FCA Consults on Aligning Sustainability Disclosures with UK SRS

The Financial Conduct Authority has launched a consultation on proposed amendments to the sustainability disclosure framework applicable to UK listed issuers.

On 30 January 2026, the Financial Conduct Authority (“the FCA”) published Consultation Paper CP26/5 setting out proposals to replace its existing TCFD-aligned climate disclosure rules for listed companies. The consultation closes on 20 March 2026. The FCA has also published a CP26/5 response form alongside the consultation paper to facilitate the submission of stakeholder feedback using the prescribed template. The regulator states that the objective is to align the UK listing framework with current international standards and to support the development of UK Sustainability Reporting Standards (UK SRS).

The FCA notes that its current climate disclosure requirements were built around the recommendations of the Task Force on Climate-related Financial Disclosures (TCFD), which was established in 2015 and disbanded in 2023. Since then the International Sustainability Standards Board (ISSB) has issued IFRS S1 General Requirements for Disclosure of Sustainability-related Financial Information and IFRS S2 Climate-related Disclosures. The UK Government is developing UK SRS to endorse these ISSB standards for use in the UK, and CP26/5 explains how the FCA proposes to incorporate that framework into the Listing Rules.

Scope and Structure of the Proposals

The consultation covers a range of listing categories, including commercial companies under UKLR 6, secondary listings under UKLR 14, depositary receipts under UKLR 15, non-equity shares and non-voting equity shares under UKLR 16, and the transition category under UKLR 22. The FCA therefore proposes to introduce new rules requiring in-scope listed companies to report in line with UK SRS.

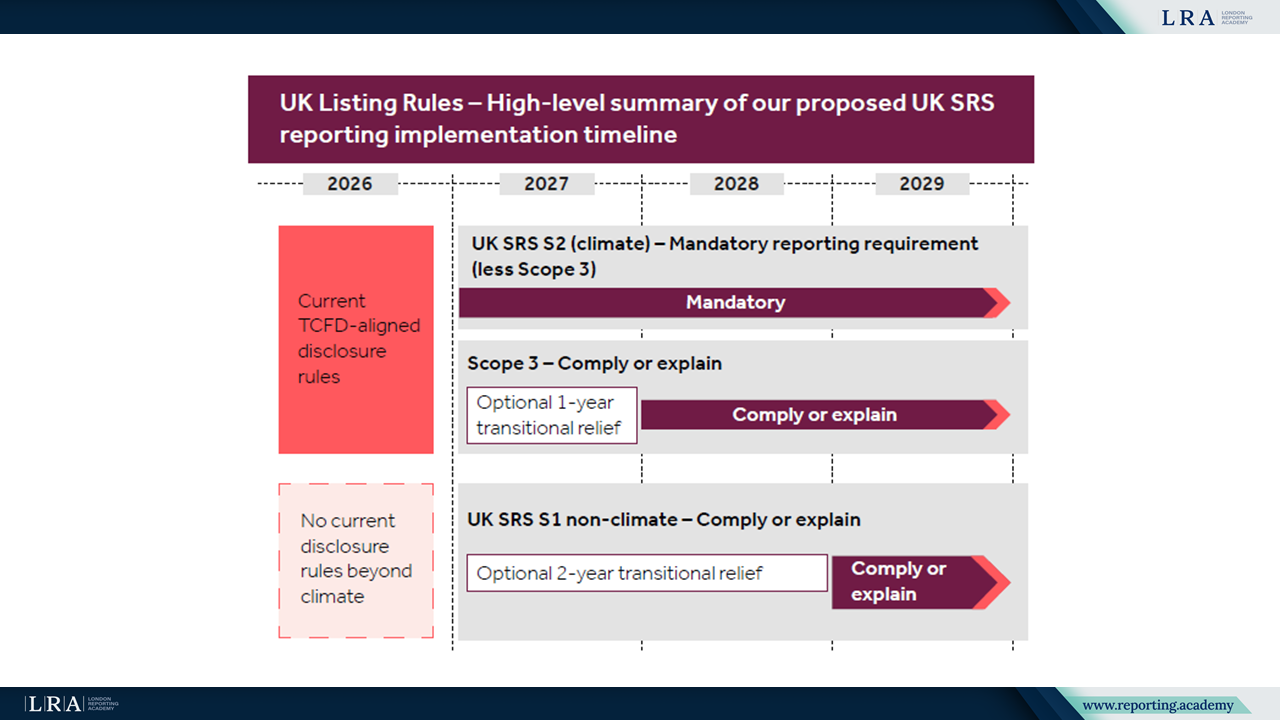

Source: High-level summary of the proposed UK SRS implementation timeline, Consultation Paper

For climate-related disclosures the FCA proposes mandatory reporting against UK SRS S2. However, in recognition of practical challenges, Scope 3 greenhouse gas emissions would be subject to a comply or explain approach. Where an issuer does not disclose Scope 3 information it would be required to explain the reasons and describe the steps it is taking to obtain the necessary data.

For non-climate sustainability-related information under UK SRS S1, the FCA proposes a comply or explain basis. The regulator acknowledges that this would represent a broader reporting requirement for some issuers and therefore considers proportionality in its approach.

Transition Plans and Assurance

CP26/5 clarifies that mandating climate-related transition plans is a matter for Government. The FCA nevertheless proposes that issuers should disclose whether they have published a climate-related transition plan, where it can be found, or explain why such a plan has not been published.

The consultation also addresses third-party assurance. Issuers would be required to state whether their sustainability disclosures have been subject to assurance and, where applicable, identify the assurance provider, the scope and level of assurance, the standards applied and where the assurance report is available.

Implementation Timeline

Subject to feedback and the finalisation of UK SRS, the FCA aims to publish a Policy Statement (PS) in autumn 2026. The proposed rules would come into force from 1 January 2027 and apply to accounting periods beginning on or after that date. The consultation paper also refers to transitional reliefs within UK SRS, including up to two years for certain non-climate disclosures under UK SRS S1 and one year for Scope 3 disclosures under UK SRS S2.

CP26/5 outlines a framework to transition the UK listing regime from a TCFD-based model to one aligned with ISSB-derived UK Sustainability Reporting Standards, incorporating proportional mechanisms such as comply or explain and transitional reliefs.