Navigating the New Sustainability Disclosure Landscape: A Comparative Overview of ESRS, IFRS S1/S2, SEC Climate Rule, and CA SB 253/261

As sustainability becomes an increasingly critical focus for governments, investors, and key private-sector stakeholders, companies must navigate a rapidly evolving regulatory environment. The growing number of disclosure frameworks underscores the need for enhanced transparency, accountability, and consistency in sustainability reporting.

In September 2024, ERM launched a new report that provides a comprehensive analysis of these key sustainability standards and rules. It includes two detailed comparison tables: the first addressing general reporting elements, and the second focused on climate-specific requirements.

Download the full report:

This guide provides an updated comparison of key sustainability-related disclosure regulations and standards, helping businesses streamline their reporting efforts and reduce the resources required for compliance.

The regulations and standards covered include:

- CSRD / ESRS: Corporate Sustainability Reporting Directive and the European Sustainability Reporting Standards (ESRS) by EFRAG;

- ISSB IFRS S1/S2: International Sustainability Standards Board’s standards on general sustainability (S1) and climate (S2);

- SEC Rule: United States Securities and Exchange Commission’s Climate-related Disclosure Rule;

- California SB 253/261: California’s climate-related disclosure bills, focusing on greenhouse gas emissions and financial risks.

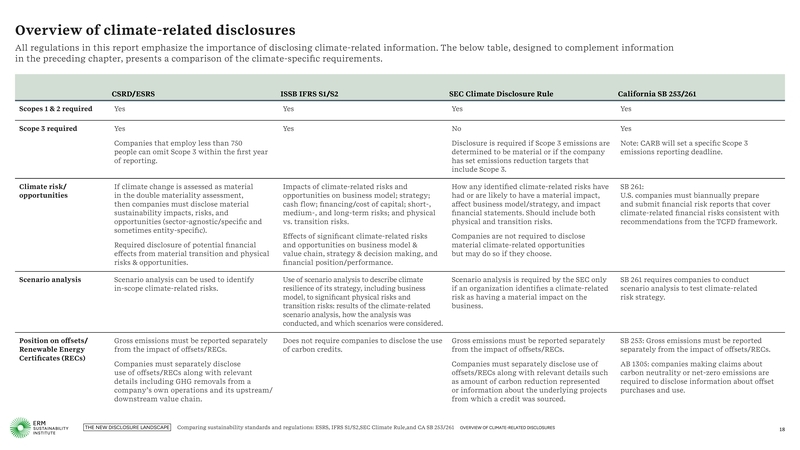

Source: ERM Report 2, Comparing sustainability standards and regulations: ESRS, IFRS S1/S2, SEC Climate Rule, and CA SB 253/261, September 2024

Key Takeaways

- Multiple Jurisdictions: The increase in climate and sustainability-related disclosure requirements across various jurisdictions means that many companies will need to comply with more than one framework;

- Efficiency in Compliance: Understanding the similarities and differences between these frameworks can help businesses streamline their disclosure processes, improving accuracy and efficiency;

- Overlapping Regulations: There is considerable overlap in the key sustainability disclosure regulations, particularly between CSRD/ESRS, IFRS S1/S2, SEC Rule, and CA SB 253/261. Aligning with one framework often leads to partial alignment with others, making compliance more manageable;

- TCFD Alignment: Most of these frameworks align with the Task Force on Climate-Related Financial Disclosures (TCFD), allowing companies to simplify their reporting efforts by adhering to TCFD’s guidelines;

- Value Beyond Compliance: Sustainability reporting should not merely be a compliance exercise. Companies can use these regulations to generate additional business value by improving their sustainability strategies and enhancing their reputation.

Key Regulations in Detail

CSRD / ESRS

Passed in late 2022, the CSRD and ESRS elevate sustainability reporting to the same rigor as financial reporting. The CSRD aims to standardize sustainability disclosures, ensuring transparency and accountability regarding corporate impacts on society and the environment. The ESRS provides detailed frameworks to guide companies in complying with CSRD, focusing on double materiality: assessing both the environmental/social impact of business activities and how these affect financial performance.

Source: ERM Report 2, Comparing sustainability standards and regulations: ESRS, IFRS S1/S2, SEC Climate Rule, and CA SB 253/261, September 2024

The CSRD applies to a broad range of companies globally, with EU-based and non-EU companies required to comply, especially if they meet certain thresholds. Additionally, sector-specific standards are under development to address the unique sustainability challenges of different industries.

ISSB’s IFRS S1/S2

The ISSB introduced its sustainability disclosure standards, IFRS S1 and S2, in June 2023. These standards aim to improve the quality and consistency of sustainability reporting, aligning ESG disclosures with financial reporting standards. The IFRS S1 covers general sustainability disclosures, while IFRS S2 addresses climate-related financial risks.

These standards will be mandatory when regulators adopt them into national reporting requirements, and jurisdictions accounting for more than half of the global economy are already aligning with the ISSB’s standards.

Source: ERM Report 2, Comparing sustainability standards and regulations: ESRS, IFRS S1/S2, SEC Climate Rule, and CA SB 253/261, September 2024

SEC Climate Disclosure Rule

The SEC’s Climate Disclosure Rule, adopted in March 2024, requires U.S. companies to disclose material climate-related risks and the financial impacts of such risks. The rule’s requirements are more limited compared to the CSRD and California’s regulations, such as the exclusion of Scope 3 GHG emissions from the SEC’s disclosures. The rule, which is still under judicial review, will apply to larger registrants starting in 2026.

California SB 253/261 and AB 1305

In 2023, California passed three major climate disclosure bills: SB 253, SB 261, and AB 1305. These laws require companies operating in California to disclose Scope 3 emissions, climate-related financial risks, and carbon credits trading information. The comprehensive nature of these laws sets them apart from other regulations, making them a model for broader U.S. compliance.

SB 253 mandates disclosure of total operational GHG emissions, while SB 261 requires companies to report on climate-related financial risks and mitigation measures. AB 1305 focuses on transparency in the voluntary carbon market, setting standards for carbon credit claims.

Upcoming Developments

- California: The California Air Resources Board (CARB) will issue more detailed regulations for SB 253 and 261, with updates expected by 2025;

- CSRD: EFRAG is developing sector-specific standards to provide more detailed reporting guidelines;

- ISSB: Ongoing work with jurisdictions to support the adoption of IFRS S1/S2 and sector-specific guidance;

- SEC: Finalization of climate-related financial disclosures, with ongoing challenges around the rule’s implementation.

Conclusion

The landscape of sustainability-related regulations continues to evolve, and businesses must stay ahead of the changes to ensure compliance. Understanding the similarities and differences between key regulations like the CSRD, ISSB’s IFRS S1/S2, the SEC Rule, and California’s SB 253/261 will be crucial for companies seeking to streamline their reporting processes, reduce compliance costs, and mitigate risks. By aligning with these frameworks, companies can not only meet regulatory requirements but also enhance their reputation, attract investment, and contribute to the global sustainability agenda.