IFRS Foundation and TNFD Formalise Collaboration to Advance Nature-related Reporting

As global markets intensify their focus on biodiversity and natural capital, the IFRS Foundation and TNFD are advancing their efforts to align sustainability reporting. Their newly formalised partnership signals a stronger institutional commitment to integrating nature into financial disclosure frameworks, reinforcing the shift toward more holistic and interoperable sustainability standards.

On 9 April 2025, the IFRS Foundation and the Taskforce on Nature-related Financial Disclosures (TNFD) announced the formalisation of their collaboration, aiming to enhance the quality and consistency of nature-related disclosures in global capital markets. Building on prior engagement, the partnership is set to deepen cooperation between the International Sustainability Standards Board (ISSB) and the TNFD to promote a more integrated approach to sustainability reporting.

Background and Strategic Context

The formal agreement follows several years of dialogue and shared commitment between the two organisations to deliver decision-useful information to investors. The ISSB’s global baseline – established through IFRS S1 and IFRS S2 – and the TNFD’s voluntary disclosure framework have both emerged as foundational tools to support market transparency on environmental, climate and nature-related risks.

Recognising the urgency of reversing nature loss and the increasing materiality of biodiversity-related issues, the collaboration reflects growing stakeholder demand for greater coherence and interoperability in corporate reporting. The partnership also supports the goals of the Kunming-Montreal Global Biodiversity Framework, reinforcing alignment with broader international sustainability objectives.

TNFD’s Role and Contribution

Launched in June 2021, the TNFD has been instrumental in formulating frameworks that enable organisations to assess and disclose their dependencies and impacts on nature. Their recommendations, released in September 2023, align with global biodiversity goals and provide a structured approach for businesses to integrate nature-related considerations into their strategic planning and reporting processes. More recently, the TNFD has been supporting the ISSB’s Biodiversity, Ecosystems and Ecosystem Services (BEES) research project, initiated in 2024. In February 2025, the TNFD presented an overview of its work to ISSB members, helping to build a shared understanding and laying the groundwork for ongoing collaboration.

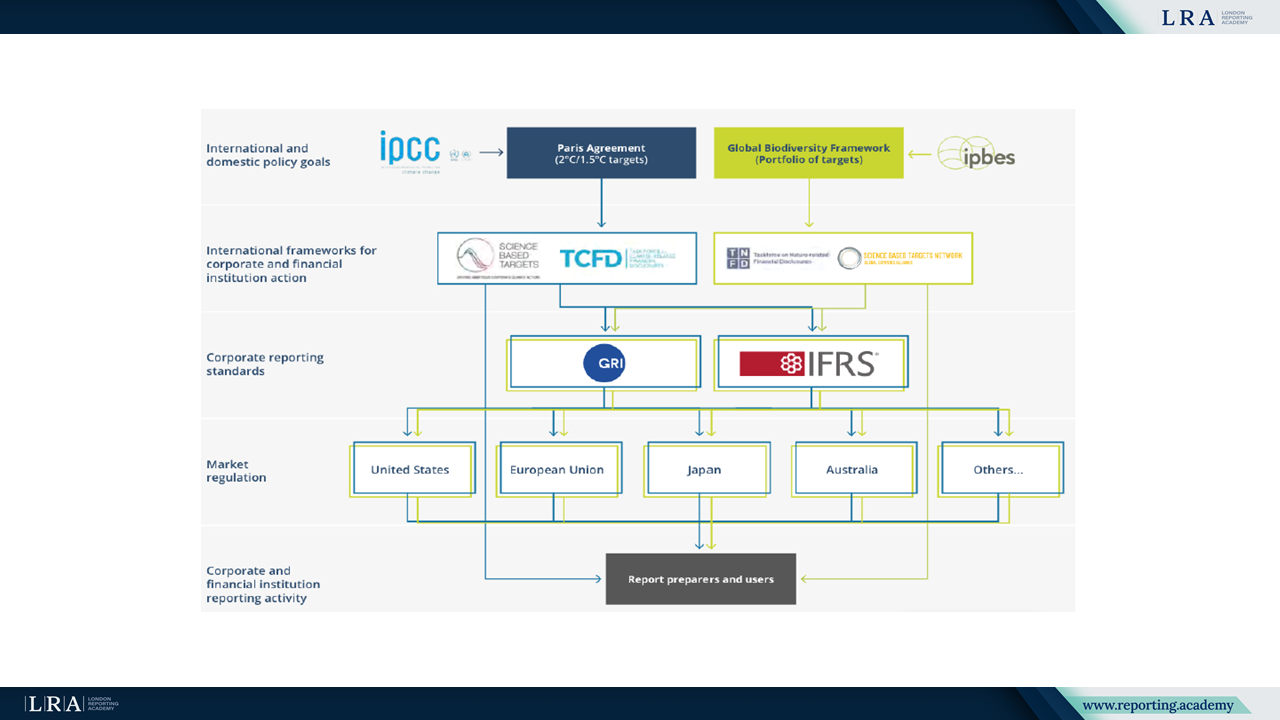

Source: Overview of Global Sustainability Reporting Architecture; AP3C: Nature-related risks and opportunities – The TNFD recommendations

Next Steps and Ongoing Collaboration

The formalised collaboration between the IFRS Foundation and the TNFD reaffirms both organisations’ commitment to enhancing the quality of nature-related financial disclosures. While no immediate changes to standards have been announced, this step marks the beginning of a closer technical dialogue, paving the way for potential future alignment and more coherent sustainability reporting practices worldwide.

Under the MoU, the ISSB and TNFD will share research, knowledge and technical expertise to inform both the ISSB’s BEES initiative and nature-related aspects of its SASB Standards enhancement work. The two organisations will also explore opportunities for joint market engagement and capacity-building efforts, including collaboration with other strategic partners.

In parallel, the TNFD continues its broader global efforts to advance nature-related disclosures – including the development and pilot testing of additional guidance for preparers and the pursuit of data-related initiatives to improve market access to high-quality nature-related information.