Key Insights from Switzerland’s Proposed Updates to Sustainability Disclosure Rules

The Swiss government has unveiled new proposals to strengthen corporate sustainability-related disclosure requirements. They aim to amend Switzerland's current Climate Disclosure Ordinance, which was introduced this year. The proposals include an obligation for companies to develop ‘net zero roadmaps’ in line with Switzerland's 2050 climate target and to adopt internationally recognised standards, such as the ISSB or the EU's ESRS, for climate-related reporting. The proposed changes mark a significant step towards aligning Swiss corporate governance with global standards and expanding the scope of mandatory reporting.

Compliance Obligations and Deadlines for Swiss Climate Disclosure:

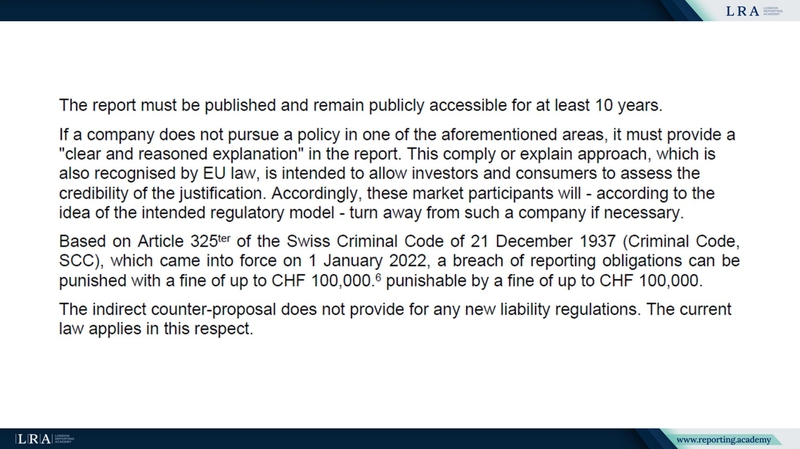

- The reports must be published and remain publicly available for at least 10 years. If a company fails to take a specific approach on any of the issues mentioned in the Climate Disclosure Regulation, it must “explain clearly and adequately” in its document;

- Failure to comply with reporting obligations may result in fines of up to CHF 100,000, as provided for in Article 325ter of the Swiss Criminal Code, which entered into force on 1 January 2022;

- The consultation period for these proposals will remain open until March 21, 2025, with the updated rules expected to take effect in 2026.

Source: Switzerland's current Climate Disclosure Ordinance, November 2022

Proposed Changes and Key Details

- Mandatory Net-Zero Plans: Companies would need to create detailed roadmaps outlining how they aim to achieve net-zero greenhouse gas (GHG) emissions by 2050, in line with the recently enacted Climate and Innovation Act. These roadmaps include:

- Interim, sector-specific science-based emissions reduction targets;

- Strategies to facilitate the transition to climate-friendly technologies;

- Financial sector-specific plans to align financial flows with the net-zero goal.

- Expanded Reporting Standards: To meet their obligations, companies can choose to align disclosures with the ISSB standards or the EU’s ESRS. This follows the incorporation of TCFD recommendations into ISSB’s framework, which has now assumed responsibility for monitoring climate disclosure progress globally.

- Broadened Scope: The threshold for companies subject to mandatory sustainability reporting would be significantly lowered, from those with over 500 employees to those with:

- 250 employees;

- CHF 25 million (€26 million) in total assets;

- CHF 50 million (€52 million) in annual sales.

- Digital Reporting Requirements: Climate reports must be submitted in a human- and machine-readable electronic format, enabling publication on international platforms for broader accessibility.

Source: Switzerland's current Climate Disclosure Ordinance, November 2022

Background and Rationale

The existing ordinance mandates reporting on GHG emissions, climate-related risks, impacts, and transition plans, based on the TCFD recommendations. This move follows earlier proposals from the Swiss Federal Council aimed at aligning domestic regulations with international frameworks, particularly the EU’s CSRD. By lowering the thresholds for mandatory reporting and aligning with global standards, Switzerland aims to ensure its companies remain competitive and transparent in the global market.

Implications for Businesses

If enacted, these updates would:

- Drive Strategic Planning: Companies will need to embed sustainability into their core strategies by developing actionable net-zero roadmaps;

- Enhance Transparency: Adoption of internationally recognised standards ensures comparability and trust among global stakeholders;

- Promote Innovation: The focus on science-based targets and climate-friendly technologies encourages companies to invest in sustainable innovations;

- Increase Compliance Scope: More businesses, especially SMEs, will be required to implement robust sustainability reporting frameworks.

Businesses operating in Switzerland should prepare to align their operations and reporting processes to meet these stringent requirements and leverage the opportunities presented by greater sustainability integration.

Takeaway

For businesses, these proposals signify an urgent need to integrate sustainability into corporate strategies, particularly in financial planning and operational processes. Early adopters of these frameworks can position themselves as leaders in the transition to a sustainable economy, gaining a competitive advantage in attracting investors, customers, and talent. The alignment with ISSB and ESRS also underscores the importance of being globally accountable and transparent, which is increasingly becoming a non-negotiable aspect of corporate governance.