IAASB and IESBA Introduce New Standards to Enhance Transparency in Sustainability Reporting

The new ISSA 5000 and IESSA standards establish clear requirements for auditors, ensuring independence, ethics, and consistency in the assurance of sustainability reporting. By setting a high bar for audit quality, these standards help mitigate risks such as greenwashing and enhance trust among investors and the public. Their application strengthens the reliability and comparability of sustainability data, supporting informed decision-making. Moreover, adherence to these standards provides businesses with a strategic advantage, reinforcing long-term sustainability and competitiveness in the global market.

The International Auditing and Assurance Standards Board (IAASB) and the International Ethics Standards Board for Accountants (IESBA) have introduced new standards aimed at enhancing trust in sustainability reporting. The introduction of ISSA 5000 and IESSA will provide unified approaches to sustainability assurance, reduce the risks of greenwashing, and strengthen ethical requirements for professionals in the field.

These new standards will come into effect for reporting periods beginning on December 15, 2026, with the possibility of early adoption. IAASB and IESBA will continue to support the implementation process through webinars, guidance materials, and ongoing monitoring of practical application.

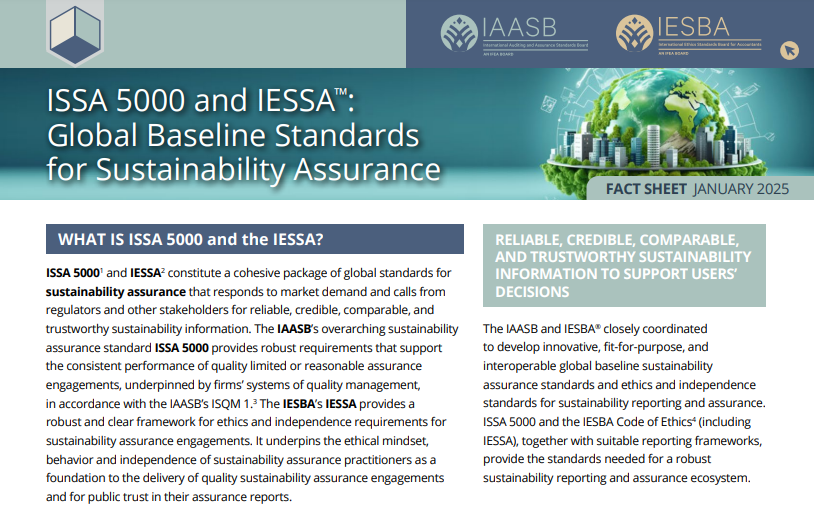

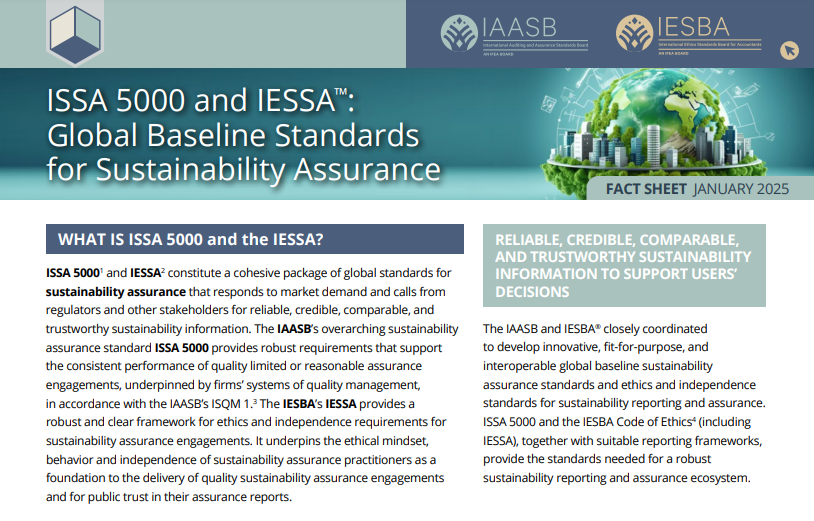

The IAASB and IESBA have also released an informational sheet titled ISSA 5000 and IESSA: Global Baseline Standards for Sustainability Assurance, which outlines the key aspects of the new standards. Their implementation marks a significant step towards standardising sustainability assurance globally.

ISSA 5000: Global Standard for Sustainability Reporting Assurance

ISSA 5000 establishes a unified framework for sustainability reporting assurance, aligning with international standards. As investors and regulators increasingly demand comparable and reliable sustainability data, this standard ensures consistency on a global scale. It covers both limited and reasonable assurance, allowing organisations to choose the approach that best suits their needs. This flexibility helps companies optimise costs while maintaining confidence in their reported data.

Embedded within firms' quality management systems, ISSA 5000 ensures compliance with international assurance standards, strengthening the reliability of assurance processes and helping organisations manage risks related to reporting quality. The standard supports assurance of sustainability reports prepared under frameworks such as GRI, ESRS, IFRS, and other disclosure systems. This adaptability allows businesses to verify data regardless of the specific reporting framework used.

IESSA: Ethical Principles and Independence in Assurance

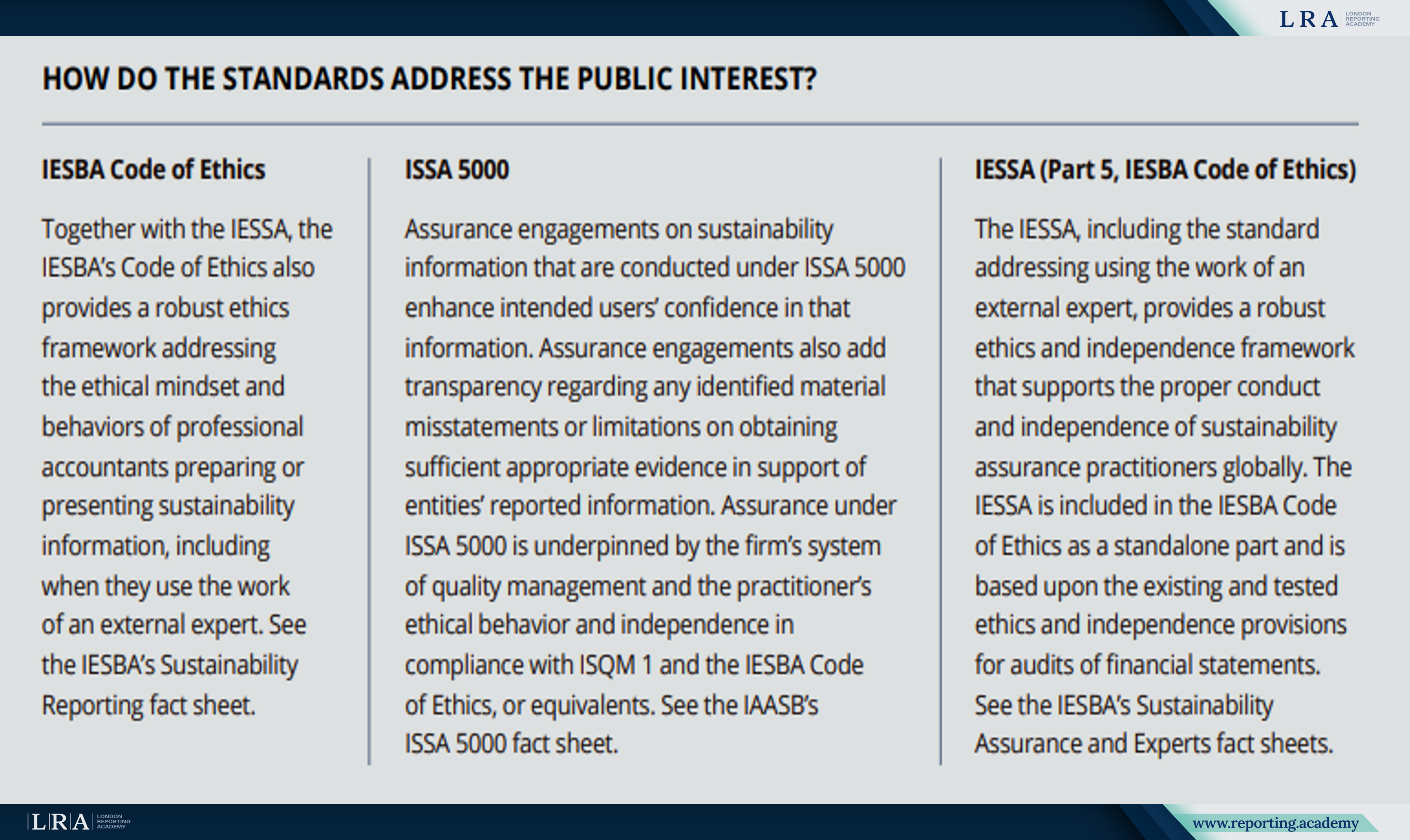

IESSA, developed by the IESBA, introduces stringent requirements for the independence and ethics of professionals involved in sustainability reporting assurance. It enhances transparency and protects the public interest.

IESSA establishes strict requirements to ensure the independence of professionals conducting sustainability reporting assurance. By reducing the risk of conflicts of interest, the standard enhances the objectivity and reliability of data assessments.

The updated IESBA Code of Ethics now applies not only to accountants and auditors but also to all professionals involved in preparing sustainability reports. This expansion strengthens accountability and ensures that sustainability data is presented with integrity.

The standard also regulates the involvement of external experts, setting clear requirements for their independence and qualifications. Companies hiring third-party consultants must now ensure that they adhere to ethical standards, further reinforcing the credibility of sustainability assurance.

Source: Informational sheet titled ISSA 5000 and IESSA: Global Baseline Standards for Sustainability Assurance

Building Trust in Sustainability Audits with ISSA 5000 and IESSA

The implementation of the ISSA 5000 and IESSA standards enables auditors to carry out independent and objective verification of sustainability data disclosed by companies in accordance with various reporting standards. Adhering to these standards helps reduce the risk of non-compliance with regulatory requirements and increases a company's attractiveness to investors, as transparency and reliability of verified data become crucial criteria for financial institutions.

Furthermore, these standards help businesses avoid reputational risks associated with accusations of greenwashing by providing independent confirmation of the credibility of sustainability claims. As reporting assurance requirements tighten, these standards enable companies to build trust with clients, partners, and regulators.

It is also worth noting that the ISSA 5000 and IESSA standards contribute to the global harmonisation of sustainability assurance practices. This is particularly important for multinational companies operating in different countries and needing to comply with varying regulatory requirements. Understanding how auditors will assess their data helps companies prepare information in line with international standards, improving reporting and transparency.