on the company’s business goals and inventory boundary.

Version 1.1 replaces the January 2026 edition without redesigning the accounting model. It clarifies several technical and reporting issues across land management, biogenic products, Scope 3 and total emissions. It also adds examples of digital tracking methods to the recommendation on ongoing product carbon storage monitoring.

The Guidance mirrors the Standard’s 20 chapters and explains how to apply them through calculations, examples and ten corporate case studies. The Checklist helps companies verify that all required information is included, while the Sample Template shows how to present both descriptive and quantitative disclosures. Companies may use a different format, provided that all required reporting information is included.

Source: Structure of the Land Sector and Removals Standard and Guidance, Land Sector and Removals Standard

Scope and Timing

Companies reporting in conformance with GHG Protocol must follow the LSR Standard and Guidance when significant land-sector activities occur in their operations or value chain. The same requirement applies when a company reports CO₂ removals or CO₂ capture with geologic storage, including where it has done so previously.

Potential users include agricultural producers, food and beverage companies, retailers, bioenergy and biomaterial businesses, and operators involved in technological removals or geologic storage. A company with land-sector activities that does not follow the LSR Standard and Guidance must disclose and justify why those activities are not significant. GHG Protocol does not prescribe a specific significance threshold, so companies need to explain the basis for that assessment.

Version 1 of the Standard and Guidance covers agriculture and CO₂ removal technologies but does not provide comprehensive requirements for forestry. GHG Protocol has opened a Forest Carbon Accounting Request for Information until 1 February 2027 to inform future work.

A More Structured GHG Inventory

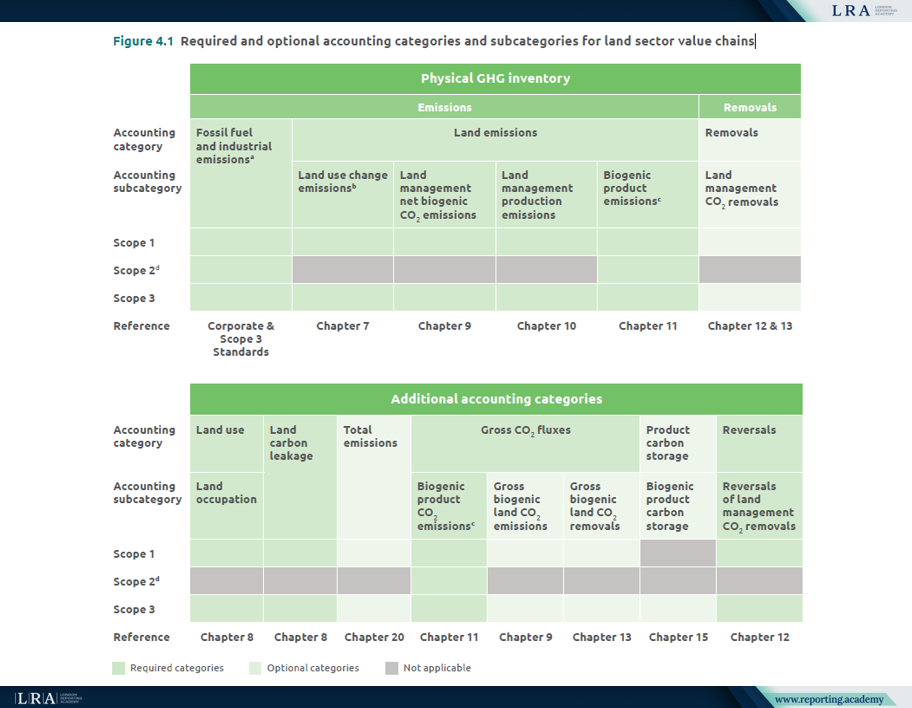

The LSR Standard requires companies to report land emissions separately from fossil fuel and industrial emissions. Within land emissions, it distinguishes between land use change emissions, land management net biogenic CO₂ emissions, land management production emissions and biogenic product emissions.

Source: Required and optional accounting categories and subcategories for land sector value chains, Land Sector and Removals Standard

Scope 1 and Scope 2 emissions must be broken down by the relevant accounting subcategories and, where applicable, by individual greenhouse gas. Scope 3 emissions must be reported separately for each applicable Scope 3 category, with further breakdown by the relevant land-related subcategories. Version 1.1 clarifies that companies are not required to present a single total combining all Scope 3 categories.

Additional accounting categories must be presented separately where applicable. These include land use, with land occupation as its subcategory, land carbon leakage, specified gross CO₂ fluxes and reversals. Product carbon storage is optional and, if reported, must remain separate from the physical GHG inventory.

Reporting CO₂ removals is optional. If a company chooses to report them, the applicable requirements vary by removal type. These include stock-change accounting for land management removals, reporting life-cycle GHG emissions, physical traceability for Scope 3 removals, and ongoing storage monitoring and reversals where applicable. Product carbon storage is a separate optional category and is not reported as a removal.

Required disaggregated emissions and removals remain visible as distinct figures. A permitted aggregate or net value may be added, but it cannot replace the underlying disaggregation.

What Changes for Reporting Teams

Companies must document their consolidation approach, reporting period, boundaries, exclusions and the link between Scope 3 sourcing areas and relevant products. Data systems must also support calculation, traceability and evidence on sourcing regions, land management units or harvested areas.

Companies must explain the methods, assumptions, data sources, data quality and uncertainty underlying the inventory. For each Scope 3 category, companies must report the percentage of emissions calculated using supplier or other value-chain partner data.

Required inventory information must be publicly reported. The Standard and Guidance do not mandate the use of specific calculation tools or datasets. Companies select resources based on their sector, geographic location, data availability and the applicable requirements and recommendations.

Assurance and Accounting Boundaries

The Standard requires companies to disclose whether third-party assurance was performed, the level obtained, the provider’s relevant competencies and the opinion issued. Where assurance was not obtained, the company must explain and justify why. The Standard recommends obtaining at least a limited level of assurance.

The LSR Standard does not provide requirements or guidance on project accounting, GHG credit certification or GHG credit verification, although it includes provisions intended to avoid double counting with credited reductions and removals.

Preparing for 2027

Companies should determine whether the Standard applies, map existing inventory data against the required categories and assess whether current systems can support the necessary disaggregation, traceability and documentation.

The package does not remove judgement from land-sector accounting. It makes those judgements more visible and reviewable, placing early emphasis on significance assessments, boundary decisions, carbon stock methods, removals, reversals and supporting evidence.