GRI and CDP: Progressing Alignment for Enhanced Climate Disclosure

GRI and CDP have released a disclosure mapping between GRI 102 and GRI 103 and the CDP 2025 climate questionnaire. The resource aims to facilitate more coherent climate reporting across both frameworks.

In October 2025, the Global Reporting Initiative (GRI) and CDP released a new mapping resource linking GRI disclosures to CDP’s 2025 corporate climate questionnaire. This builds on their ongoing collaboration, formalised through a Memorandum of Understanding signed in 2023. The guidance is intended to assist organisations in aligning climate-related disclosures between frameworks and improving the quality and comparability of reported data.

The Context Behind the Alignment

The landscape of sustainability reporting continues to evolve rapidly, with increasing demands for transparency and coherence across frameworks. GRI provides globally recognised standards for reporting environmental, social and governance impacts. CDP collects and publishes environmental data disclosed by companies, which is used by investors and other stakeholders. Recognising the need for compatibility, the mapping links GRI’s revised climate and energy standards with CDP’s 2025 climate questionnaire.

Key Takeaways from the Mapping

The mapping focuses on GRI 102: Climate Change 2025 and GRI 103: Energy 2025. It shows how specific GRI disclosures are associated with corresponding indicators in CDP’s 2025 questionnaire. Each mapped item includes a defined level of correspondence, such as "Full", "Partial", or "No correspondence", which reflects the extent to which the GRI requirement is covered by CDP questions. This helps organisations identify overlaps, streamline data collection, and reduce unnecessary duplication in reporting.

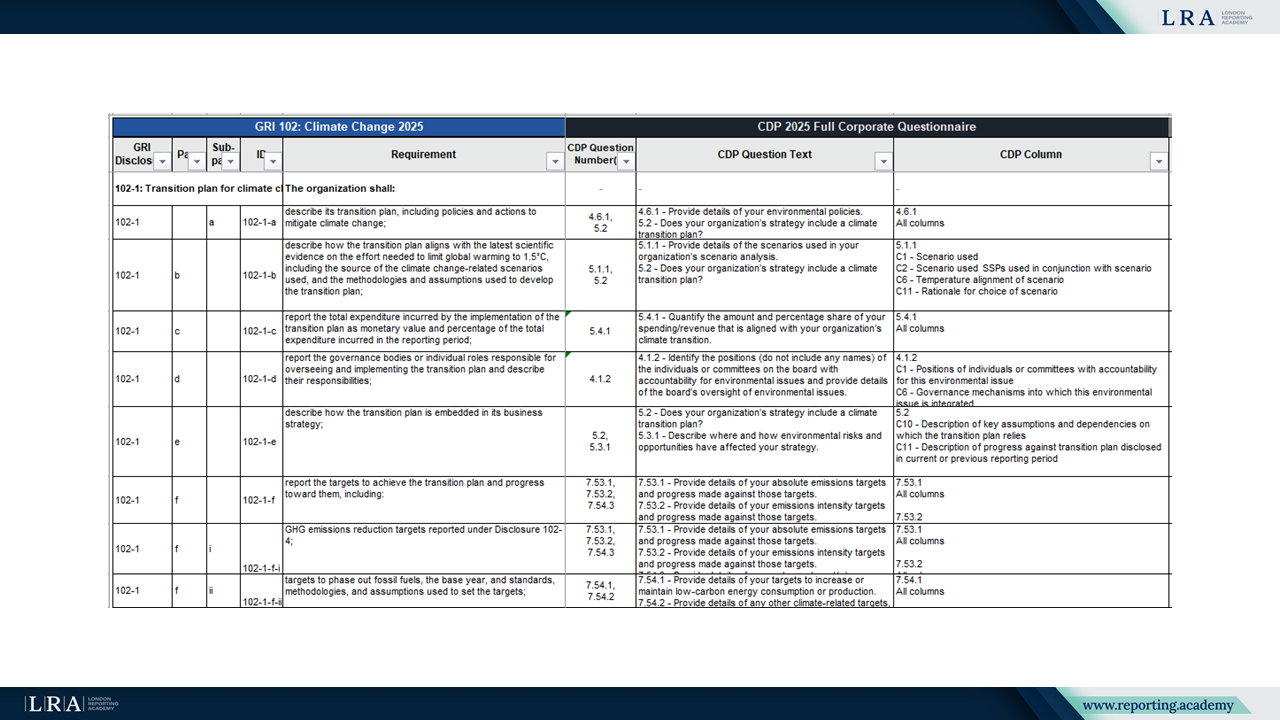

Source: Mapping GRI 102 and GRI 103 standards to CDP 2025 full corporate questionnaire

GRI 102-1 (paragraphs a and b), which requires organisations to describe their transition plans, including policies and actions to mitigate climate change, and to explain how these plans align with the latest scientific evidence to limit global warming to 1.5°C, corresponds to CDP questions such as 4.6.1 and 5.1.1. These CDP questions relate to the structure of environmental transition plans, scenario use, and underlying assumptions. GRI 103-1 focuses on energy-related policies and commitments. When companies provide sufficient detail, these disclosures may support CDP questions including 4.6.1, 4.10, 7.30.14, 7.54.1, 7.54.2 and 7.55.2. In contrast, disclosures under GRI that refer to broader economic or social issues may not always align directly with CDP’s more environmental focus.

Practical Implications for Reporting Entities

For organisations preparing their 2025 sustainability disclosures, this mapping offers a practical reference point. It can help reduce administrative burden by clarifying how shared content supports both frameworks. The resource also enhances consistency in climate-related disclosures, which is valuable for investors, regulators and other users of ESG data.

Users of GRI 102 and 103 are encouraged to consult the mapping to evaluate how their disclosures may align with CDP’s requirements. This is particularly relevant as various jurisdictions strengthen climate-related disclosure mandates. The mapping may also assist organisations in developing more integrated reporting strategies.

A Step Towards Reporting Interoperability

While GRI and CDP serve different reporting objectives, their collaboration reflects a broader shift toward alignment among sustainability frameworks. GRI is rooted in stakeholder inclusivity and multi-dimensional impact reporting. CDP centres on environmental data used in capital markets. Through this mapping, they illustrate how organisations can meet overlapping information needs more effectively.

As the ESG reporting landscape continues to develop, similar alignment initiatives are likely. This 2025 mapping contributes to the effort by offering practical clarity for companies managing climate and energy disclosures. It supports the goal of more coherent, transparent and efficient sustainability reporting.