Philippine SEC Adopts PFRS S1 and PFRS S2 for Sustainability Disclosures

The Philippine Securities and Exchange Commission has adopted PFRS S1 and PFRS S2 through SEC Memorandum Circular No. 16, Series of 2025, alongside Sustainability Reporting Guidelines and an adoption roadmap for publicly listed companies and large non-listed entities. The Circular sets a phased implementation from FY 2026 onwards and outlines governance and submission requirements, as well as a timetable for external limited assurance on Scope 1 and Scope 2 greenhouse gas emissions.

The Philippine Securities and Exchange Commission issued SEC Memorandum Circular No. 16, Series of 2025, adopting the Philippine Financial Reporting Standards on Sustainability Disclosures, specifically PFRS S1, General Requirements for Disclosure of Sustainability-related Financial Information and PFRS S2, Climate-related Disclosures. The Circular states that, at the Commission En Banc meeting held on 04 December 2025, the SEC resolved to adopt PFRS S1 and PFRS S2 and approved the issuance of the Sustainability Reporting Guidelines for PLCs and LNLs, including the PFRS Adoption Roadmap.

It notes that IFRS S1 and IFRS S2 issued by the ISSB were approved by the Philippine Financial and Sustainability Reporting Standards Council (FSRSC) and then approved by the Professional Regulatory Board of Accountancy (PRBOA) on 17 October 2024 through Resolution No. 61.

Reporting Perimeter, Placement and Governance

The Circular applies to publicly listed companies (PLCs) and large non-listed entities (LNLs). PLCs and LNLs that are reporting entities under Section 17.2 of the Revised Securities Regulation Code must submit a Sustainability Report as an attachment to the annual report, while LNLs outside that paragraph must submit the Sustainability Report together with their audited financial statements. Sustainability Reports must be reviewed and approved by the board of directors prior to issuance.

From effectivity until the financial year immediately preceding mandatory adoption, PLCs continue to comply with the Sustainability Reporting Guidelines under SEC Memorandum Circular No. 4, Series of 2019, while being encouraged to commence transitioning during the intervening financial years.

Tiered Adoption Timetable and Thresholds

Beginning FY 2026, covered companies start adopting PFRS S1 and PFRS S2 under a tiered approach.

- Tier 1 applies to PLCs listed in the Philippine Stock Exchange, Inc. (PSE) with market capitalisation of more than PHP 50 billion as of 31 December 2025, adopting for financial years beginning on or after 1 January 2026, with reporting in 2027.

- Tier 2 applies to PLCs listed in the PSE with market capitalisation of more than PHP 3 billion up to PHP 50 billion as of 31 December 2025, adopting for financial years beginning on or after 1 January 2027, with reporting in 2028.

- Tier 3 applies to PLCs with market capitalisation of PHP 3 billion or less as of 31 December 2025, PLCs whose debt securities are listed solely on the Philippine Dealing & Exchange Corp. (PDEx) with no equity securities listed in the PSE, and LNLs with annual revenue of more than PHP 15 billion for the immediately preceding financial year, adopting for financial years beginning on or after 1 January 2028, with reporting in 2029.

The Circular defines market capitalisation as the market value of a PLC’s outstanding equity securities, calculated as the total number of outstanding shares multiplied by their closing or last traded prices as of 31 December 2025. The Circular also sets a separate basis for PLCs listed after 31 December 2025.

Assurance, Transition Reliefs and Exemptions

Mandatory external limited assurance on Scope 1 and Scope 2 GHG emissions by an independent assurance practitioner is required two years after initial implementation for each tier, to be conducted in accordance with ISSA 5000.

Transition reliefs are set out for limited periods, including a climate-first reporting focus, timing flexibility for submitting the Sustainability Report after publishing related financial statements, a one-year relief from comparative information, and a one-year allowance to use methods other than the GHG Protocol: A Corporate Accounting and Reporting Standard. Scope 3 GHG emissions are not required for two years for all tiers.

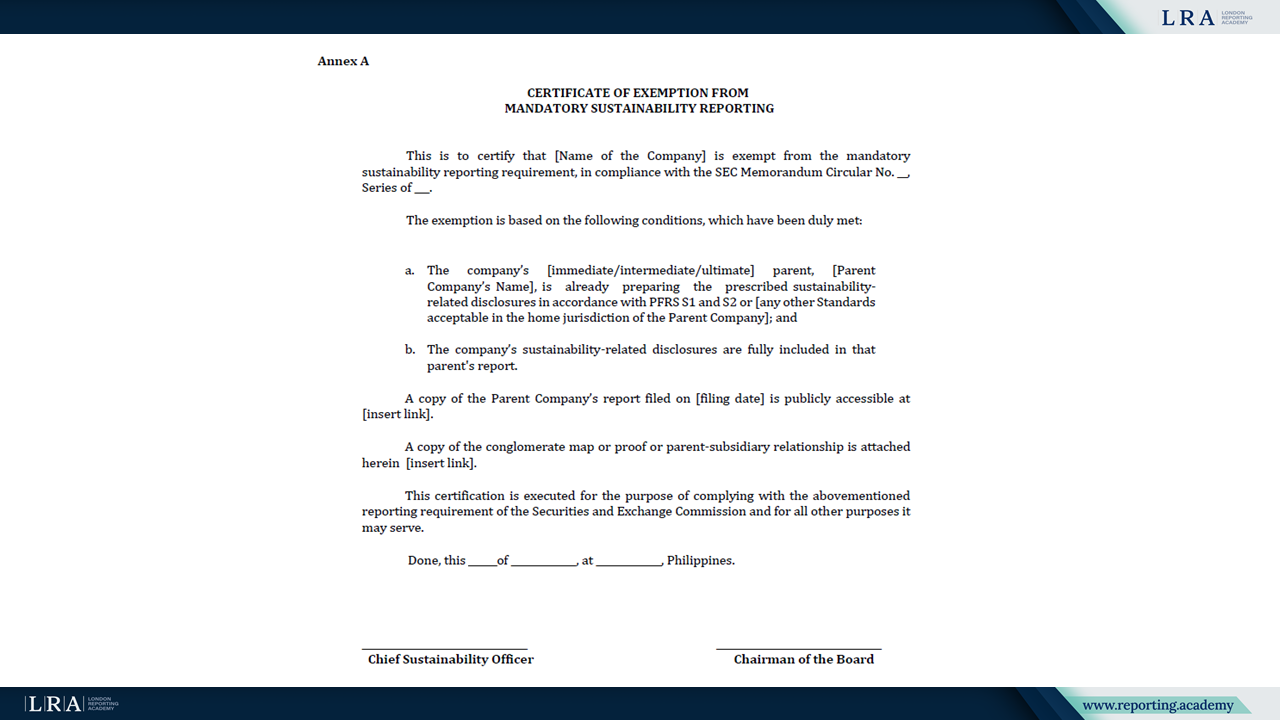

For LNLs, an exemption from mandatory submission is available when a relevant parent already prepares and files the prescribed Sustainability Report in its reporting jurisdiction, the subsidiary’s sustainability-related disclosures are included and publicly available, and the entity submits a Certificate of Exemption as an attachment to the annual financial statements.

Source: Certificate of Exemption, Memorandum Circular No. 16

Looking Ahead

The Circular signals further SEC issuances to support implementation, including additional rules and guidance on external assurance and other subsequent guidance materials. It also indicates that penalties for large non-listed entities will be addressed through subsequent Commission issuances and that the SEC may consider other cases as valid exceptions from mandatory submission.