EU Framework Proposes Streamlined Access to Sustainable Finance for SMEs

The Platform on Sustainable Finance has introduced a new voluntary framework to enhance access to sustainable finance for SMEs. The "SME Sustainable Finance Standard" outlines simplified eligibility criteria and reporting guidance tailored to the capacities of smaller enterprises.

The Platform on Sustainable Finance has published a new report, "Streamlining Sustainable Finance for SMEs" introducing a voluntary framework intended to help small and medium-sized enterprises (SMEs) and their financiers demonstrate alignment with environmental sustainability performance. The SME Sustainable Finance Standard proposes a simplified, consistent approach for evaluating SME-related finance under the broader EU sustainable finance framework. As noted in the report, the Standard is designed to facilitate access to sustainable finance through a streamlined and proportionate approach, particularly tailored to the needs and capacities of SMEs.

About the Platform and Related EU Initiatives

The Platform on Sustainable Finance is an expert advisory body to the European Commission, supporting the development and implementation of sustainable finance policy. Its work complements core initiatives such as the EU Taxonomy – a classification system for environmentally sustainable economic activities – and the InvestEU Programme, which aims to mobilise investment for key policy areas including sustainability and innovation.

Context and Purpose

SMEs play a central role in the EU economy, accounting for over 50% of the Union’s GDP and an estimated 63% of enterprise CO₂ and broader GHG emissions. Their contribution makes them pivotal to Europe’s sustainability transition. Achieving a net-zero, resilient, and environmentally sustainable economy depends on SMEs’ ability to access the necessary financing to decarbonise, build climate resilience, green their operations, and develop sustainable products and services.

Despite this importance, SMEs face significant challenges in securing external financing for sustainability-related efforts. Most rely on internal funding, and when external support is sought, bank loans are the primary channel. The limited volume of financing classified as sustainable stems from issues such as high minimum loan sizes, complex regulatory requirements, the absence of harmonised definitions for sustainable finance, and insufficient sustainability-related data, particularly in relation to the EU Taxonomy.

The Taxonomy framework, while increasingly used to classify and access green finance, remains difficult for SMEs to navigate. As a result, few SMEs use it voluntarily to demonstrate environmental sustainability. Nonetheless, growing expectations from financiers and value chain partners are prompting SMEs to provide Taxonomy-aligned information.

To address these barriers, the Platform proposes a tailored and simplified approach – the SME Sustainable Finance Standard – designed for use by banks and other financiers to classify loans and other financing provided to SMEs as sustainable (green or transition finance) and to streamline associated voluntary reporting. The standard is not intended for use under the Omnibus proposals by companies that are not SMEs. However, some SMEs may still choose to report in alignment with the Taxonomy to access green finance, particularly if forthcoming legislative updates further simplify disclosure obligations. Even then, the Taxonomy may remain impractical for many SMEs.

Key Components of the SME Sustainable Finance Standard

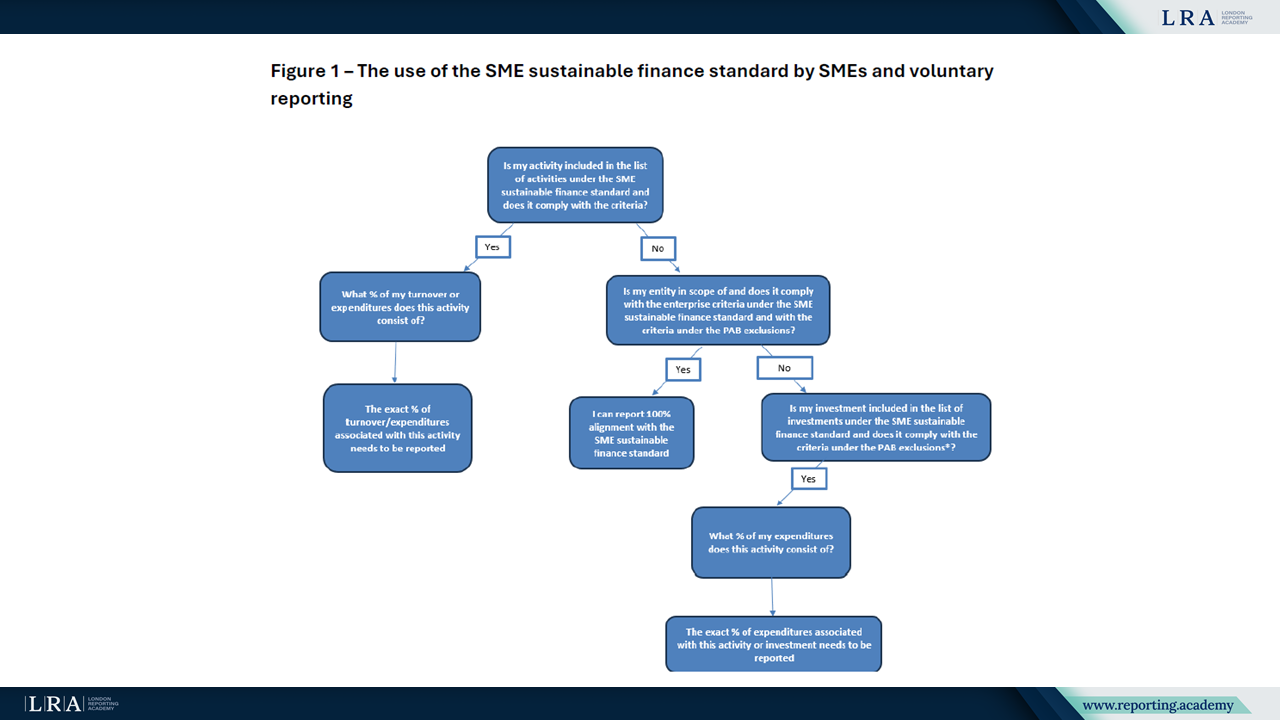

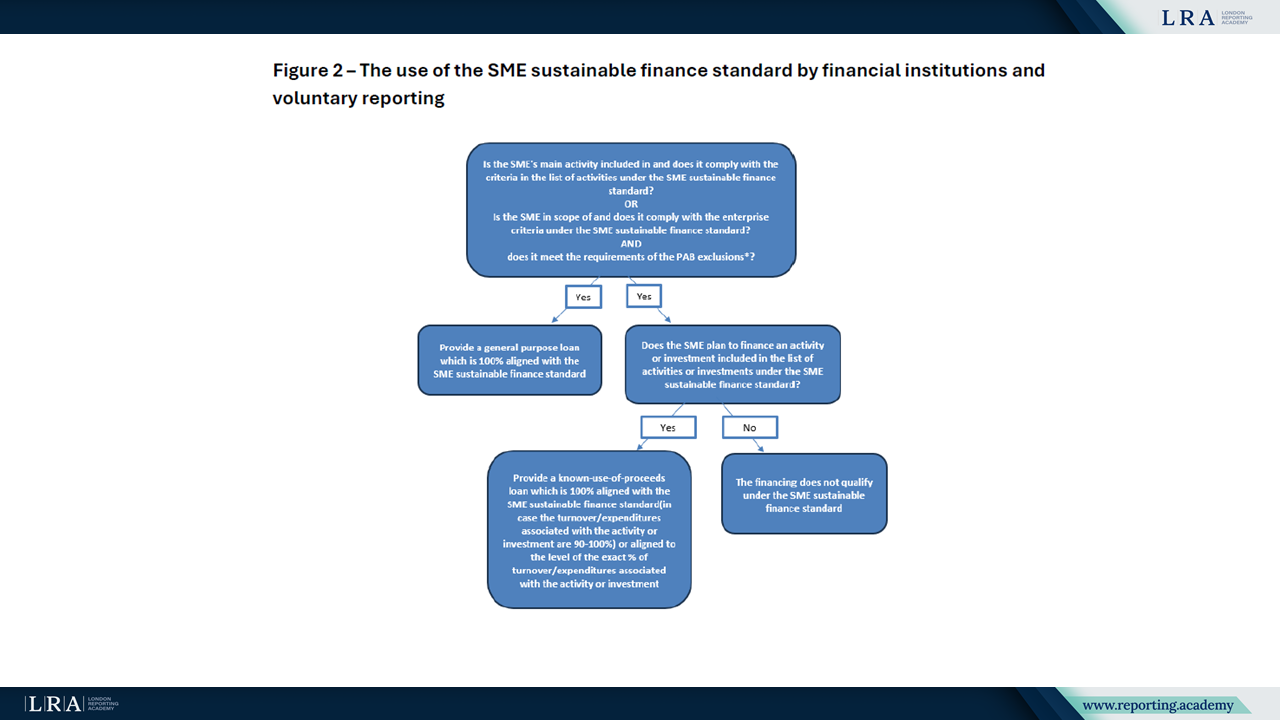

The SME Sustainable Finance Standard initially focuses on climate change mitigation and adaptation but extends beyond the activities currently covered by the EU Taxonomy. It introduces a practical framework tailored to SME capacities and is structured around three eligibility areas:

- Activities – Activities listed in the Taxonomy Climate Delegated Act, along with additional activities not currently included, provided they are supported by well-recognised environmental labels and certifications from a pre-defined European Commission list, serving as proxies for demonstrating climate-related sustainability performance.

- Enterprises – SMEs demonstrating climate-aligned business practices, either by integrating climate considerations into their business model or by holding a recognised climate-related certification from a pre-defined list.

- Investments – Projects and measures targeting Taxonomy-listed activities as well as additional activities not currently included, provided they meet simplified and robust eligibility criteria.

Source: Streamlining Sustainable Finance for SMEs

To improve usability for SMEs, the standard proposes simplifying the Taxonomy’s technical screening criteria. Recommendations include grouping similar activities, clarifying references to EU legislation, and streamlining life-cycle assessment requirements.

The framework includes minimum safeguards that require SMEs to:

- Comply with applicable laws.

- Avoid activities excluded under the EU Benchmark Regulation for Paris-Aligned Benchmarks.

- Align voluntary reporting with a simplified indicator set, in line with the VSME standard proposed under the Omnibus package.

The standard can be used for both debt and equity financing, distinguishing between known use-of-proceeds and general-purpose finance. To ease compliance, it focuses on the SME’s main activity (accounting for 90–100% of turnover or expenditures). An online tool is also proposed to assist SMEs and financiers in applying the standard.

Source: Streamlining Sustainable Finance for SMEs

By reducing verification and reporting complexity and introducing clear classification criteria, the standard is designed to improve transparency and usability for both SMEs and financial institutions. It also encourages wider recognition of SMEs’ climate-related efforts in the broader sustainability finance ecosystem.

Next Steps

To ensure practical implementation, the Platform recommends several follow-up actions. These include the development of a dedicated online tool, modelled on existing instruments such as the EIF Sustainability Guarantee Tool and the EIB Green Checker. This tool would help SMEs assess whether their activities or investments meet the criteria of the SME sustainable finance standard. The Platform also suggests that national sustainability initiatives be considered in the tool’s design. Finally, the Platform advises extending the standard to cover the remaining four environmental objectives of the EU Taxonomy at the earliest opportunity.