The EU Platform on Sustainable Finance Publishes Report on Key Recommendations to Simplify the EU Taxonomy

The EU is reforming its taxonomy to reduce bureaucratic burden and make sustainable finance more accessible. New principles for assessing Do No Significant Harm (DNSH), Key Performance Indicators (KPIs), and Operating Expenses (OpEx) will streamline reporting for businesses, while banks and investors will gain more accurate data on green assets. Clear standards will ensure disclosure without legal risks, enhancing transparency and directing capital towards sustainable projects.

On 5th February 2025, the EU Platform on Sustainable Finance published a detailed report with key recommendations aimed at simplifying and optimising the EU Taxonomy. The goal of these proposals is to enhance the accessibility and efficiency of reporting processes in sustainable finance, especially for various types of organisations, such as small and medium-sized enterprises (SMEs), banks, and investors.

Read the report Simplifying the EU Taxonomy to Foster Sustainable Finance for more details.

Clarification of the "Do No Significant Harm" (DNSH) Assessment

The Platform aims to simplify and clarify the "Do No Significant Harm" (DNSH) assessment by tailoring requirements based on an organisation's type (financial or non-financial), application scope (turnover or capital expenditure), and location (EU or non-EU). To ease compliance, it recommends applying the "comply or explain" principle to activities where DNSH evaluation is particularly complex, pending a full review of the criteria in the Delegated Acts on Climate and Environment.

However, this approach will not extend to ongoing environmental obligations, such as greenhouse gas emissions or water body conservation, nor to cases where non-compliance could cause lasting harm, such as assets in protected areas. In such instances, organisations must specify unmet criteria and justify their non-fulfilment, informing future policy revisions.

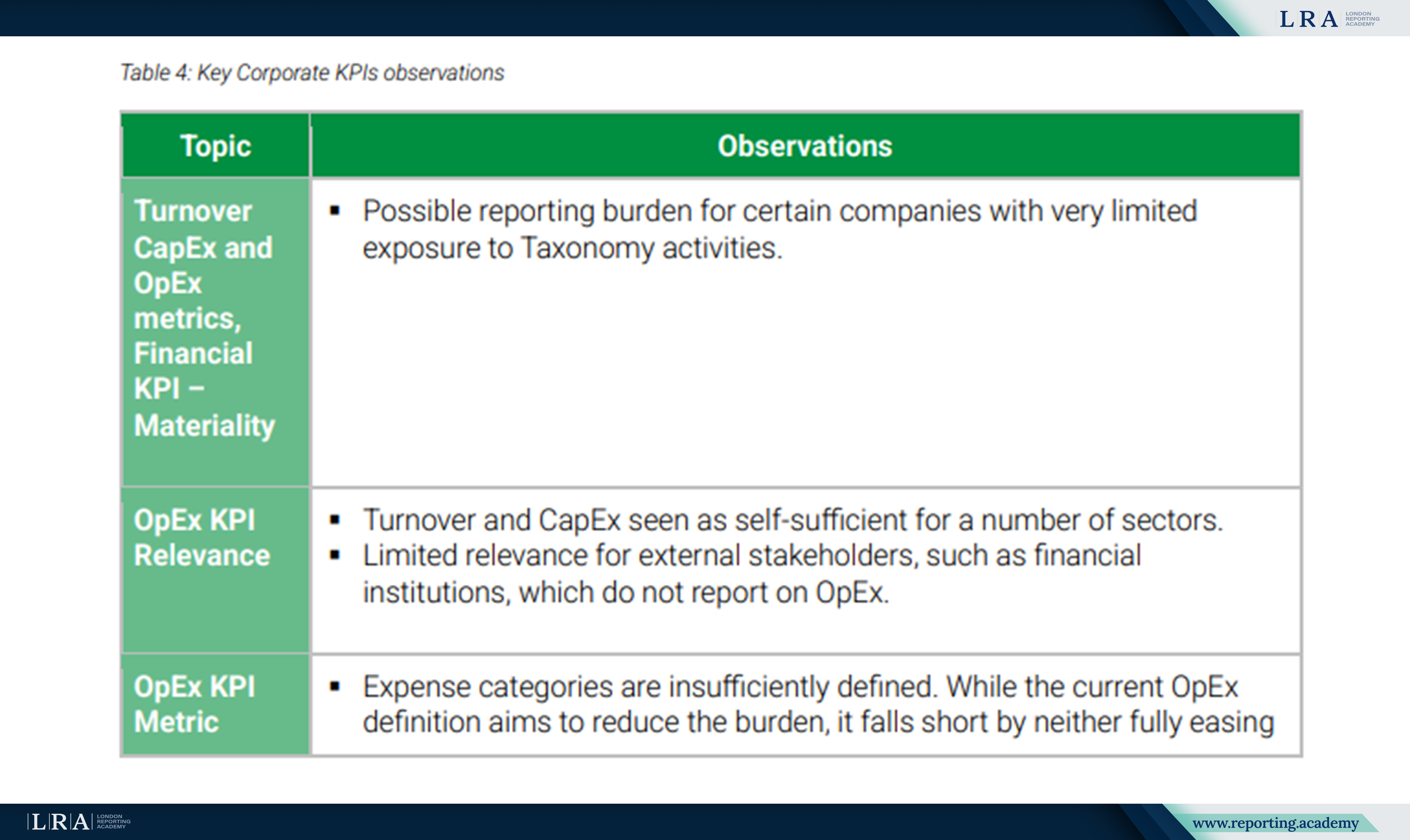

Introduction of Materiality Principles and Simplification of KPI Assessment

The next key step is introducing materiality principles for all organisations. This involves setting thresholds for key performance indicators (KPIs) and simplifying the DNSH assessment for turnover-related KPIs. The Platform expects that applying materiality principles will help focus on the most significant aspects of sustainable activity, making assessment and reporting more straightforward.

Source: Report Simplifying the EU Taxonomy to Foster Sustainable Finance

Clarification of KPI Calculations Related to Operating Expenses (OpEx)

The Platform recommends clarifying KPI calculations for operating expenses (OpEx) to improve accuracy and reduce unnecessary reporting. It suggests limiting mandatory R&D disclosures to focus on key sustainability aspects rather than nominal costs.

These recommendations are based on an August 2024 survey conducted with European companies under the CSRD framework, in collaboration with Business Europe and CSR Europe. The Platform also proposes aligning financial and non-financial reporting segmentation under the CSRD for consistency.

For high-risk sectors, additional guidance may be provided on reporting adaptation-related OpEx, such as accident insurance. In these cases, materiality thresholds should balance transparency with proportionality while minimising reporting burdens.

Clear Principles for Reporting in the Financial Sector

The report places particular emphasis on the importance of creating clear principles for financial sector reporting in the context of the EU Taxonomy. This will allow financial organisations to disclose data with confidence, knowing that they will not face legal risks, which will increase trust from investors and regulators. The introduction of "safe harbours" will help set the framework for safe and accurate data disclosure, thereby strengthening sustainable finance within the EU.

The report also highlights the need for developing standards that consider the needs of various market participants, including SMEs. Simplifying requirements and providing clear reporting instructions will improve the interface between the taxonomy and financial reporting, which will in turn increase data transparency and reliability. This will help channel capital flows into projects that align with sustainable development goals and stimulate the transition to a more sustainable and environmentally-oriented economy.

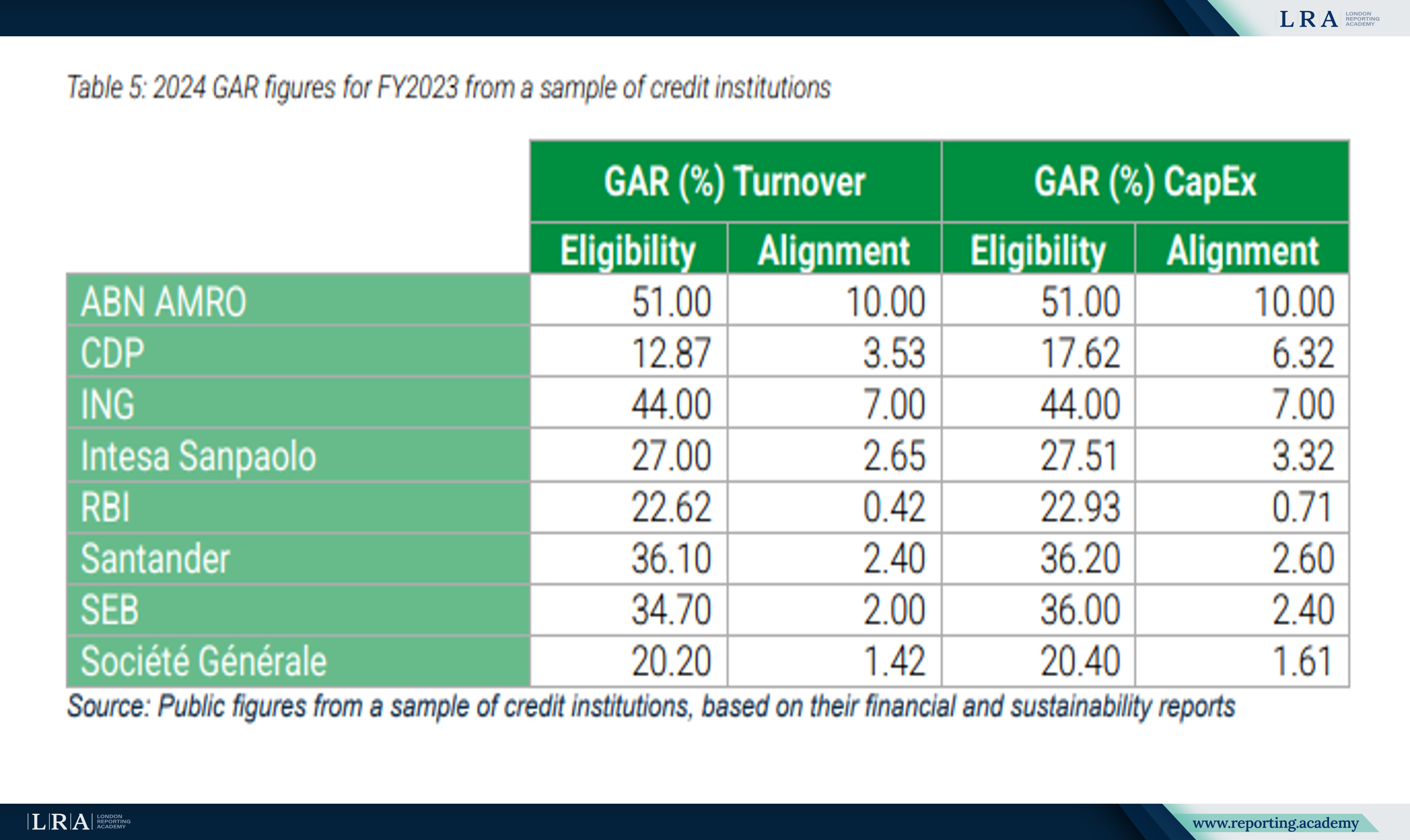

Expanding the Use of Proxy Assessments for Assets

The Platform proposes expanding the use of proxy assessments for assets that meet the Green Asset Ratio (GAR) and Green Investment Ratio (GIR) thresholds. These disclosures allow banks to assess and explain the environmental quality of their balance sheets, which helps attract environmentally conscious clients and investors. The goal of these disclosures is to increase the transparency of green assets in banks' balance sheets, which should lead to capital cost advantages for operations aligned with the EU Taxonomy.

However, the Platform noted that the current GAR disclosures do not always achieve their goal. Limitations in the reporting process were identified, which hinder comparability and effective functioning. To address this, the Platform has established a GAR working group that studied proposals for improving the process based on the experiences of credit institutions.

Source: Report Simplifying the EU Taxonomy to Foster Sustainable Finance

Support for SMEs, Banks, and Investors

The report emphasises the importance of supporting SMEs, as well as banks and investors, in integrating the EU Taxonomy. Given the limited resources of SMEs, flexible reporting mechanisms are suggested that will allow small companies to integrate sustainable practices without significant costs. The report also proposes the creation of accessible tools for banks and investors to ease adaptation to the standards and stimulate the market for sustainable financial products.

Conclusion

The EU Platform on Sustainable Finance's recommendations are crucial in simplifying the EU Taxonomy reporting process, reducing administrative burdens, and enhancing accessibility for all organisations, including SMEs. By introducing clear guidelines and materiality-based KPIs, the proposed changes will make it easier for businesses to integrate sustainability practices, while also reducing reporting pressure, particularly for smaller companies with limited resources.

For financial institutions and investors, the recommended adjustments to the Green Asset Ratio (GAR) will improve transparency and accuracy in assessing green assets. This should reduce the cost of capital for sustainable investments, fostering greater confidence in the market.

Ultimately, these changes will accelerate the EU’s transition to a greener economy, ensuring that sustainability efforts are more inclusive and aligned with the EU's long-term goals. The recommendations will make reporting more efficient and support the flow of investment into sustainability-driven projects.