EFRAG Releases Feedback on the IASB Exposure Draft “Climate-related and Other Uncertainties in the Financial Statements - Proposed Illustrative Examples”

The European Financial Reporting Advisory Group (EFRAG) has released a feedback statement on the IASB's Exposure Draft titled "Climate-related and Other Uncertainties in the Financial Statements - Proposed Illustrative Examples." This statement highlights stakeholder perspectives on the proposed guidance and its implications for financial reporting.

The European Financial Reporting Advisory Group (EFRAG) has recently issued a feedback statement on the IASB's Exposure Draft titled “Climate-related and Other Uncertainties in the Financial Statements - Proposed Illustrative Examples”. This document marks an important step towards enhancing the reporting of climate-related and other uncertainties within financial statements. The feedback statement, published in March 2025, summarises key stakeholder responses collected during the consultation period and outlines critical observations influencing the project's next stages.

The Purpose of the Project

The project "Climate-related and Other Uncertainties in the Financial Statements" was initiated by the IASB following stakeholder concerns raised during the IASB’s 2021 Third Agenda Consultation. Stakeholders highlighted issues regarding insufficient reporting of climate-related risks within financial statements. Responding to this feedback, the IASB added this topic to its work plan in April 2022, activating it officially in March 2023. The primary objective of the project is to explore how financial statements can more effectively communicate the effects of climate-related and other uncertainties, addressing current gaps in reporting practices.

The Exposure Draft and Consultation

In July 2024, the IASB published an exposure draft containing eight illustrative examples intended to guide entities in reporting climate-related and other uncertainties according to IFRS Accounting Standards. These illustrative examples primarily address climate-related risks but apply equally to other uncertainties. The exposure draft was available for public comment until November 2024. During this period, EFRAG organised several outreach events, gathering diverse stakeholder perspectives. The IASB expects that the illustrative examples will help improve the reporting of the effects of climate-related and other uncertainties in financial statements, including by strengthening connections between an entity's general purpose financial reports.

Summary of the Feedback Statement

EFRAG's March 2025 feedback statement summarises major stakeholder responses to the Exposure Draft. Stakeholders broadly welcomed the illustrative examples, recognising their value as essential educational materials that can improve connectivity and the quality of disclosed information both within and outside financial statements.

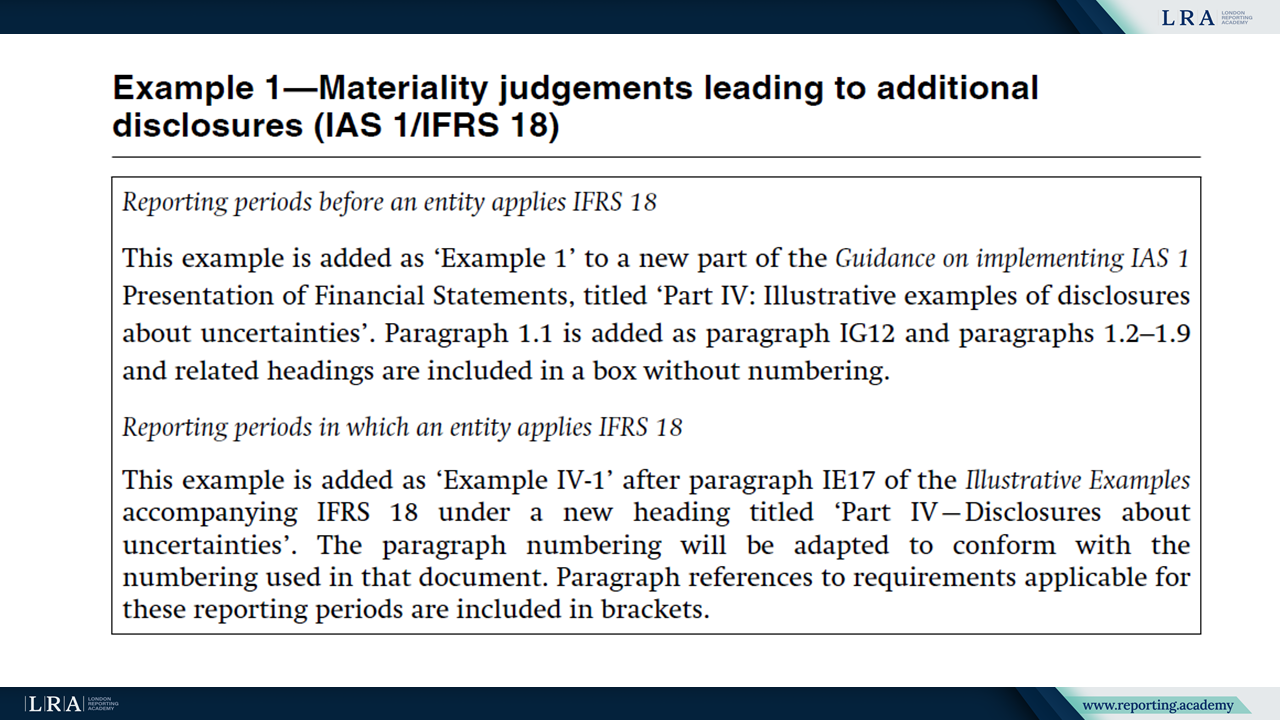

Nevertheless, respondents identified areas needing refinement. In particular, many emphasised the need to improve paragraph BC326 of the Exposure Draft to provide clearer guidance on the interaction between illustrative Examples 1 and 2 and ISSB Standards.

Source: Climate-related and Other Uncertainties in the Financial Statements - Proposed Illustrative Examples; Examples 1 and 2.

Stakeholders provided targeted feedback on illustrative examples. Notably, there was uncertainty about interpreting paragraph 125 of IAS 1, especially illustrated in Example 4. Stakeholders recommended resolving this through targeted standard-setting rather than solely through illustrative examples.

Source: Climate-related and Other Uncertainties in the Financial Statements - Proposed Illustrative Examples; Example 4.

Furthermore, although respondents generally supported including illustrative examples as accompanying IFRS Accounting Standards to facilitate timely issuance, some expressed concerns that the lack of formal EU endorsement might limit their practical use. Respondents thus proposed embedding the examples directly into IFRS Accounting Standards to ensure EU endorsement.

Lastly, stakeholders strongly emphasised the importance of enhancing connectivity between financial and sustainability reporting. They encouraged the IASB and ISSB to collaboratively create illustrative examples specifically addressing this connectivity to prevent redundant reporting and improve overall coherence.

EFRAG integrated these stakeholder insights into its final comment letter, urging the IASB to expedite the finalisation of illustrative examples while addressing the highlighted feedback areas.

EFRAG's Recommendations for Next Steps

EFRAG has strongly endorsed the IASB's illustrative examples and recommended the IASB prioritise their publication promptly. According to EFRAG’s final comment letter, further development of additional examples or initiation of new standard-setting activities should occur only after finalising the existing illustrative examples, except for targeted standard-setting activities specifically related to clarifications, such as the interpretation of paragraph 125 of IAS 1 dealing with disclosure of estimation uncertainty.

EFRAG also suggested targeted standard-setting activities to clarify specific IFRS Accounting Standards requirements, including IAS 36 (Impairment of Assets), IAS 38 (Intangible Assets), IFRS 7 (Financial Instruments: Disclosures), IFRS 9 (Financial Instruments), and mechanisms related to pollutant pricing, acknowledging the broader impact these uncertainties could have across various accounting standards.

Conclusion

The Exposure Draft “Climate-related and Other Uncertainties in the Financial Statements - Proposed Illustrative Examples” represents a significant advancement in addressing stakeholder concerns regarding the reporting of climate-related and other uncertainties in financial statements. Stakeholders have generally welcomed these examples as valuable resources that will enhance the transparency and connectivity of disclosed information. Although there were suggestions for refinement, overall support for the initiative remains strong. Going forward, the IASB is encouraged to finalise the illustrative examples promptly, continue targeted standard-setting activities, and strengthen collaboration with the ISSB to further improve the connectivity between financial statements and sustainability-related disclosures.