SB 253 in California: Gradual Implementation for Greater Impact

For the Climate Corporate Data Accountability Act (SB 253), which was initially passed in 2023, a postponement in implementation was introduced due to challenges faced by businesses in meeting the new reporting requirements. The California Air Resources Board (CARB) stated that it will not impose penalties on entities subject to the bill for incomplete reporting during the first reporting cycle, which is due in 2026.

The recent Enforcement notice from CARB, issued on 5 December, provides important guidance on the upcoming greenhouse gas emissions reporting requirements under SB 253. These updates are crucial for companies to understand as they prepare for the 2026 deadline. Companies will be expected to comply with detailed reporting rules, ensuring transparency and accountability in line with both state and international standards.

Similarly, a delay in the implementation of The Climate-Related Financial Risk Disclosure Act (SB 261) was introduced, granting companies more time to align with the updated standards for reporting climate-related financial risks. These changes reflect a broader understanding of the operational difficulties businesses face in achieving ambitious environmental transparency goals.

This move towards extended compliance timelines coincides with other important developments in the reporting landscape. Notably, Ursula von der Leyen recently announced the creation of an Omnibus initiative aimed at simplifying and harmonising regulations in the reporting field. Additionally, changes in the leadership of the U.S. Securities and Exchange Commission (SEC), which oversees climate reporting, may further influence how climate-related disclosures are enforced, potentially reshaping the broader regulatory environment for corporate sustainability.

Key Insights and Updates

SB 253 helps companies by providing a structured framework for disclosing value chain emissions and climate-related financial risks, ensuring transparency and compliance with evolving environmental standards.

Emissions Reporting Obligations and Key Compliance Considerations:

- Disclosure Requirements:

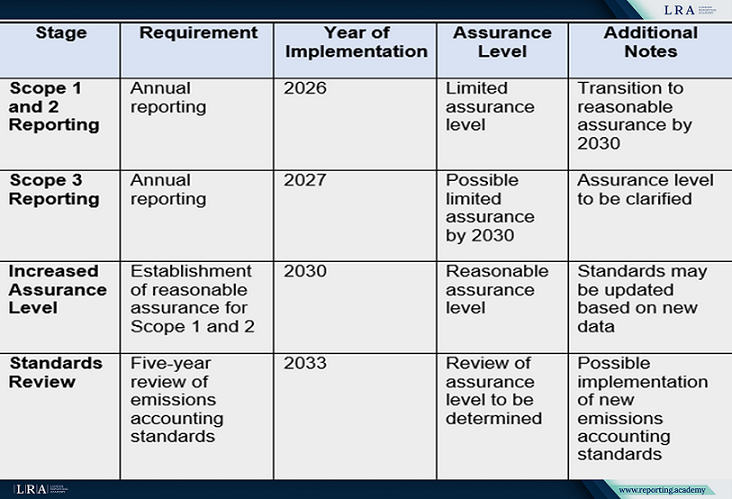

- Companies must annually report emissions data:

- Scope 1 (direct emissions) and Scope 2 (indirect emissions from purchased energy) beginning in 2026.

- Scope 3 (all other indirect emissions, including supply chains) starting in 2027. These disclosures must be submitted no later than 180 days after Scope 1 and Scope 2 data for the prior year.

- Reports must align with international standards, such as the Greenhouse Gas Protocol.

- Companies must annually report emissions data:

- Verification of Reports:

- From 2026, companies must conduct independent assurance for Scope 1 and 2 emissions at a limited assurance level, advancing to a reasonable assurance level by 2030.

- For Scope 3, limited assurance may also be introduced by 2030.

- Standards Review:

- Beginning in 2033, a five-year review of available emissions accounting standards will take place. New rules may be implemented if more effective standards emerge.

- Transitional measures:

- CARB will allow companies to use existing data collection processes during the first year of reporting and will not impose penalties for incomplete reports, provided that the requirements are met in good faith.

- Flexibility for Businesses:

- The law considers mergers, acquisitions, and other structural changes that could affect reporting. Provisions are in place to minimise duplicative efforts for businesses already reporting similar data in other jurisdictions.

Table: Key Timelines and Stages of SB 253 Implementation

Smoother Transition with CARB’s Flexible Approach

Acknowledging the operational challenges businesses face, CARB has introduced measures to ease the initial compliance burden. In the first year of reporting, companies can rely on data already collected or available, provided they demonstrate a genuine effort to align with the law’s objectives. Additionally, no penalties will be applied for incomplete data during this period, offering businesses breathing room to adapt.

Balancing Ambition with Feasibility

Gavin Newsom, California Governor, had previously expressed concerns about the feasibility of the original timelines, suggesting a delay in implementation. While this adjustment was not included in the final bill, CARB’s flexible enforcement approach reflects an understanding of these challenges, encouraging a collaborative pathway to compliance.

Source: Climate Corporate Data Accountability Act (SB 253)

Implications for Businesses

For businesses, SB 253 represents both a challenge and an opportunity:

- Challenges:

- Scaling up data collection and reporting processes to meet the rigorous standards;

- Engaging with value chain partners to accurately assess Scope 3 emissions.

- Opportunities:

- Enhancing corporate sustainability practices, boosting investor and stakeholder confidence;

- Establishing a competitive edge as an early adopter of comprehensive climate reporting;

- Aligning with evolving global standards for environmental accountability, potentially easing entry into other markets.

Conclusion

California’s Climate Corporate Data Accountability Act sets a new standard for climate reporting in the U.S., challenging businesses to rethink their environmental impact. While the road to compliance may seem daunting, CARB’s phased approach provides a valuable opportunity for organisations to adapt and excel. By embracing these changes, businesses can contribute to a more sustainable future while positioning themselves as leaders in environmental responsibility.