PCAF Updates its Global GHG Accounting and Reporting Standard for the Financial Industry

Financial institutions continue to refine their approaches to measuring climate impacts, and updates to established accounting frameworks play a central role in supporting this progress. The latest revision of the PCAF Standard provides new methodological clarity and additional tools that aim to enhance the quality and consistency of greenhouse gas disclosures across lending, investment and insurance activities.

The Partnership for Carbon Accounting Financials (PCAF) has launched the 2025 update of its Global GHG Accounting and Reporting Standard for the Financial Industry. The revision reflects input from financial institutions across regions and consolidates methodological developments introduced since the release of earlier editions. The update strengthens consistency across asset classes, expands guidance for both financed and insurance-associated emissions and integrates additional recommendations informed by industry feedback, including those related to inventory fluctuation. The revised materials aim to support more transparent, comparable and decision-useful non-financial reporting.

Structure of the PCAF Standard

The Standard is structured into three parts:

- Part A on financed emissions,

- Part B on facilitated emissions

- Part C on insurance-associated emissions.

Part A has now reached its third edition, while Part C has progressed to its second edition. Part B remains under development. Together these components form the Global GHG Accounting and Reporting Standard for the Financial Industry.

The updated Part A includes new methodologies for use of proceeds structures, securitisation and structured products, sub-sovereign debt and an optional IFRS-aligned approach for undrawn loan commitments. The update also incorporates improvements informed by feedback on the Inventory Fluctuation discussion paper.

Source: PCAF_PartA_2025_V3

Expanded Coverage of Asset Classes in Part A

The 2025 edition of Part A expands the scope of the standard through four new methodologies for use of proceeds structures, securitisations and other structured products, sub-sovereign debt and an optional approach for undrawn loan commitments consistent with IFRS S1 and IFRS S2. Existing methodologies for listed equity and corporate bonds, business loans and unlisted equity, project finance, commercial real estate, mortgages, motor vehicle loans and sovereign debt remain central and have been further clarified.

An infographic in the standard illustrates the expanded asset class landscape and shows how the ten categories are mapped across corporate finance, project financing and real economy exposures.

Source: PCAF_PartA_2025_V3

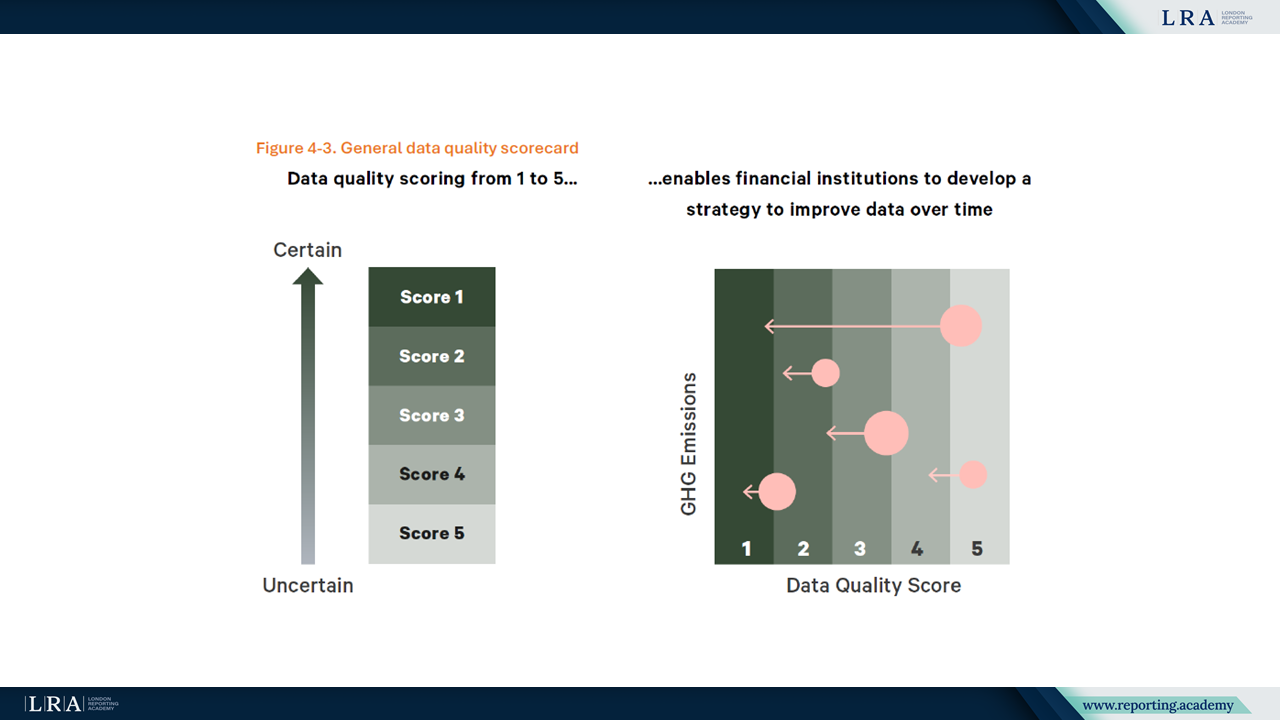

The revised Part A strengthens attribution rules and refines the expectations for data quality. The five-level data quality scale continues to guide institutions in assessing source reliability and methodological transparency. The update also introduces clearer expectations regarding inventory fluctuation and how institutions should explain changes in portfolio emissions. A visual data quality scorecard provides a structured summary of quality levels.

Source: Data Quality Scorecard, PCAF_PartA_2025_V3

Supplemental Guidance on Avoided Emissions and Forward-looking Metrics

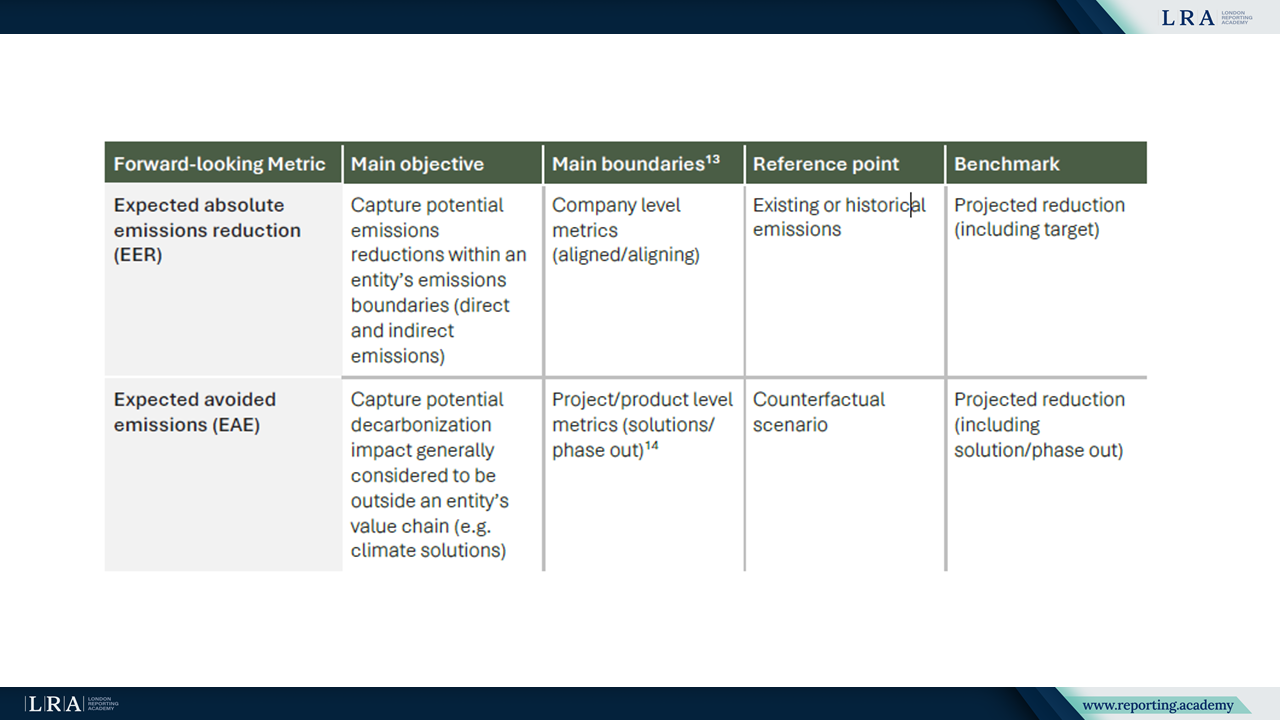

The supplemental guidance provides a structured approach to financed avoided emissions and introduces two forward-looking metrics: Expected Emissions Reductions (EER) and Expected Avoided Emissions (EAE). Financed avoided emissions represent the share of avoided emissions attributable to a financial institution when it finances climate solutions or enablers. They are reported separately and are not part of Scope 1, Scope 2 or Scope 3 accounting.

The forward-looking metrics quantify expected climate effects at the point of a transaction. EER address reductions within the counterparty’s own boundary while EAE compare projected emissions of a solution with its counterfactual scenario. The guidance requires transparent assumptions, detailed methodological reporting and annual disclosure of achieved progress. These metrics cannot replace financed emissions or be used to adjust portfolio level indicators.

The guidance also summarises the two metrics in a comparative table that outlines their respective objectives, assessment boundaries, reference points and benchmarks for projected reductions. This gives institutions a concise overview of how the metrics differ and where each may be most relevant in practice.

Source: Supplemental Guidance (2025)

Revised Methodology for Insurance-associated Emissions in Part C

The updated Part C expands the methodology for insurance-associated emissions by covering four segments: commercial insurance, project insurance, personal motor insurance and treaty reinsurance. Project insurance and treaty reinsurance are introduced for the first time in the 2025 edition. The approach applies the “follow the risk” principle, recognising that attribution in insurance is based on the portion of risk transferred to the (re)insurer rather than on capital deployed, and treats insurance-associated emissions as a separate category that should not be combined with financed emissions.

Source: PCAF_PartC_2025_V2

Insurance-associated emissions are calculated by multiplying a segment-specific attribution factor by the insured entity’s absolute Scope 1 and Scope 2 emissions and, where material and available, relevant Scope 3 emissions. The Standard sets out different attribution approaches for the four segments and introduces a dedicated data-quality hierarchy for insurance portfolios, together with guidance on managing potential double counting along primary insurance and reinsurance chains. Institutions are expected to disclose aggregated absolute emissions along with their methodological choices, attribution rules and data-quality assessments.

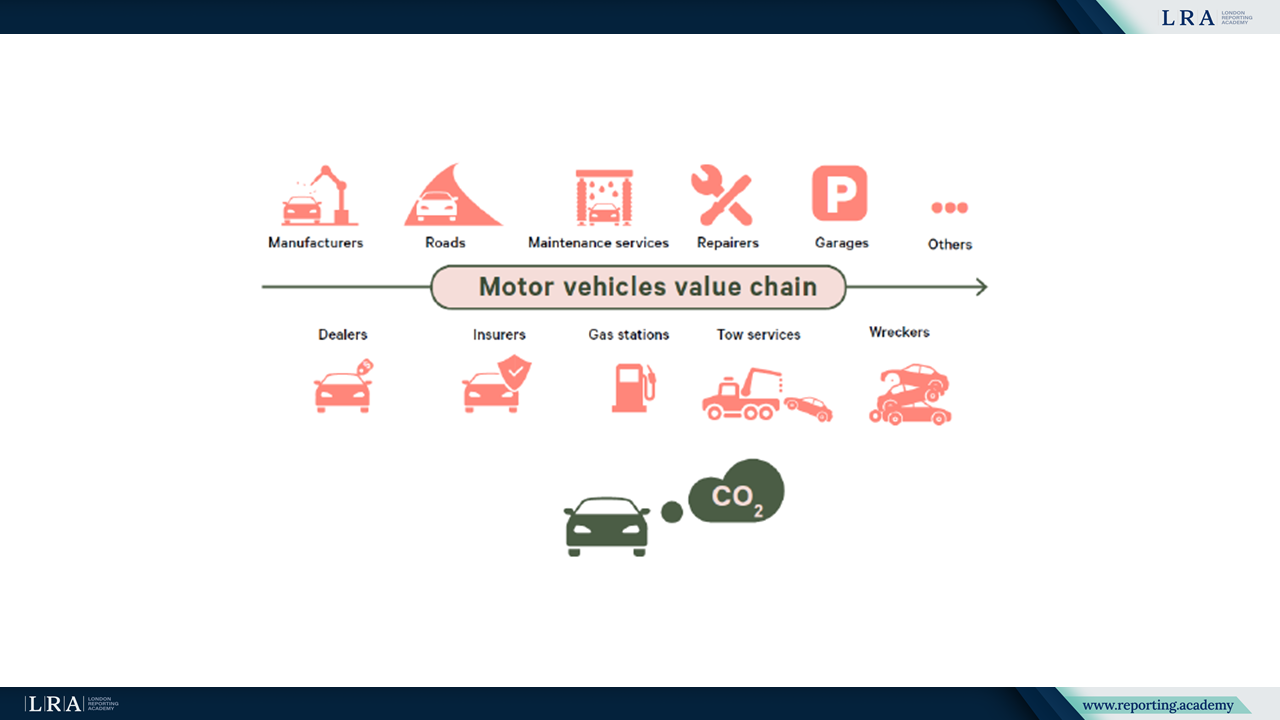

Within the four segments, personal motor insurance follows a distinct approach that reflects the characteristics of the motor vehicle value chain. The Standard illustrates this through a schematic representation of the typical stages in the value chain and the points at which insurers interact with it.

Source: Motor vehicle value chain, Source: PCAF_PartC_2025_V2

Alignment with International Reporting Frameworks

The updated standard maintains consistency with the GHG Protocol and strengthens alignment with IFRS S1 and IFRS S2. The documents support comparability of disclosures and enable integration with transition planning and climate-related risk assessment frameworks. The updates also reflect extensive stakeholder feedback and ensure consistency with broader initiatives such as those of GFANZ.

Conclusion

The 2025 update of the PCAF standard broadens the methodological foundation available to financial institutions. The inclusion of new asset classes, refined attribution principles, enhanced data quality expectations and structured forward-looking metrics supports organisations in improving the completeness and transparency of their non-financial reporting and in meeting emerging disclosure requirements.