EFRAG advances the discussion on connectivity in corporate reporting

Connectivity between financial and sustainability reporting has become an increasingly prominent topic as users seek clearer links between narrative disclosures and financial outcomes. Against this background, EFRAG’s recent work provides a structured lens for understanding how such connections are currently framed, observed and constrained within corporate reporting.

In December 2025 EFRAG published a Discussion Paper entitled Connectivity of Financial and Sustainability Reporting together with a Supplemental Document containing illustrative examples. The publication forms part of EFRAG’s proactive research agenda and is positioned as non-authoritative. It is intended to stimulate public debate on how financial and sustainability information are presented within the annual report and to contribute to the evolution of corporate reporting practices rather than to provide implementation or application guidance for ESRS.

The initiative responds to increasing expectations from users of corporate reports that financial statements and sustainability reporting should together present a coherent and holistic view of an undertaking’s strategy, performance, prospects and risk profile. In this context, EFRAG highlights that the concept of connectivity has gained particular relevance alongside the introduction of sustainability reporting requirements in the European Union, including the first reporting cycles under the European Sustainability Reporting Standards (ESRS).

Connectivity as a reporting concept and its scope

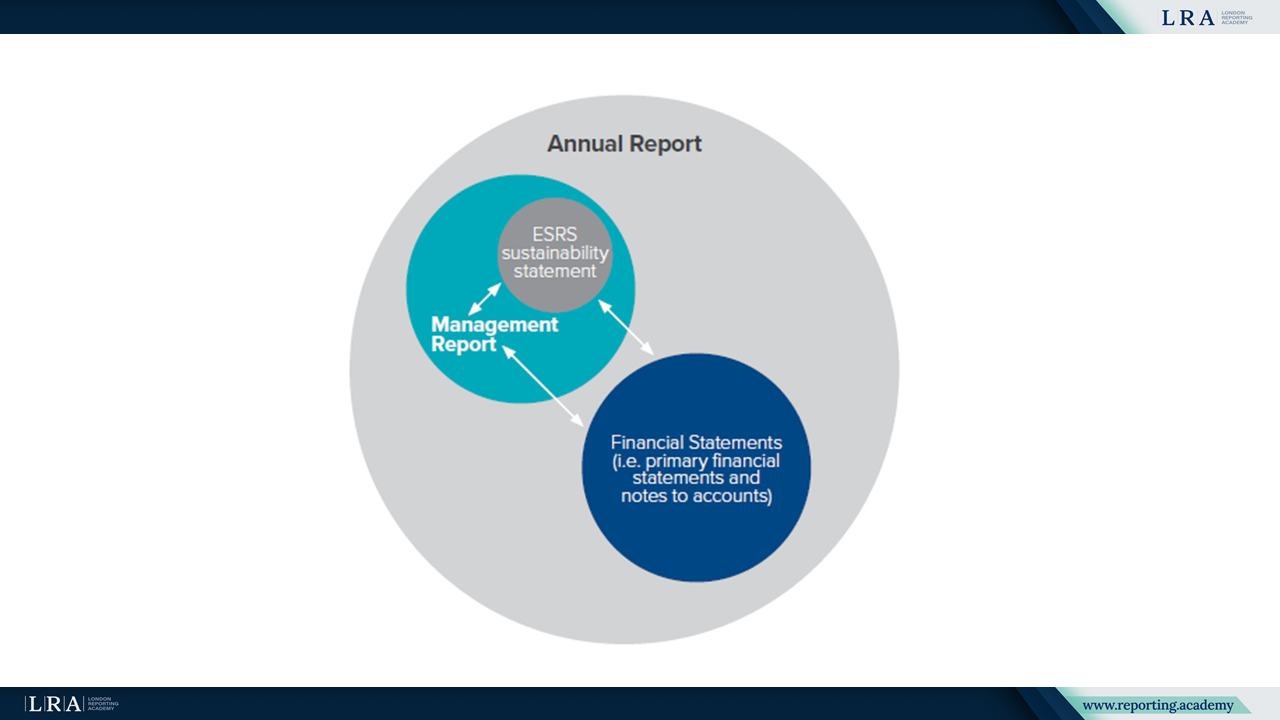

In the Discussion Paper connectivity of reported information is described as an attribute of high-quality information that supports the provision of a holistic and coherent set of disclosures within and across different sections of the annual report. EFRAG underlines that financial statements and sustainability statements serve different objectives and are subject to distinct recognition and disclosure requirements. Financial statements are constrained by recognition criteria and measurement thresholds, while sustainability statements include impacts, risks, opportunities and forward-looking information that are not recognised under IFRS Accounting Standards.

Source: Scope of connectivity under the EU reporting framework, EFRAG Discussion Paper

A central theme of the Discussion Paper is the clarification of the borders of different annual report sections. EFRAG observes that a lack of clarity regarding what information can be disclosed in the financial statements and what should instead be reported in the sustainability statement or other sections of the management report contributes to perceived inconsistencies in corporate reporting. By analysing connectivity together with the borders of report sections, the Discussion Paper seeks to explain why some information is connected across reports while other information cannot be connected despite user expectations.

Types and mechanisms of connectivity

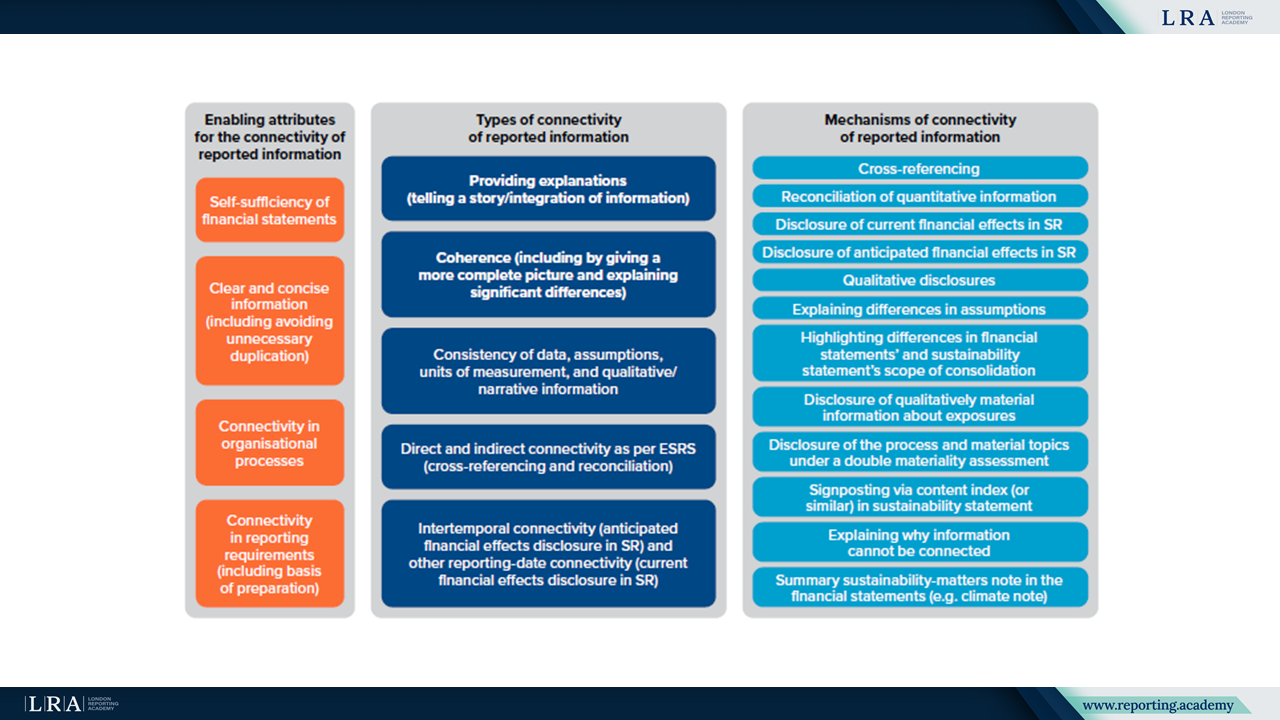

The Discussion Paper distinguishes between different types of connectivity and the mechanisms through which they are achieved. Connectivity is described through concepts such as coherence where information across reports provides a more complete picture, consistency of related data, narratives and assumptions, and the connection of quantitative information through cross-referencing or reconciliation. In addition, the Paper discusses intertemporal connectivity, which links information disclosed in the current reporting period to potential effects in future-period financial statements.

Source: Enabling attributes, types and mechanisms of connectivity of reported information, EFRAG Discussion Paper

These types and mechanisms are analysed with reference to existing requirements and guidance in ESRS, ISSB Standards and the IFRS 1 Practice Statement-Management Commentary (IFRS MCPS). EFRAG notes that while connectivity and related concepts are explicitly addressed in sustainability reporting standards and management commentary guidance, IFRS Accounting Standards do not currently define connectivity as an explicit reporting principle.

Insights from current reporting practices and user perspectives

EFRAG’s review of more than 70 annual reports indicates that companies are still at an early stage in applying connectivity in practice. The Discussion Paper identifies areas of progress including the increased use of cross-referencing between sustainability statements and financial statements, and the reconciliation of sustainability-related metrics with financial information, for example in the context of EU Taxonomy disclosures and climate-related reporting.

At the same time EFRAG highlights recurring challenges. These include inconsistent terminology across different sections of the annual report, limited linkage between sustainability-related impacts, risks and opportunities and their effects on financial position, performance and cash flows and differences in levels of aggregation between sustainability and financial disclosures. The Paper also emphasises that some perceived inconsistencies reflect differences in the borders of report sections rather than omissions or errors in reporting.

From a user perspective the Discussion Paper reports that connectivity is regarded as a characteristic of high-quality reporting. Users and other stakeholders emphasise that improved connectivity can reduce information asymmetry and support a clearer understanding of how sustainability-related impacts, risks and opportunities are linked to financial effects. In this sense connectivity is viewed as a factor that enhances the credibility and usefulness of corporate reporting rather than as a purely presentational exercise.

Illustrating connectivity across reporting frameworks

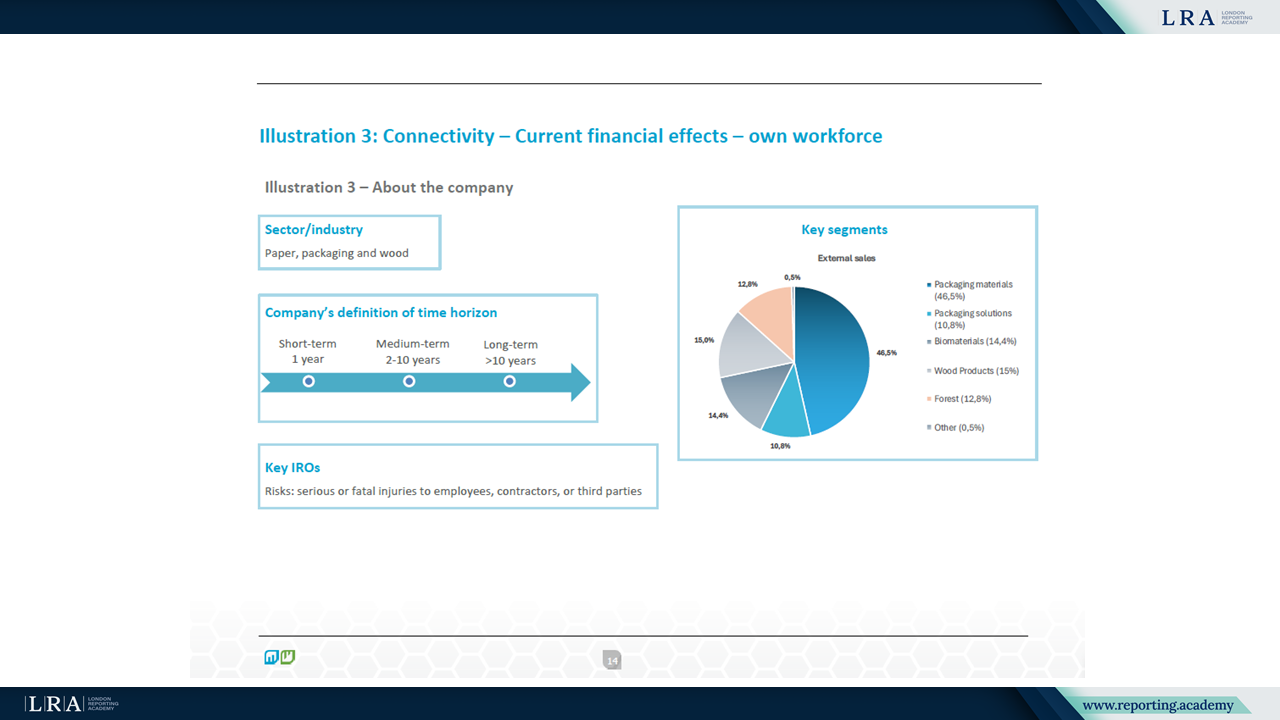

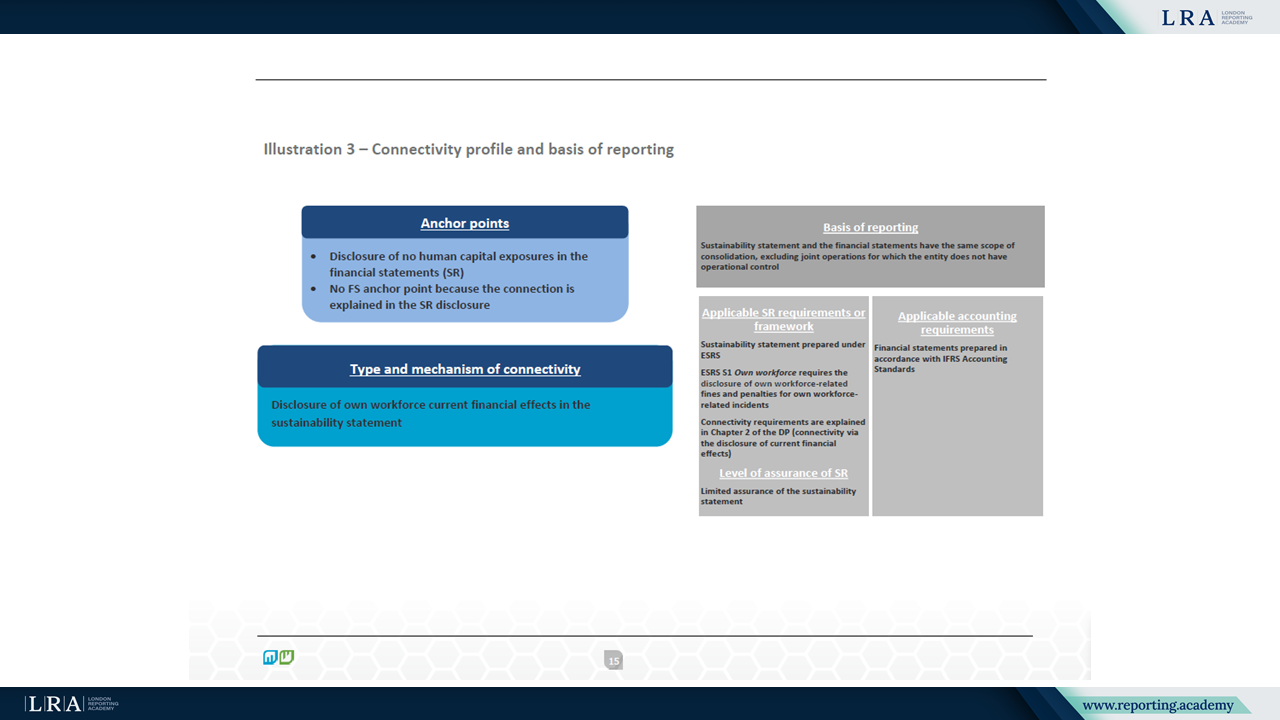

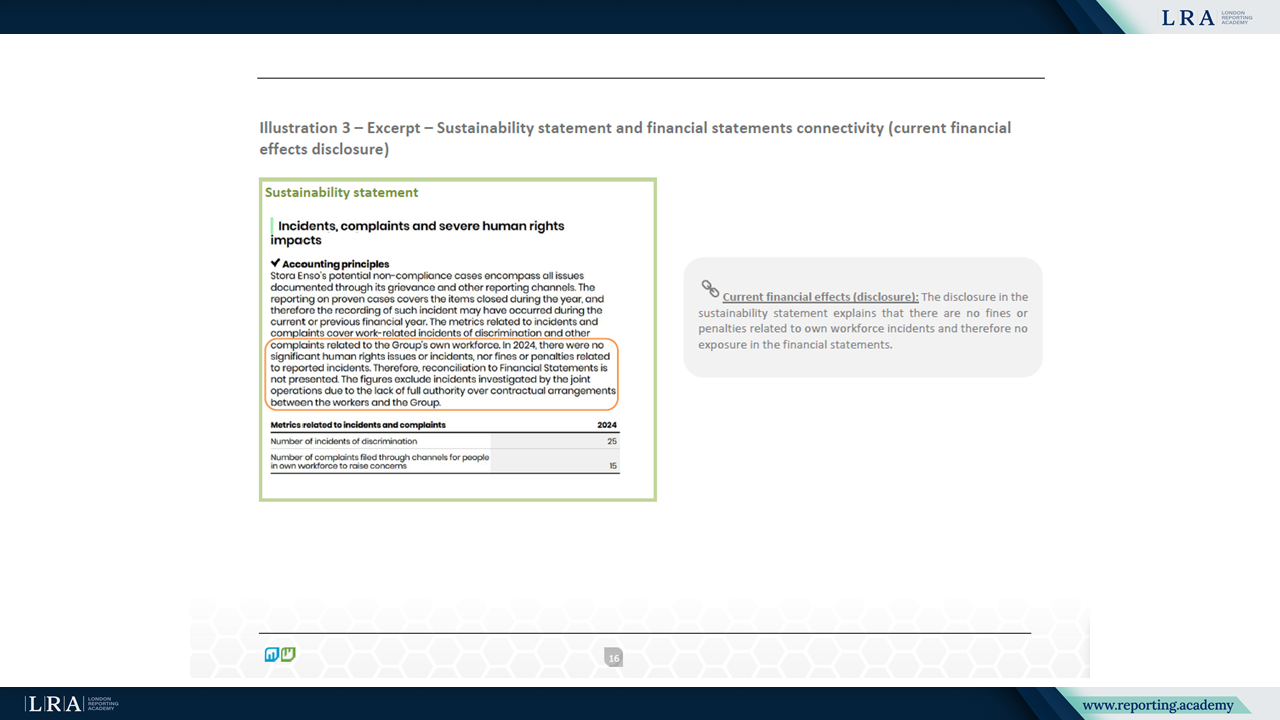

The Supplemental Document complements the Discussion Paper by presenting 17 illustrations drawn from the 2024 annual reports of 15 companies across 9 sectors. The illustrations are based on different reporting frameworks, including ESRS, ISSB Standards and TCFD recommendations and are intended to demonstrate that connectivity is relevant regardless of the underlying reporting framework.

Source: Illustrations of connectivity, EFRAG Connectivity DP - Supplemental Document

Source: Illustrations of connectivity, EFRAG Connectivity DP - Supplemental Document

Source: Illustrations of connectivity, EFRAG Connectivity DP - Supplemental Document

The examples show how anchor points can be used to connect disclosures across sustainability statements, financial statements, management reports, governance reports and risk reports. The topics covered include climate change, energy optimisation, water pollution, own workforce and sustainability-linked financing. EFRAG stresses that the illustrations are not assessments of reporting quality and are not intended to represent best practice or a target reporting model. Instead they demonstrate different types and mechanisms of connectivity as observed in current reporting practice.

Consultation and next steps

EFRAG has opened a public consultation on the Discussion Paper and the Supplemental Document with comments requested by 30 June 2026. The feedback received is expected to inform EFRAG’s future research activities and may contribute to discussions on the further development of corporate reporting requirements at European and international level.

By framing connectivity together with the clarification of report boundaries EFRAG positions the Discussion Paper as a contribution to the ongoing discussion on how financial and sustainability information can be aligned in a coherent manner to enhance transparency and support informed decision-making.