Global Progress on Corporate Climate Disclosures: Key Insights

A recent report presented by the IFRS Foundation to the Financial Stability Board (FSB) highlights important progress in both mandated and voluntary corporate climate-related disclosures. It focuses on how companies have aligned their reporting with the Task Force on Climate-related Financial Disclosures (TCFD) recommendations.

Following the TCFD's disbandment in 2023, the IFRS Foundation assumed responsibility for monitoring the progress of climate-related disclosures. The report underscores the growing global momentum in climate transparency, particularly in light of the ISSB Standards adoption and their impact on sustainability-related reporting across jurisdictions.

Key Findings

Extensive Adoption of ISSB Standards

- Over 1,000 companies have already referenced the ISSB Standards in their sustainability reports, reflecting growing global recognition of the need for clear climate-related disclosures.

- 30 jurisdictions are making significant progress in adopting the ISSB Standards within their legal and regulatory frameworks, ensuring more consistency in reporting.

TCFD Recommendations Alignment

- A strong 82% of companies have disclosed information aligned with at least one of the 11 TCFD recommendations.

- However, fewer than 3% fully meet all 11 criteria, highlighting gaps in disclosures regarding governance, strategy, risk management, and metrics/targets for climate risks. This incomplete disclosure suggests that investors may be lacking critical information to assess and price climate-related risks effectively.

Source: Preview of the Inaugural Jurisdictional Guide for the adoption or other use of ISSB Standards November 2024

Jurisdictional Developments

An analysis conducted by the IFRS Foundation highlights key features in the regulatory frameworks of these jurisdictions:

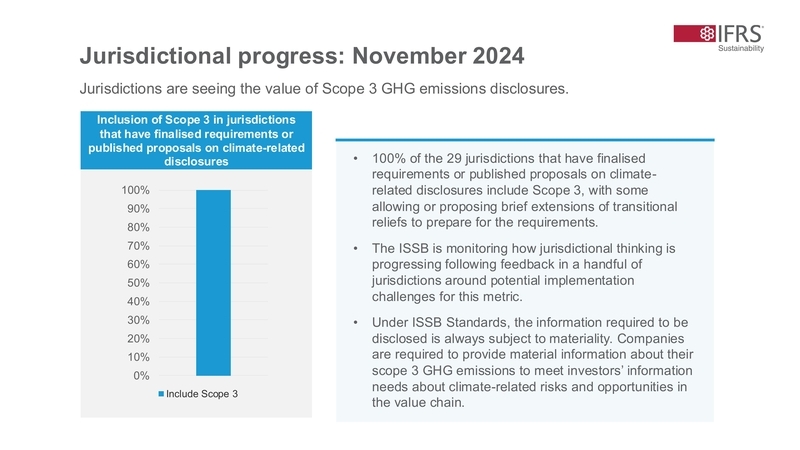

- Scope 3 Emissions Disclosure: Almost all jurisdictions (29) have incorporated requirements for disclosing Scope 3 GHG emissions, with some providing transitional relief to help companies prepare.

Source: Preview of the Inaugural Jurisdictional Guide for the adoption or other use of ISSB Standards November 2024

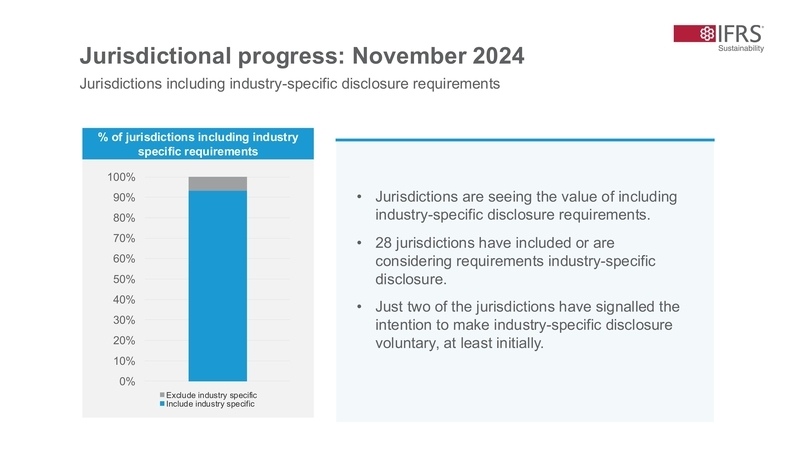

- Industry-Specific Disclosure: 28 jurisdictions have introduced or are considering industry-specific disclosure requirements to ensure that sustainability reports are relevant and comparable across sectors.

Source: Preview of the Inaugural Jurisdictional Guide for the adoption or other use of ISSB Standards November 2024

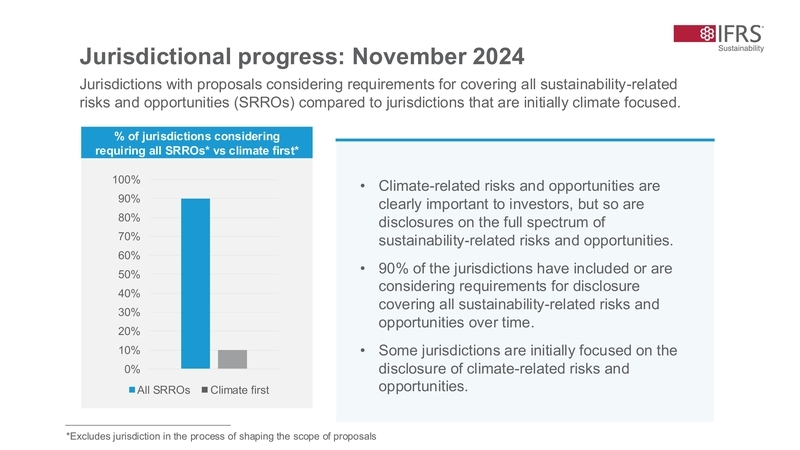

- Comprehensive Sustainability Reporting: 90% of jurisdictions are moving toward including disclosures on the full spectrum of sustainability-related risks and opportunities, with an initial focus on climate-related issues.

Source: Preview of the Inaugural Jurisdictional Guide for the adoption or other use of ISSB Standards November 2024

This backdrop underscores the importance of the regulatory adoption of ISSB Standards, following their endorsement by IOSCO in July 2023. The transition from recommended to mandated disclosures is expected to increase the availability of robust and material sustainability-related information for global capital markets.

Challenges and Stakeholder Concerns

While progress is evident, stakeholders, including investors and multinational companies, express concerns about regulatory fragmentation. Many stakeholders advocate for alignment with the global baseline of ISSB Standards to ensure that companies operating in multiple jurisdictions are not burdened by differing reporting requirements. This approach would streamline the disclosure process, making it more efficient and globally consistent.

Industry-Specific Standards and SASB Integration

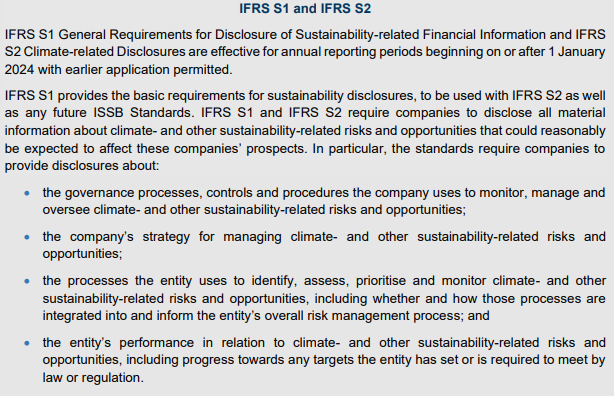

A key takeaway from the report is the growing importance of industry-specific disclosures, which are now being incorporated by many jurisdictions. This is in line with the SASB Standards, which remain the only globally established set of comprehensive industry-specific sustainability disclosure standards. These disclosures are essential for improving the quality and comparability of climate-related reporting, ensuring that companies adhere to the IFRS S1 general requirements for sustainability-related financial disclosures.

The Financial Stability Board has published its 2024 progress report on Achieving Consistent and Comparable Climate-related Disclosures, which summarises the key findings from the IFRS Foundation’s report.

Source: FSB report 2024, Achieving Consistent and Comparable Climate-related Disclosures

Next Steps:

- Alignment and Monitoring:

Ensuring jurisdictional alignment with ISSB Standards is essential for achieving globally comparable disclosures. Progress should be closely monitored. - Enhancing Assurance:

Establishing robust assurance mechanisms to improve trust and reliability in climate-related financial information should remain a priority. - Addressing Fragmentation:

Efforts should continue to harmonise jurisdictional requirements to mitigate the risks of fragmentation, benefiting both preparers and users of sustainability information. - Adapting to Dynamics:

Given the evolving nature of climate-related and sustainability issues, ongoing refinement of standards and practices is vital to meet stakeholders’ information needs effectively.

These steps underscore the importance of global collaboration and regulatory alignment to advance sustainability-related financial reporting.