Japan Publishes Schedule of Differences and Table of Concordance between SSBJ and ISSB Standards

Japan has taken a significant step toward aligning its national sustainability reporting framework with global standards. In March 2025, the SSBJ released two key reference tools designed to clarify how its newly issued standards correspond to the IFRS Sustainability Disclosure Standards.

On 31 March 2025, the Sustainability Standards Board of Japan (SSBJ) published two key documents: the Schedule of Differences and the Table of Concordance, mapping its newly issued sustainability disclosure standards against the IFRS Sustainability Disclosure Standards (ISSB Standards).

Overview and Context

Following the establishment of the International Sustainability Standards Board (ISSB), the SSBJ was created in July 2022 to develop Japan’s sustainability reporting framework and contribute to the development of international standards. On 5 March 2025, the SSBJ issued its first three Sustainability Disclosure Standards:

- Universal Sustainability Disclosure Standard “Application of the Sustainability Disclosure Standards” (the Application Standard)

- Theme-based Sustainability Disclosure Standard No. 1: General Disclosures (the General Standard)

- Theme-based Sustainability Disclosure Standard No. 2: Climate-related Disclosures (the Climate Standard)

Source: News release of 5 March 2025; SSBJ.

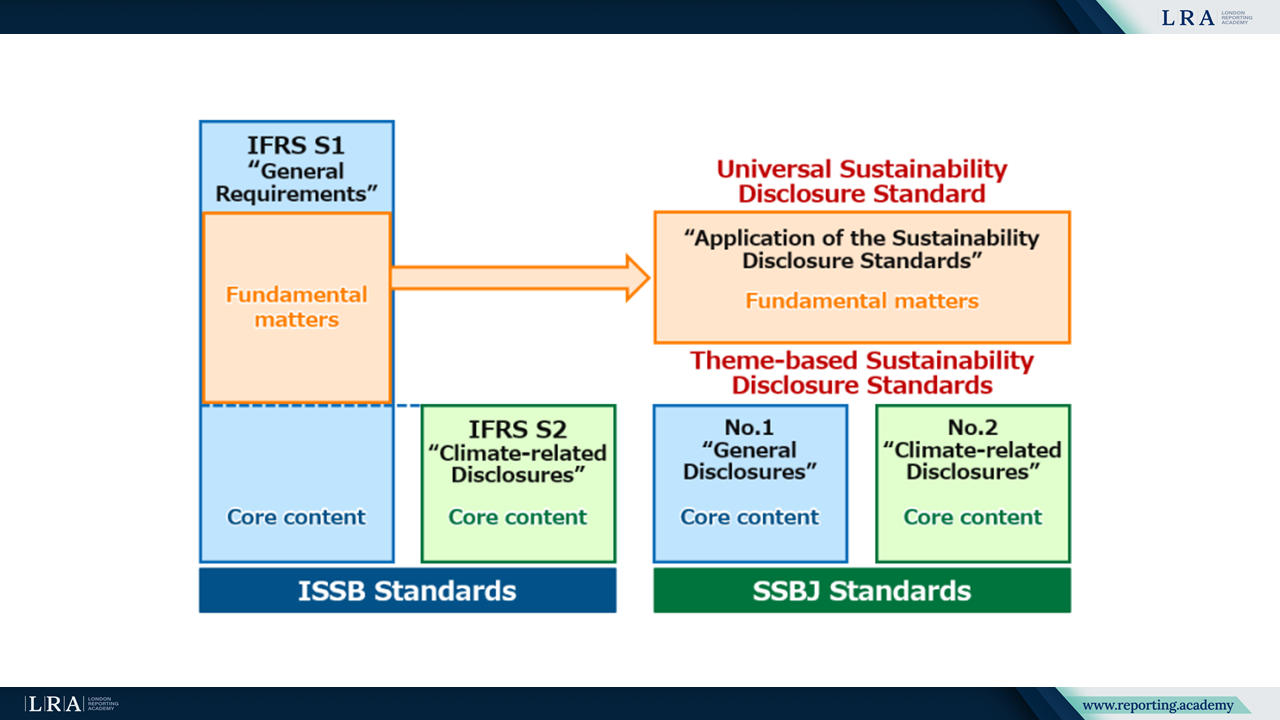

For the convenience of users, the SSBJ divided the standard corresponding to ISSB’s IFRS S1 “General Requirements for Disclosure of Sustainability-related Financial Information” into two parts. The “core content” of IFRS S1, which prescribes disclosures on sustainability-related risks and opportunities, has been incorporated into the General Standard. The remaining requirements, which detail the basic principles for preparing such disclosures, are included in the Application Standard. Despite this structural separation, the application of all three SSBJ Standards in tandem ensures consistency with the disclosure outcomes envisioned under IFRS S1.

As previously outlined, the SSBJ has now released the Schedule of Differences and Table of Concordance to facilitate adoption and provide clarity on interoperability with ISSB Standards. These tools provide practical insights into the similarities and differences between the SSBJ Standards and ISSB’s IFRS S1 and S2.

Detailed Alignment with ISSB Standards

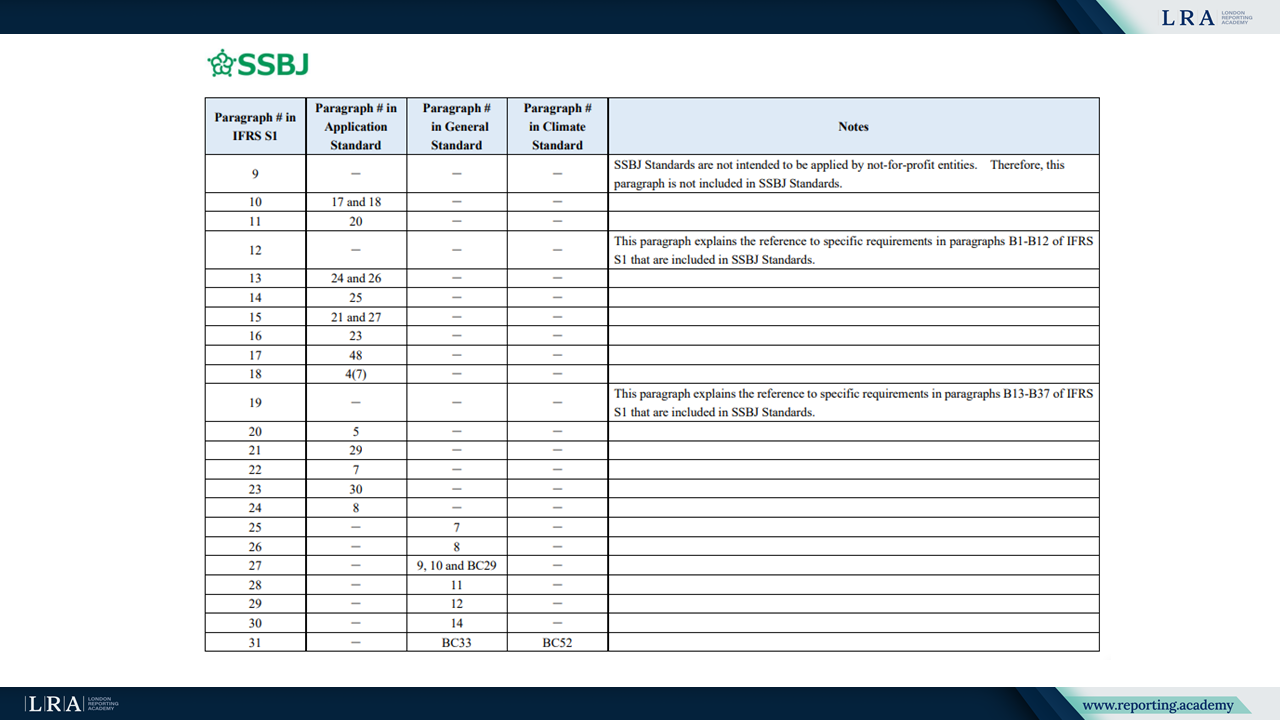

The Table of Concordance illustrates whether – and if so, where – each paragraph of the ISSB Standards is incorporated into the SSBJ Standards.

Source: The Table of Concordance; SSBJ.

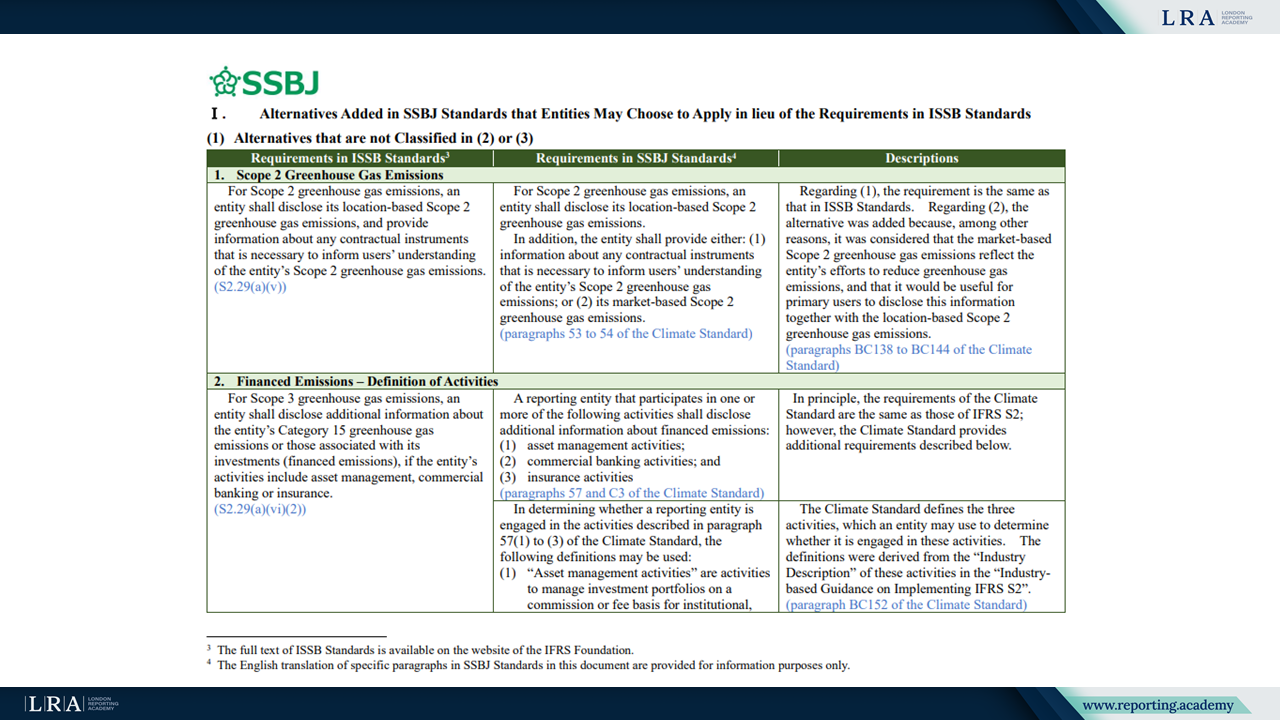

The Schedule of Differences classifies the differences between the ISSB Standards and the SSBJ Standards into two main groups:

I. Alternatives added in the SSBJ Standards that entities may choose to apply in lieu of the ISSB requirements, including:

- Alternatives that are not classified under (2) or (3);

- Alternatives provided to ensure consistency with Japanese laws and regulations;

- Alternatives designed for entities that apply the SSBJ Standards voluntarily.

II. Additional requirements introduced in the SSBJ Standards that are not included in the ISSB Standards.

The document addresses a range of topics, such as Scope 2 and financed emissions, location and timing of disclosures, comparative information, remuneration policies, and industry classification frameworks.

Source: The Schedule of Differences; SSBJ.

Notably, unlike the ISSB, the SSBJ treats its Basis for Conclusions as part of the authoritative guidance, requiring entities to take it into account for compliance purposes.

Next Steps

Currently, the SSBJ Standards do not specify the scope or timing of their application. However, they were developed under the assumption that they will eventually be mandated for companies listed on the Prime Market of the Tokyo Stock Exchange. While entities not listed on the Prime Market may also apply the standards voluntarily or in line with other regulatory frameworks, the SSBJ did not design the standards with their specific needs in mind.

Entities that adopt the SSBJ Standards without opting for the jurisdiction-specific alternatives may also assert alignment with ISSB Standards. However, applying the alternatives may not always maintain full ISSB compliance.

To ensure international comparability, the SSBJ will continue monitoring disclosures made under both the SSBJ and ISSB Standards and will consider revisions to the SSBJ Standards if necessary.