U.S. Corporate Sustainability Reporting Reaches New Milestone as S&P 500 Approaches Universal Disclosure

Recent data from the Governance & Accountability Institute highlights continued momentum in corporate sustainability disclosure across both the S&P 500 and Russell 1000, pointing to strong voluntary uptake ahead of pending regulatory shifts.

Sustainability reporting among the largest publicly traded companies in the United States continued its upward trajectory in 2024, with the S&P 500 Index reaching 99% disclosure, according to the latest research from Governance & Accountability Institute. The findings demonstrate that non-financial reporting has become a standard practice for large-cap firms, even as the regulatory landscape remains in flux.

Record Levels Across Market Capitalisation Segments

The 14th edition of the annual research series tracking sustainability disclosure trends reveals that 94% of Russell 1000 companies published sustainability reports in 2024, up from 93% in 2023. The increase, whilst more modest than in previous years, extends a consistent pattern of growth that began when G&A Institute first tracked these metrics in 2011, when only 20% of S&P 500 companies reported on sustainability matters.

Source: G&A’s 2025 Sustainability Reporting in Focus

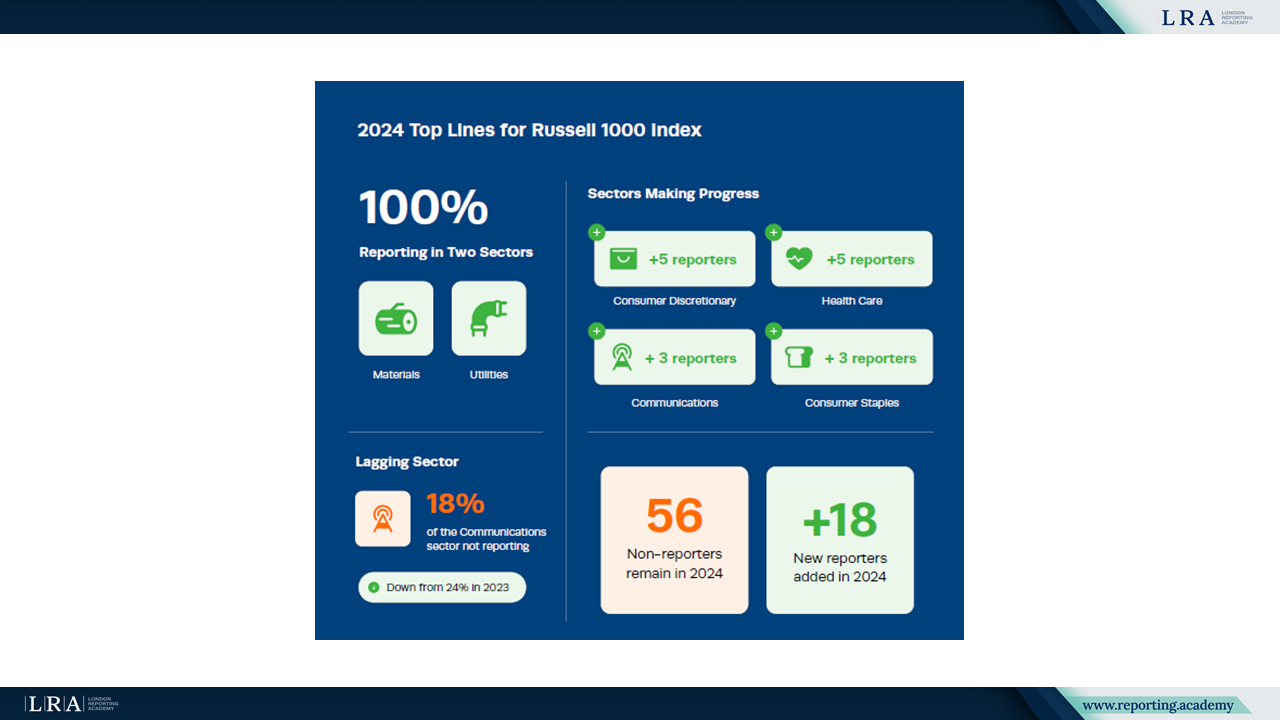

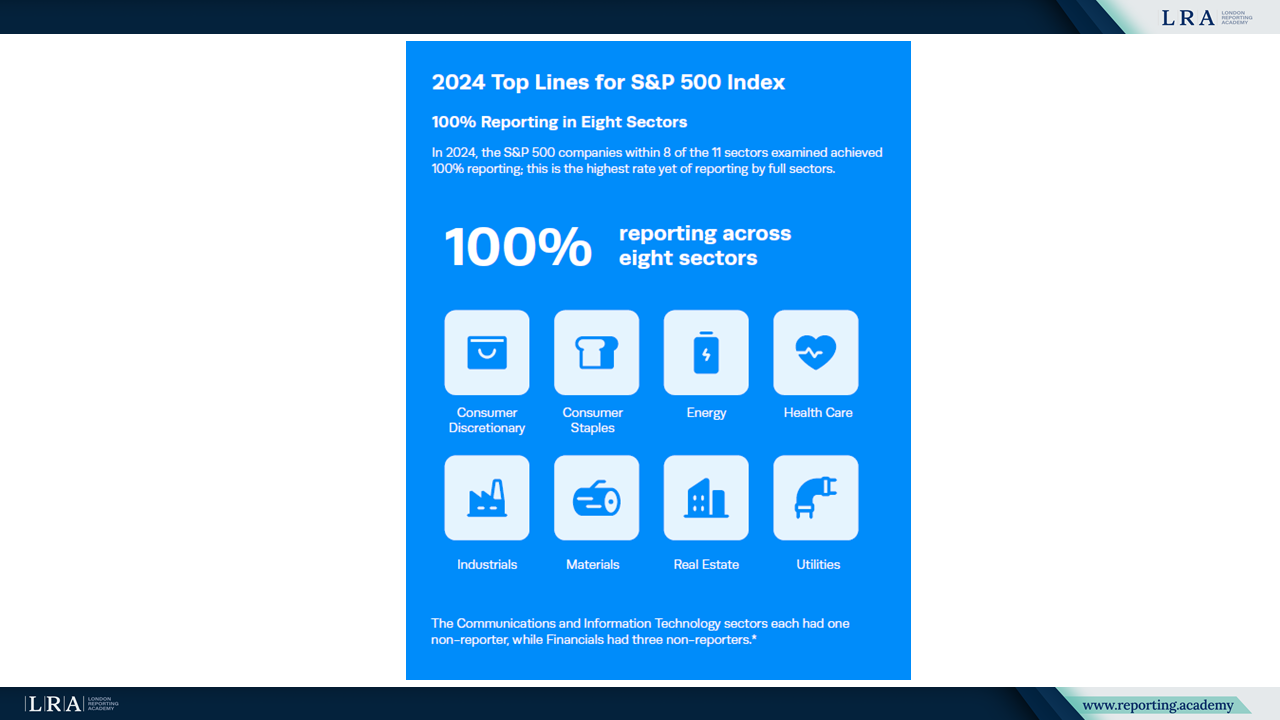

The S&P 500, which represents the largest half of the Russell 1000 by market capitalisation, saw five non-reporting companies remaining in 2024, down from seven in 2023. Eight sectors within the S&P 500 achieved 100% reporting rates. Communications and Information Technology each had one non-reporter, whilst Financials accounted for three.

Source: G&A’s 2025 Sustainability Reporting in Focus

Among smaller-cap companies in the Russell 1000, reporting reached 90% in 2024, an increase from 87% in 2023. This segment, comprising firms with market capitalisations between approximately $2.4 billion, has demonstrated notable momentum since 2018, when only 34% of these companies reported on sustainability.

Framework Adoption and Disclosure Practices

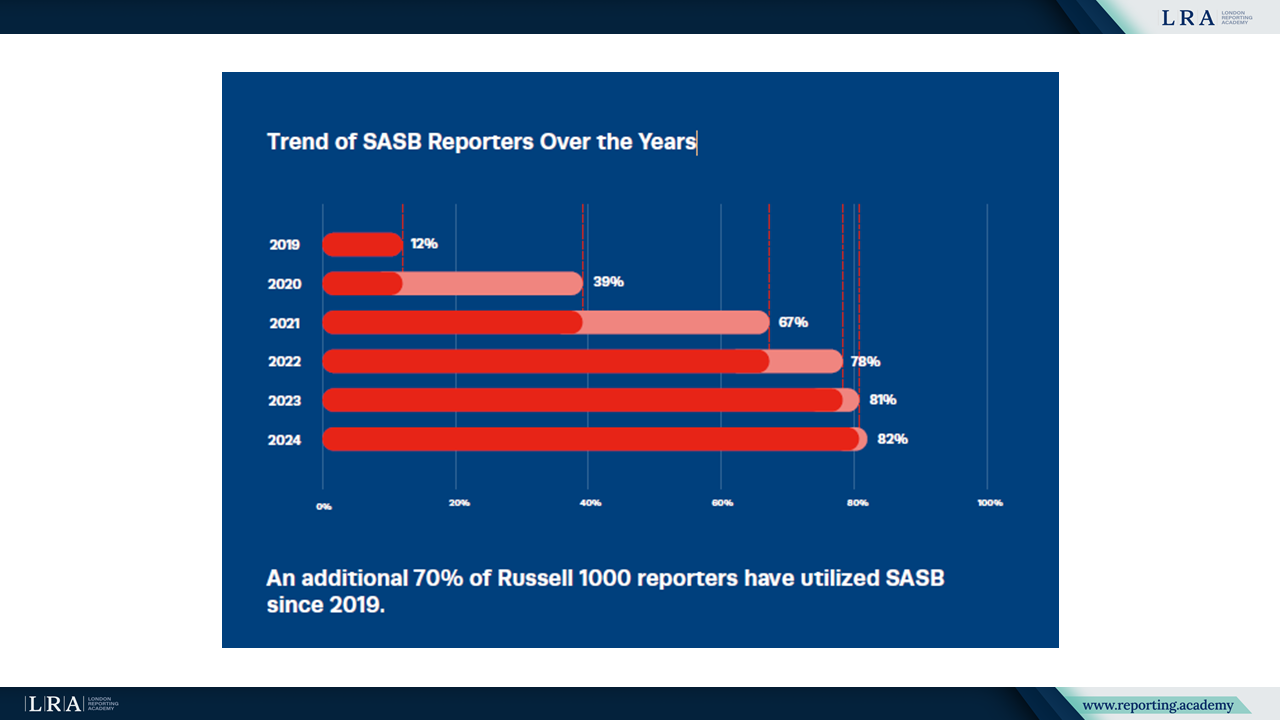

SASB Standards remained the most widely utilised reporting framework across the Russell 1000, with 82% of reporting companies aligning with these standards in 2024. This marks the fourth consecutive year that SASB has held this position. The Sustainability Accounting Standards Board (SASB) Standards, now consolidated under the International Sustainability Standards Board (ISSB) Standards, focus on financially material sustainability information across 77 industries.

Source: G&A’s 2025 Sustainability Reporting in Focus

Alignment with the Task Force on Climate-related Financial Disclosures (TCFD) increased to 65% of Russell 1000 reporters, up from 60% in 2023. However, the rate of growth has slowed compared to previous years. The Global Reporting Initiative (GRI) Standards maintained steady adoption at 55%, unchanged from 2023.

The research also tracked emerging frameworks for the first time. ISSB Standards, which became effective in January 2024, were adopted by 17% of Russell 1000 companies. The European Sustainability Reporting Standards (ESRS), primarily designed for companies subject to the Corporate Sustainability Reporting Directive (CSRD), were voluntarily implemented by 6% of reporting companies.

Assurance and Climate Disclosure Trends

External assurance for sustainability disclosures continued to expand, with 51% of Russell 1000 reporters obtaining third-party verification in 2024. This represents more than double the 24% recorded in 2019. Among S&P 500 companies, 68% utilised external assurance, whilst 32% of smaller Russell 1000 companies did so.

Climate-related disclosure through CDP questionnaires remained relatively stable, with 57% of Russell 1000 companies responding to the CDP Climate Change questionnaire in 2024. The CDP Water Security module recorded the largest increase, with 41 additional companies participating compared to 2023.

Nature-related disclosure remained limited, with only 1% of Russell 1000 companies applying the Task Force on Nature-related Financial Disclosures Recommendations (TNFD) in 2024. This low adoption rate reflects the nascent stage of biodiversity and ecosystem reporting frameworks.

Sector Variations and Sustainable Development Goals

Sector-level analysis revealed significant variations in reporting practices. The Materials and Utilities sectors maintained 100% reporting rates, whilst Communications remained the sector with the lowest coverage at 82%.

Alignment with the United Nations Sustainable Development Goals (SDGs) remained consistent, with 55% of Russell 1000 reporters referencing specific SDGs in their disclosures. Goal 13 on Climate Action, Goal 8 on Decent Work and Economic Growth, and Goal 12 on Responsible Consumption and Production were the most frequently cited targets.

The research indicates that voluntary sustainability reporting has evolved into an established practice among large U.S. companies, with disclosure rates approaching saturation in the S&P 500. As mandatory reporting requirements begin implementation in California in 2026 and companies prepare for potential international obligations, the infrastructure for comprehensive sustainability disclosure appears well established within the Russell 1000 universe.