EFRAG Presents Voluntary Sustainability Reporting Standard for Small and Medium Enterprises (VSME)

On 17 December 2024, EFRAG introduced the Voluntary Sustainability Reporting Standard (VSME) for non-listed SMEs, confirmed by the European Commission. The standard aims to simplify sustainability reporting and support access to sustainable finance. It aligns with the EU ESG Ratings Regulation, effective from July 2026, which enhances transparency for ESG rating providers.

On 17 December 2024, the European Financial Reporting Advisory Group (EFRAG) presented its technical advice on the Voluntary Sustainability Reporting Standard for non-listed small and medium-sized enterprises (SMEs) – the VSME. This long-awaited standard was developed at the request of the European Commission and confirmed on 12 December 2024. The introduction of the VSME is of great significance for SMEs seeking to access sustainable finance, as it provides a unified framework for sustainability disclosure and simplifies the reporting process.

In addition, EFRAG released its Cover Letter outlining the cost-benefit analysis for the Voluntary Standard for non-listed SMEs (VSME), which highlights the standard’s potential to reduce the reporting burden on SMEs while providing valuable insights into its economic viability and long-term benefits. EFRAG also published the VSME Basis for Conclusions, which provides a comprehensive explanation of the rationale behind the development of the standard and clarifies key decisions made during its creation.

Description of the VSME Standard

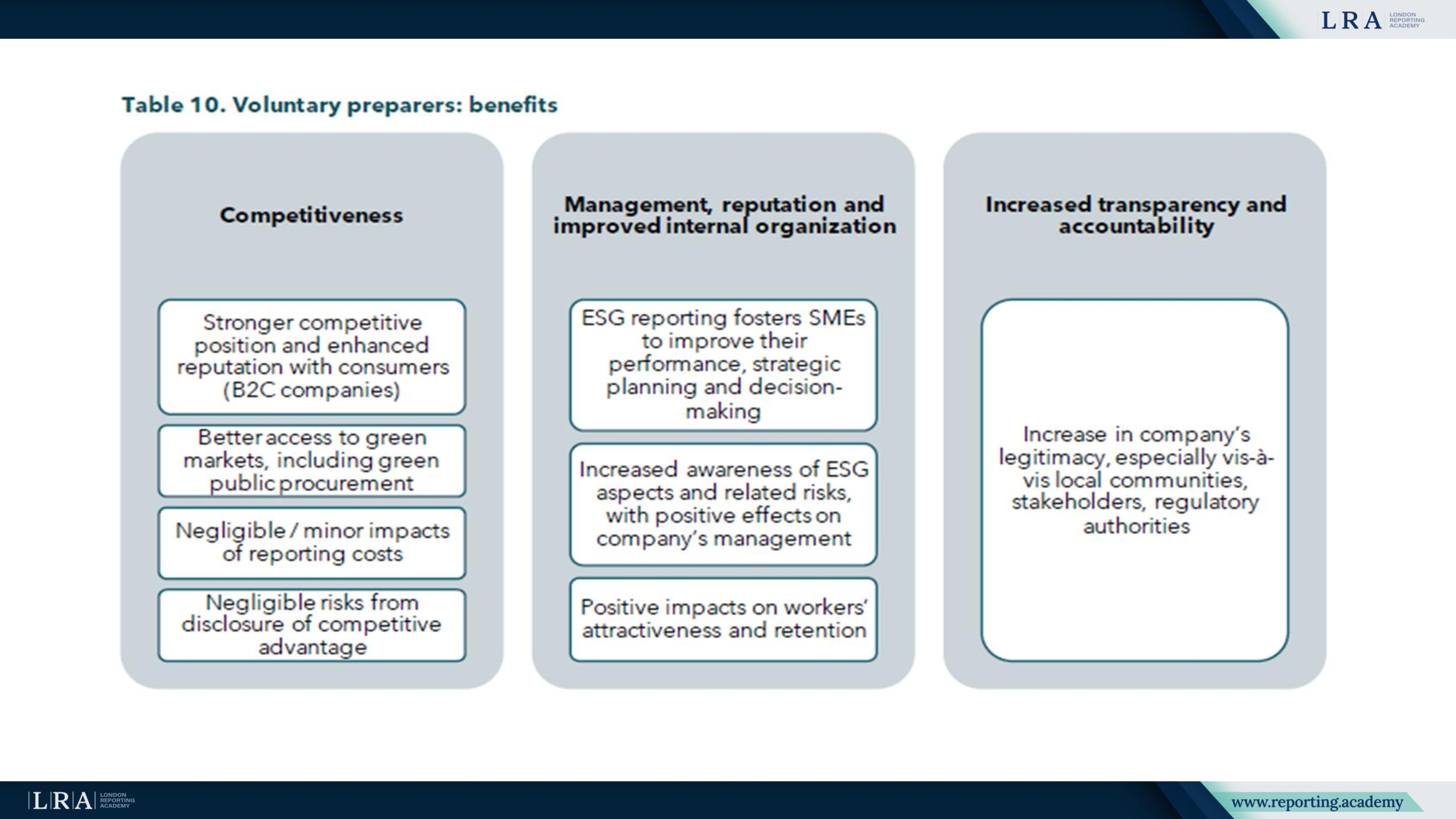

The VSME standard was created to help small and medium-sized enterprises meet the disclosure requirements set by banks, investors, and large corporations, without imposing excessive reporting obligations as seen with larger companies subject to mandatory Corporate Sustainability Reporting Directive (CSRD) requirements.

The standard consists of two modules:

- Basic Module: This is the foundational version of the standard, designed for SMEs that are just starting to disclose sustainability information. The module focuses on providing the minimum information required to meet the basic needs of stakeholders.

- Comprehensive Module: Aimed at more mature and developed SMEs, this module enables businesses to provide more detailed and structured information. It allows companies to offer deeper insights, which meet the expectations of large investors and corporations seeking more thorough analysis of sustainability and climate impact.

These two modules provide SMEs with flexibility in their reporting approach, allowing them to choose the level of disclosure most appropriate to their maturity and the requirements of their stakeholders.

Objectives of the VSME Standard

The primary goal of the VSME standard is to facilitate SMEs' access to sustainable finance through enhanced reporting. It reduces the bureaucratic burden associated with navigating numerous, sometimes contradictory, disclosure requests and streamlines the process of engaging with investors and other stakeholders. The standard standardises reporting processes and provides uniform criteria for all companies falling under its scope.

Moreover, the implementation of this standard forms part of the European Commission's broader strategy to promote a transition to a more sustainable economy. It also ties into the 2023 SME Relief Package, which includes initiatives designed to support green financing and accelerate the transition to sustainability across the European Union.

Discussion and Conclusions on Risks and Strategies

The new standard provides businesses with the opportunity to disclose their sustainability, including recommendations on practices for transitioning to a sustainable economy, reducing greenhouse gas emissions, and managing climate-related risks.

Key disclosure aspects under the new standard:

- Greenhouse Gas (GHG) Emissions: The standard requires the disclosure of data on Scope 1 emissions, Scope 2 emissions, and Scope 3 emissions where applicable for SMEs.

- Emission Reduction Targets: SMEs that have set emission reduction targets should disclose information on target values and key actions to achieve these goals.

- Climate-Related Risks: The standard outlines requirements for information on climate risks, including descriptions of climate threats and transitional phenomena that may affect the business.

This comprehensive approach enables companies not only to comply with regulatory requirements but also to enhance transparency for stakeholders. Importantly, the standard supports the integration of sustainability strategy into corporate processes and assists companies in more effectively managing climate risks.

Key Details for SMEs

For companies choosing to apply the comprehensive module, more detailed disclosures are required:

- C1 – Strategy: Business Model and Sustainability: Participating businesses must describe the key elements of their business model and strategy, including details of products and services, as well as approaches to sustainability.

- C2 – Transition Practices: SMEs can report on their initiatives aimed at transitioning to a more sustainable economy, including external policies and actions.

- C3 – Emission Reduction Targets and Transition to a Low-Carbon Economy: This section provides details on standard methods for reducing greenhouse gas emissions, which should be presented in absolute terms for Scope 1 and Scope 2. If relevant data is not available, the business can indicate the absence of such a metric.

Providing clear and accessible tools for SMEs is a key objective of the new standard. Tools such as templates and calculators will be developed to support these changes, helping businesses submit the required data with minimal costs. Importantly, EFRAG is focused not on directly creating these tools but on facilitating their development by other market participants.

Conclusion

The VSME standard marks a significant step towards creating a more structured and transparent system for sustainable finance and reporting. For SMEs, it opens up new opportunities to engage in the sustainable transition and gain better access to green finance. The standardisation and improvement of sustainability disclosure practices will help mitigate risks, boost confidence in ESG ratings, and contribute to fairer and more sustainable economic growth across the European Union.

EFRAG will continue to develop tools and methods of support for SMEs to help them integrate these new standards into their operational processes and be prepared for the changes that will occur in the sustainable finance sector in the coming years.