ESMA Publishes Paper on New Standards for EU Markets

The European Securities and Markets Authority (ESMA) has released a Consultation Paper addressing critical updates to the European Single Electronic Format (ESEF) under the Transparency Directive and analysing the implications of transitioning to a T+1 securities settlement cycle. This initiative aims to advance financial market efficiency while balancing stakeholder costs and operational risks.

Key Highlights

The Consultation Paper introduces substantial updates to the ESEF framework and explores the transition to a shorter settlement cycle. These proposals are designed to modernise financial reporting and improve the resilience of EU markets.

Policy Objectives for ESEF

- Sustainability Reporting Enhancements: ESMA proposes aligning ESEF requirements with sustainability taxonomies developed by EFRAG to support the digitalisation of sustainability reporting;

- IFRS Reporting Revisions: Updates to tagging Notes in IFRS consolidated financial statements are included, reflecting practical insights gained from the current ESEF implementation.

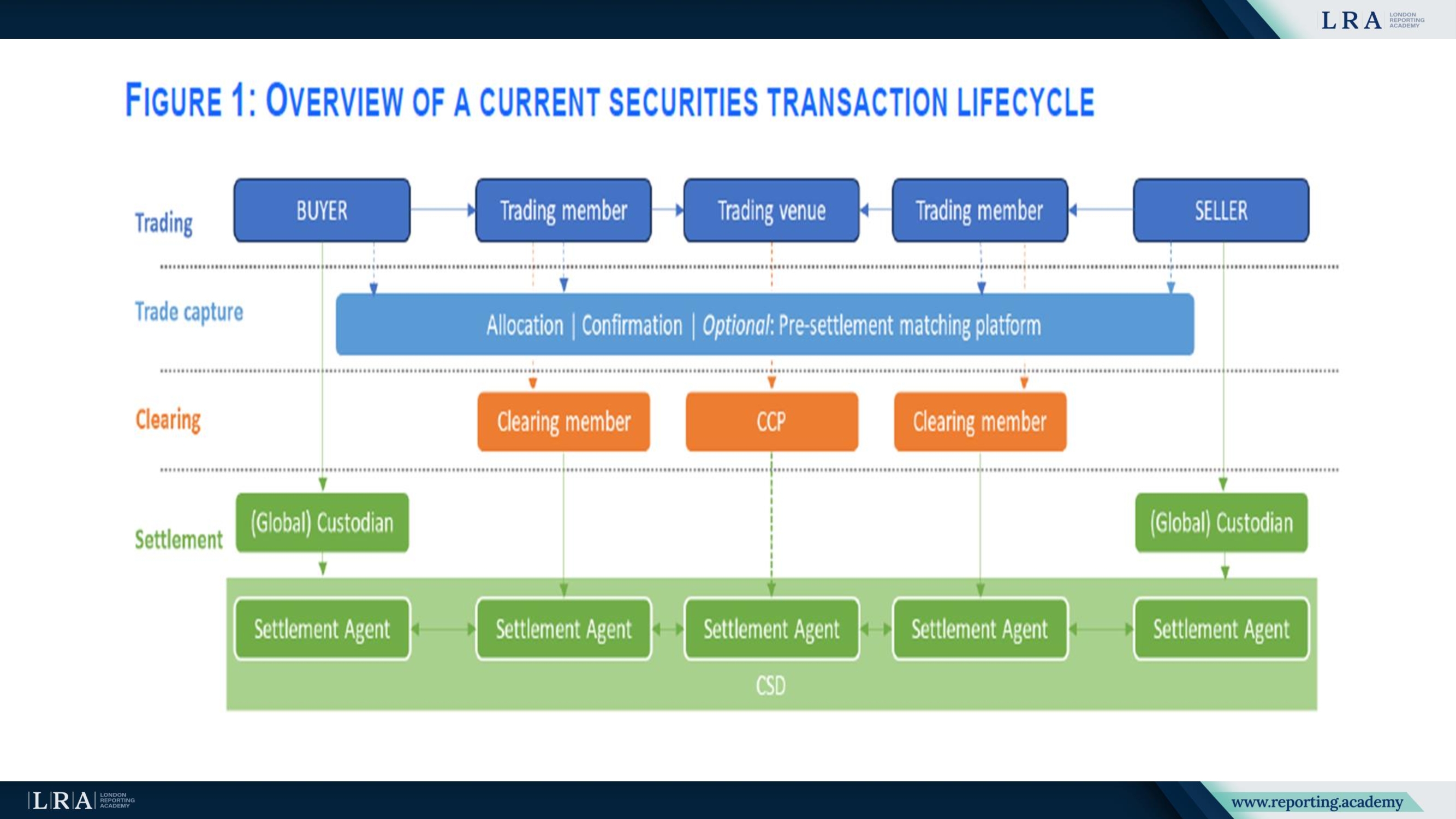

Transition to T+1 Settlement Cycle

ESMA examines the complexities and adjustments required to implement a T+1 settlement cycle, involving all trading and post-trading participants within and beyond the EU.

Source: ESMA’s Report 2024, ESMA assessment of the shortening of the settlement cycle in the European Union

Detailed Impact of the T+1 Transition

The transition to a T+1 settlement cycle marks a significant overhaul of existing processes in EU financial markets. This change will require all market participants, including investors, intermediaries, and infrastructures, to adapt their operations to meet the shortened timeline. ESMA's analysis highlights the adjustments needed across various aspects of securities and cash management, alongside the broader operational impacts.

Securities Position Management

- Securities Financing Transactions: Shortened settlement timelines demand timely securities availability, increasing collateral buffers and costs in securities lending markets. Market makers and lenders must adapt to ensure liquidity while avoiding market inefficiencies;

- Automation Imperative: The shift necessitates greater automation in securities lending and borrowing processes. Without this, liquidity and market efficiency may deteriorate.

Cash Position Management

- FX Transaction Challenges: The T+1 cycle requires FX transactions to occur earlier, potentially increasing costs. Time zone differences exacerbate these challenges for cross-border trades;

- Lessons from the U.S.: ESMA highlights the U.S. experience with T+1, where adjusted practices mitigated adverse impacts, as a reference point for the EU's transition.

Costs and Benefits

- Reduced Margin Requirements: The shift to T+1 is projected to lower open positions and CCP margin requirements by 42%, freeing liquidity worth approximately EUR 2.4 billion across equity and bond markets;

- Market Integration: Greater standardisation and automation across EU markets are expected to drive efficiency and integration.

Source: ESMA’s Report 2024, ESMA assessment of the shortening of the settlement cycle in the European Union

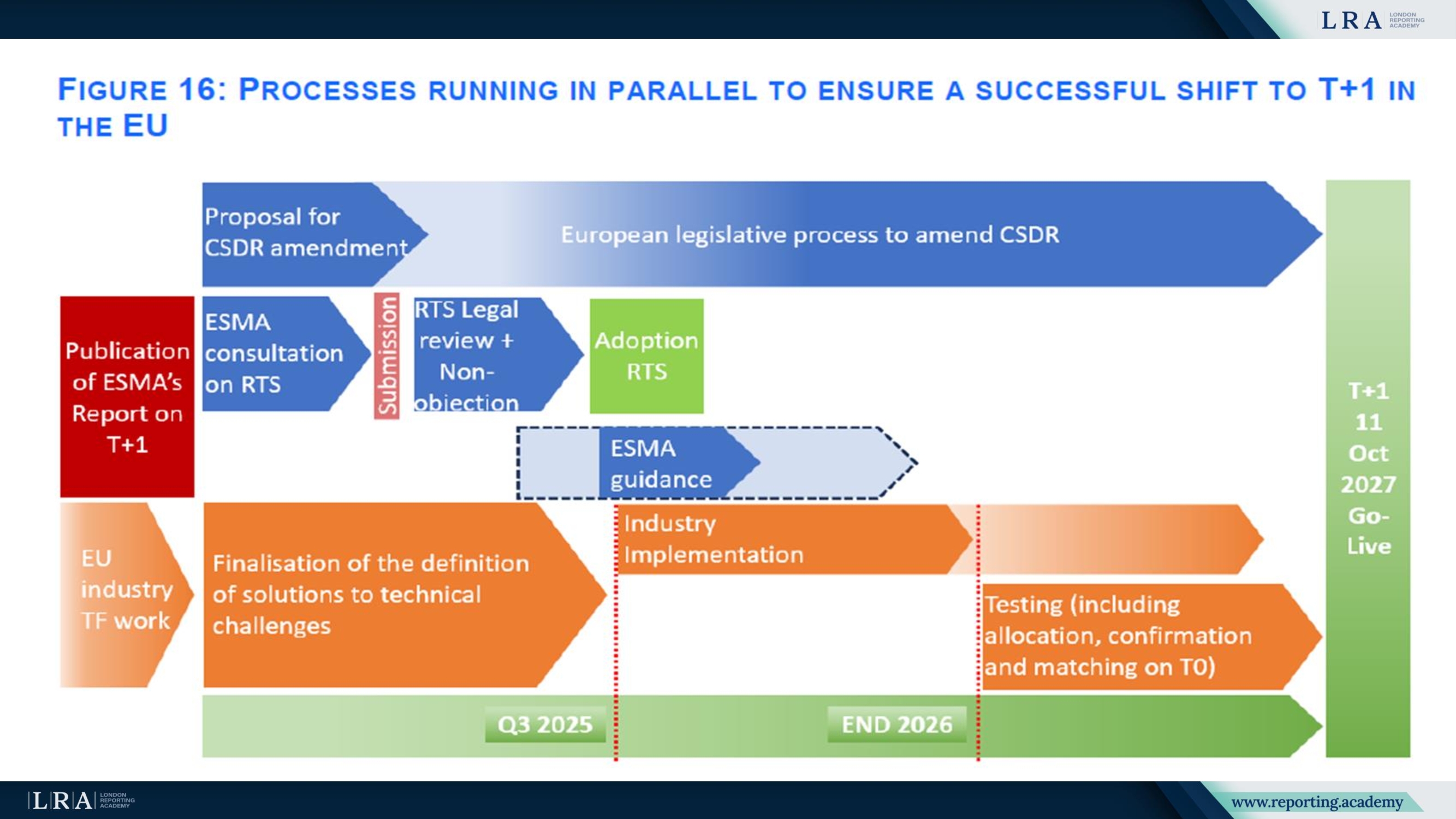

Next Steps

- Feedback Period: Stakeholder input is invited to refine the proposals, with feedback reviewed in Q2 2025.

- Draft RTS Submission: Final RTS will be submitted to the European Commission in Q3 2025 for endorsement.

Sustainability reports aligned with ESRS and Article 8 of the EU Taxonomy Regulation must be published in XHTML format and tagged using iXBRL. These updates aim to enhance digital accessibility and standardisation in sustainability disclosures.

ESMA encourages evidence-based feedback to shape policies that balance market efficiency, risk mitigation, and operational costs. The outcomes of this consultation will influence the EU’s financial reporting and settlement frameworks in the coming years.

Conclusions

- The proposed reforms will drive significant improvements in market efficiency through enhanced reporting standards, reduced settlement cycles, and better liquidity management.

- However, these changes will require substantial investments in automation and adjustments to operational processes by market participants to fully realise the potential benefits.

- The EU must carefully consider stakeholder feedback and leverage global best practices, such as those seen in the U.S., to ensure a smooth and successful transition.