GHG Protocol Publishes the Land Sector and Removals Standard

Corporate GHG inventories may require more consistent methods to reflect land-based impacts and removals. The Land Sector and Removals (LSR) Standard sets out how these topics are addressed within GHG Protocol corporate inventory reporting, including requirements on boundaries, traceability, and separate disclosure where relevant.

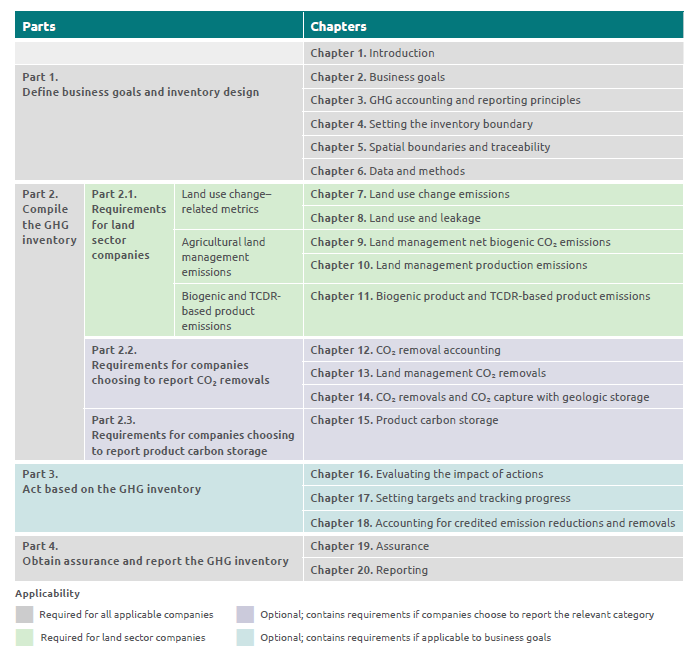

GHG Protocol has released the Land Sector and Removals (LSR) Standard, described as its first global standard for corporate accounting of land sector emissions and removals within greenhouse gas inventories. The announcement frames the document as a response to a long-standing gap in corporate climate accounting for agricultural land use and emerging CO₂ removal technologies, including direct air capture and CO₂ capture with geologic storage.

The Standard is published as Version 1.0 with an approval date of 01 October 2025, a publication date of 30 January 2026, and an effective date of 01 January 2027, and will be reviewed by 2030.

How the Standard Fits Into Corporate GHG Reporting

The LSR Standard is positioned as a supplement to the GHG Protocol Corporate Accounting and Reporting Standard and the Corporate Value Chain (Scope 3) Accounting and Reporting Standard. It is intended for annual, entity-level corporate GHG inventory accounting and is presented as superseding the requirements and guidance contained in the GHG Protocol’s previous Agricultural Guidance.

Source: Structure of the Land Sector and Removals Standard and Guidance, Land Sector and Removals Standard Executive Summary

Version 1.0 applies to agriculture and CO₂ removal technologies and does not apply to forestry. The Independent Standards Board (ISB) did not reach a decision on forest carbon accounting for corporate inventories, and a request for information on forest carbon accounting is planned for 2026 to inform potential future updates.

Applicability and Conformance Expectations

The Standard sets out when it is required for conformance with the GHG Protocol. Companies with significant land sector activities in operations or across the value chain are required to follow this Standard to be in conformance with the GHG Protocol. This requirement also applies to companies that choose to account for and report CO₂ removals or CO₂ capture with geologic storage in their GHG inventory, whether in the reporting year or in previous years.

The Standard also clarifies intended use and boundaries of application. It is designed for land sector and technology-based removal value chains, and it can be used by other entities and stakeholders, but it is not intended for GHG credit certification or verification.

Spatial Boundaries and Traceability in Scope 3

A central element of the accounting framework is the treatment of spatial boundaries and traceability for Scope 3, linked to a company’s ability to identify and track activities and information across its value chain and to determine which lands are included when accounting for emissions, removals, and other land-related metrics.

Within the Standard, Scope 3 spatial boundaries can be set at global, jurisdiction, sourcing region, land management unit (LMU), or harvested area, and the same Scope 3 spatial boundary must be applied across all land emissions, removals, and other land-related metrics for a given volume of a given product or activity.

The Standard introduces an interim traceability requirement for companies that use more granular boundaries. To apply a sourcing region, LMU, or harvested area as the Scope 3 spatial boundary, companies must have physical traceability in the value chain and use specified chain of custody models. The text explicitly states that book-and-claim approaches cannot demonstrate physical traceability.

Accounting Categories, Leakage and Separate Reporting

The Standard highlights accounting categories intended to address land sector impacts that may be underreported in corporate inventories. These include land use change emissions, land carbon leakage, and land use, described as a category to quantify a company’s contribution to global agricultural land use.

The Standard further specifies when leakage accounting is required. Where a company implements high-leakage-risk activities and reports reduced emissions or increased removals while also reducing or diverting food or feed production on agricultural land, land carbon leakage must be accounted for and separately reported under the land carbon leakage accounting category.

For removals, the Standard defines a removal as the net transfer of a greenhouse gas from the atmosphere to storage within a non-atmospheric carbon pool. Reporting CO₂ removals is optional, but any reported removals must be reported separately from emissions. Where removals are reported, additional requirements apply, including monitoring continued storage and accounting for losses, with losses reported as reversals when the carbon pool is no longer within the inventory boundary.

Next Publication

GHG Protocol has indicated that accompanying LSR Guidance is planned for publication later in the year. This publication will provide comprehensive guidance, including examples, equations, and case studies on applying the Standard in practice.