IFRS Foundation Publishes Climate Reporting Guidance

The IFRS Foundation has released new guidance that simplifies climate-related disclosures for businesses. Companies can focus solely on climate risks in the first year of applying ISSB standards, ensuring transparency and compliance. This approach not only strengthens investor confidence but also boosts market competitiveness. With these updates, reporting becomes clearer and more comparable on a global scale, enabling businesses to stay ahead in the evolving sustainability landscape.

In January 2025, the IFRS Foundation released the guidance Applying IFRS S1 when disclosing only climate-related information under IFRS S2. The document is designed to support businesses in enhancing transparency and strengthening investor confidence.

The new guidance clarifies the core requirements of the standard. It demonstrates how companies can adopt a global baseline approach to sustainability-related disclosures, integrate climate risks and opportunities into financial reporting, and align their disclosures with regulatory requirements across jurisdictions.

Overview of Educational Materials: Compliance with IFRS S1 and IFRS S2

The International Sustainability Standards Board (ISSB) actively supports companies in meeting disclosure requirements for sustainability-related risks, including climate risks. In June 2023, ISSB published its first two standards: IFRS S1 — General Requirements for Disclosure of Sustainability-related Financial Information, and IFRS S2 — Climate-related Disclosures. These standards came into effect on 1 January 2024, and their application is becoming increasingly relevant for organisations seeking to comply with global sustainability standards.

Purpose of the Educational Material

The material is intended to assist companies in understanding how to apply IFRS S1 when reporting exclusively on climate-related risks and opportunities in accordance with IFRS S2. It reflects ISSB’s transitional approach, which allows businesses to focus initially on climate-related disclosures before expanding their reporting to include other sustainability risks.

Jurisdictional and Voluntary Considerations

IFRS S1 and IFRS S2 are designed to enhance the comparability of global sustainability reporting, particularly concerning climate-related risks. As these standards are integrated into national regulations, some jurisdictions may initially require only climate-related disclosures, with plans to expand the scope in the future. Companies may also choose to adopt IFRS S1 and S2 voluntarily, focusing on climate disclosures if they wish.

The ‘Climate-first’ Approach

Recognising challenges related to data availability and organisational preparedness, ISSB has introduced a temporary relief measure. In the first year of adopting ISSB standards, companies may focus solely on climate-related disclosures. This approach allows organisations to familiarise themselves with the standards before broadening their reporting to other sustainability risks.

Under this approach, companies must disclose climate-related risks and opportunities in line with IFRS S2 while applying relevant sections of IFRS S1 that pertain specifically to climate information.

Source: The IFRS’s Guidance Applying IFRS S1 when disclosing only climate-related information under IFRS S2

Despite the limited scope of the ‘climate-first’ approach, companies that are ready may disclose broader sustainability-related risks. However, to fully comply with ISSB standards — both IFRS S1 and IFRS S2 — companies must ensure adherence to both standards.

Applicability of IFRS S1 in ‘Climate-first’ Reporting

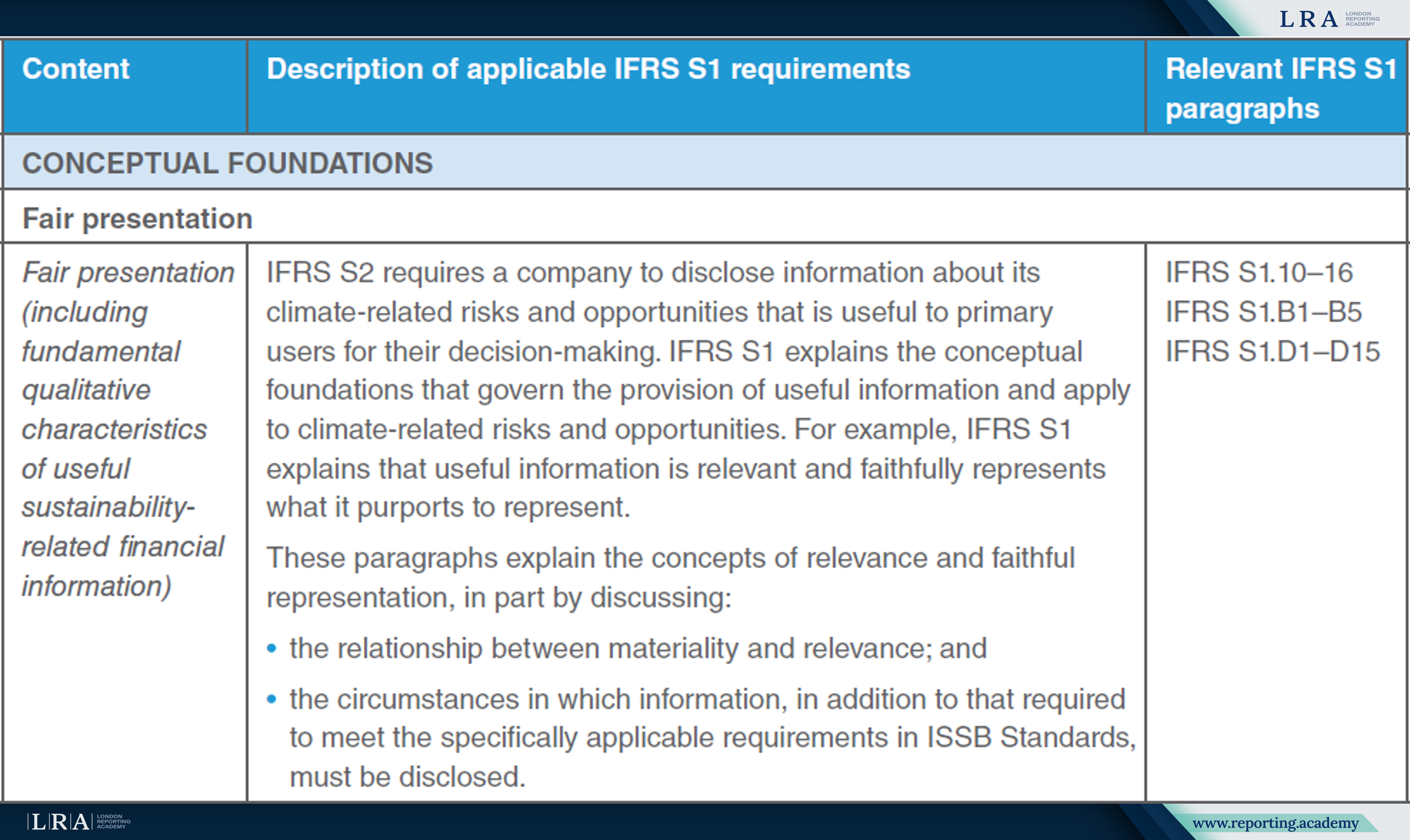

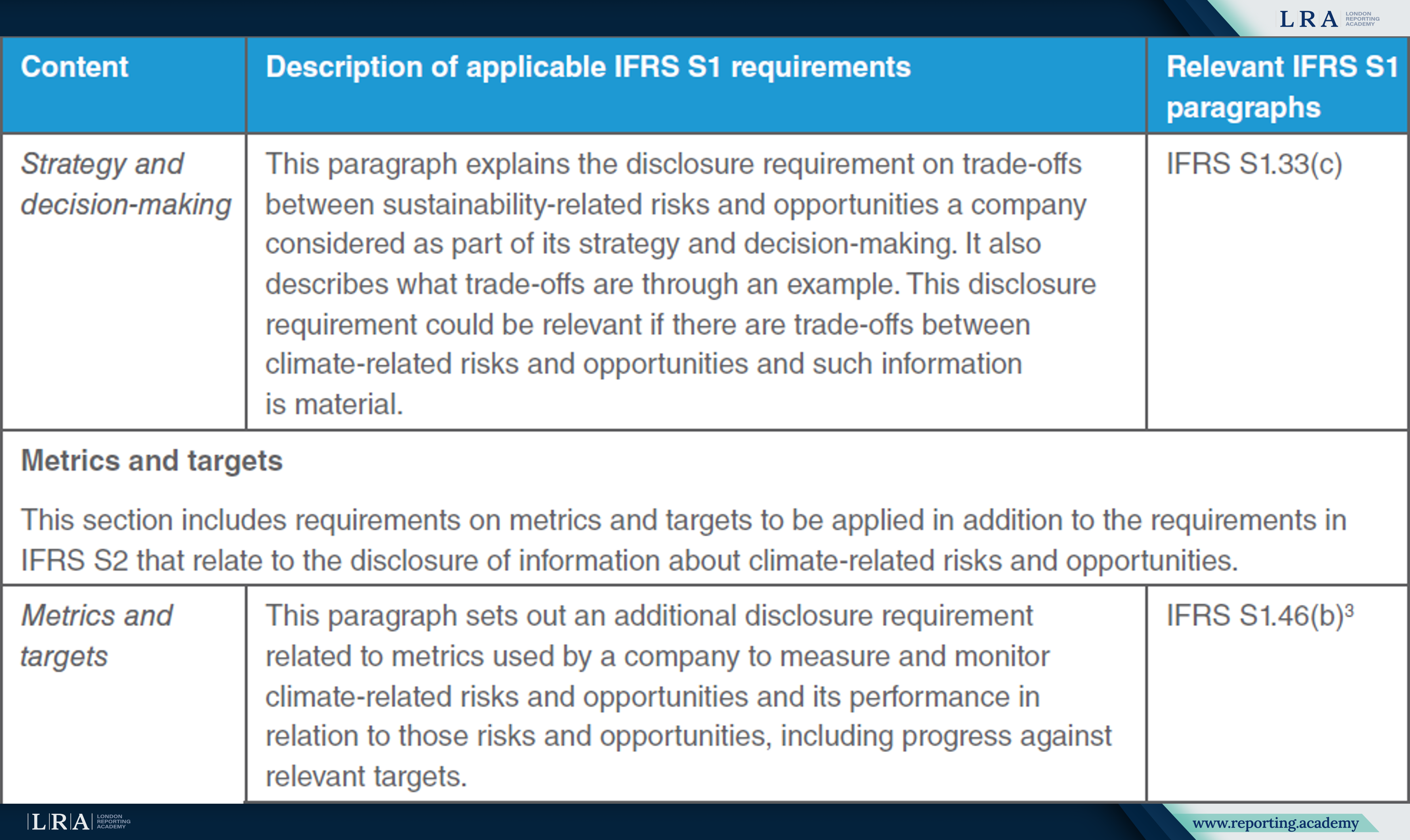

The educational material clarifies IFRS S1 requirements that must be met when a company reports exclusively on climate-related information under IFRS S2. These requirements include:

- Fair presentation – Companies must ensure that disclosed information is relevant, accurately reflects their situation, and aligns with the principles of materiality and clarity;

- Materiality assessment – Businesses must assess the significance of climate-related information in each specific case to ensure that crucial data is not omitted;

- Connected information – Companies must disclose how climate-related risks and opportunities interact with broader business strategies and financial reporting, ensuring consistency across disclosures;

- Strategy and risk management – Organisations should provide information on how their strategy and risk management approach address climate challenges, including the potential impact of these risks on operations, financial performance, and long-term outlook;

- Metrics and targets – Companies must disclose the metrics used to measure climate-related risks and opportunities, along with the targets set to manage and mitigate these risks effectively.

Source: The IFRS’s Guidance Applying IFRS S1 when disclosing only climate-related information under IFRS S2

Once these requirements are met, companies should ensure that climate-related disclosures are consistent and integrated with other elements of financial reporting. It is essential that disclosures reflect both current and long-term climate-related impacts, providing investors and stakeholders with a comprehensive view of potential risks and opportunities.

Markus Wiener, a member of the Sustainability Advisory Group at the IFRS Foundation, emphasised that adopting IFRS S2 will be a pivotal step for businesses in improving climate disclosure quality. According to him, the standard not only helps companies identify and manage climate-related risks but also lays the foundation for more informed strategic decisions, fostering long-term resilience and investment attractiveness.

Business Implications

The introduction of ISSB standards, particularly IFRS S2, requires companies to adapt their reporting practices to meet international requirements and improve transparency. The new guidance simplifies this transition by offering clear and practical recommendations that help businesses implement the standards effectively while minimising compliance risks.

For companies, aligning with ISSB standards enhances investor confidence, as transparent reporting on climate-related risks strengthens their position in financial markets and makes them more attractive to investors. The guidance also provides a structured approach and temporary relief measures, allowing organisations to adjust gradually and reduce the challenges associated with integrating climate disclosures into financial reporting. Moreover, businesses that proactively adopt ISSB standards can reinforce their reputation as responsible market participants, gaining a competitive edge in an environment where sustainability is increasingly prioritised.

As global regulators incorporate ISSB standards into national frameworks, businesses must stay ahead of these regulatory developments. The IFRS Foundation’s guidance and educational materials serve as valuable resources, helping companies not only mitigate regulatory risks but also strengthen their market standing, build investor trust, and enhance long-term competitiveness.