Singapore Extends Timelines for Climate-Reporting Requirements

Singapore has announced updated deadlines for climate-related disclosures, marking an important adjustment in the country’s reporting landscape.

On 25 August 2025, Singapore’s Accounting and Corporate Regulatory Authority (ACRA), together with Singapore Exchange Regulation (SGX RegCo), announced revised implementation timelines for climate reporting, including external assurance. This policy shift applies to both listed companies and large non-listed companies (Large NLCos). The regulators highlighted ongoing global economic uncertainties and varying levels of organisational readiness as key reasons for this extension.

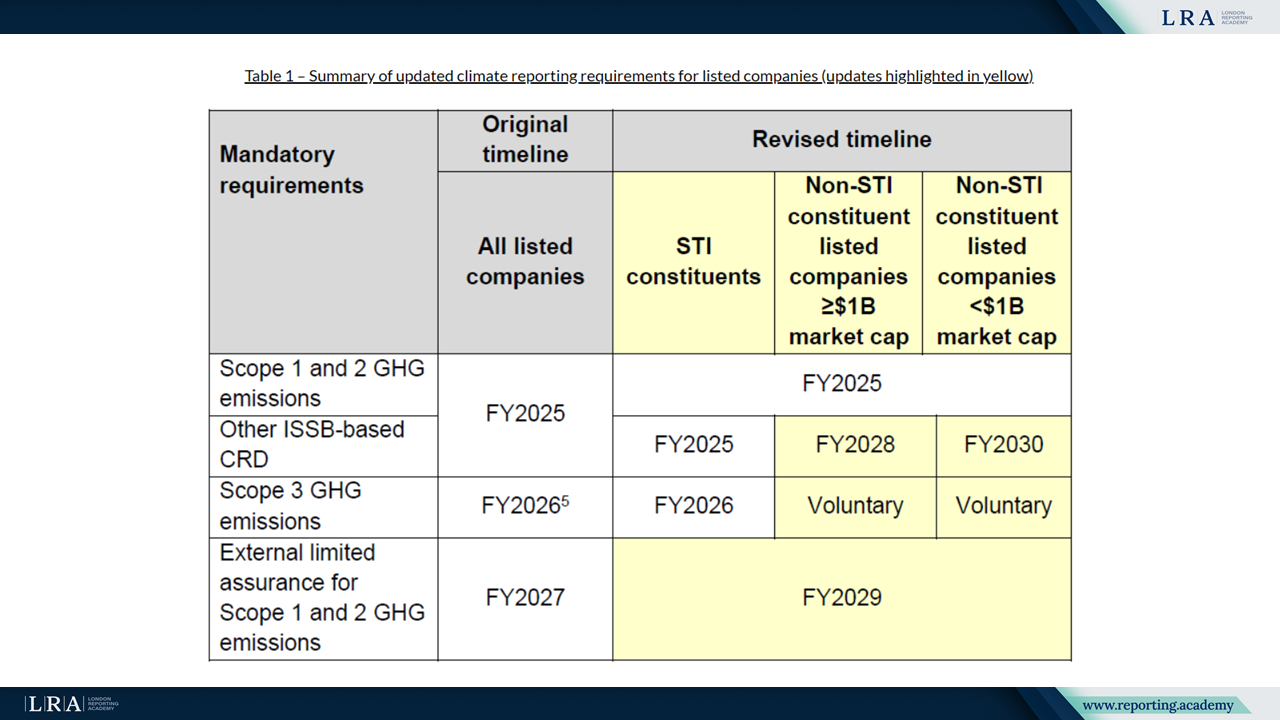

Key Requirements for Listed Companies

In their announcement, ACRA and SGX RegCo explained that the requirements will be applied differently to Straits Times Index (STI) constituents and to non-STI listed companies, with further segmentation based on market capitalisation. Under the revised schedule, Scope 1 and Scope 2 greenhouse gas emissions reporting remains mandatory from FY2025 for all listed companies. Scope 3 GHG emissions reporting will apply from FY2026, but only for STI constituents, while for non-STI companies the disclosure remains voluntary until further notice. Other ISSB-based Climate-Related Disclosures (CRD) are required from FY2025 for STI constituents. For non-STI companies with a market capitalisation of at least $1 billion, the requirement will commence in FY2028, while those below $1 billion will begin in FY2030. External limited assurance on Scope 1 and 2 emissions, initially planned for FY2027, has been deferred to FY2029 for all listed companies.

The comparative overview of original and revised timelines is shown below:

Source: The Accounting and Corporate Regulatory Authority (ACRA) press release

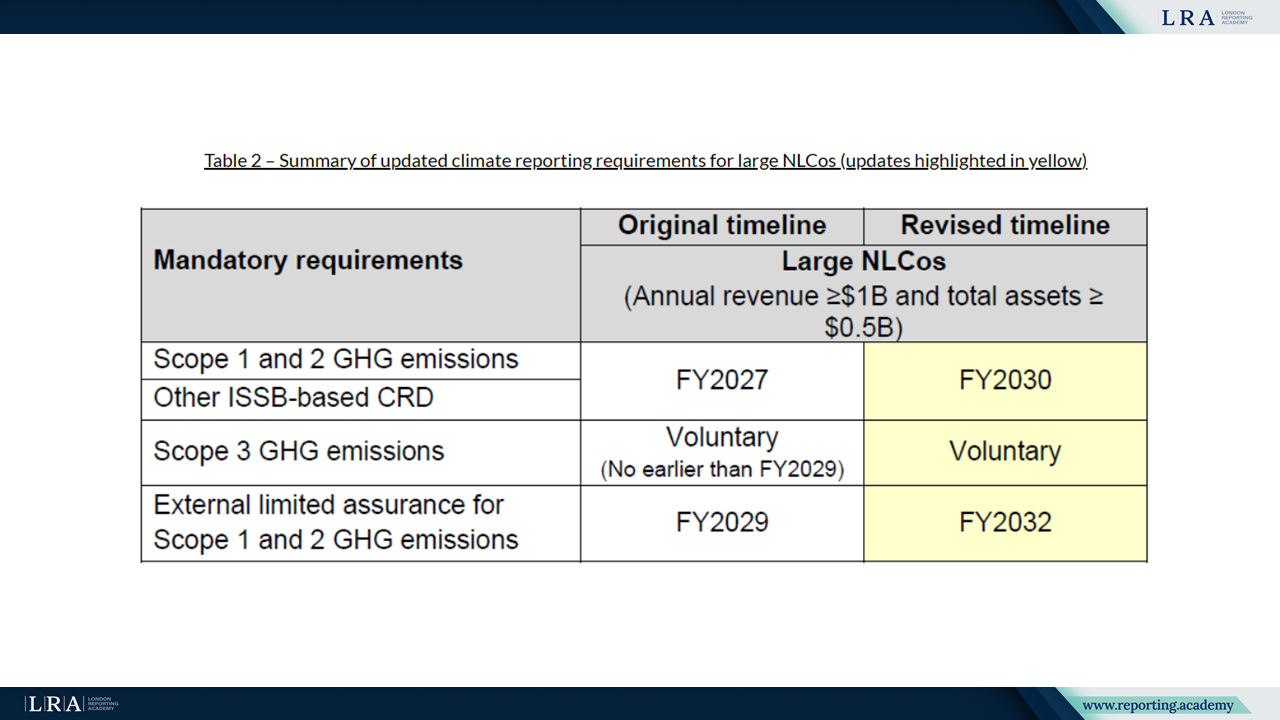

Updated Timelines for Large Non-listed Companies

Large NLCos, defined as companies with annual revenue of at least $1 billion and total assets of at least $0.5 billion, also face extended deadlines. For this category, Scope 1 and 2 GHG emissions reporting, together with other ISSB-based CRD, will begin only in FY2030. Scope 3 disclosures remain voluntary, and external limited assurance for Scope 1 and 2 emissions has been pushed back to FY2032.

The changes are summarised below:

Source: The Accounting and Corporate Regulatory Authority (ACRA) press release

Conclusion

Companies may also rely on the Sustainability Reporting Grant (SRG) offered by the Singapore Economic Development Board (EDB) and Enterprise Singapore (EnterpriseSG) to strengthen their preparation for ISSB-based CRD ahead of mandatory compliance. The deadlines for SRG applications have been adjusted to reflect the revised reporting timelines.

Singapore’s revised climate reporting framework reflects a pragmatic balance between advancing sustainability disclosure standards and accommodating diverse levels of corporate readiness. The updated approach ensures progressive alignment with ISSB standards, while giving companies additional time to prepare robust systems for data collection, reporting, and assurance.