Disclosing Anticipated Financial Effects under ISSB Standards: Clarifying Expectations for Preparers

Anticipated financial effects are a core element of sustainability-related disclosure under the ISSB Standards. As companies prepare to implement IFRS S1 and S2, understanding how to report these forward-looking impacts in a consistent and decision-useful manner has become a central concern for preparers across industries.

In August 2025, the IFRS Foundation issued educational material to support preparers in applying disclosure requirements for anticipated financial effects in accordance with IFRS S1 and IFRS S2. While not a formal part of the ISSB Standards, the document provides practical direction to enhance consistent implementation across jurisdictions and industries. It responds to preparers’ frequent questions on how to articulate the anticipated financial consequences of sustainability-related risks and opportunities, particularly in the climate context.

The guidance follows the issuance of the ISSB’s inaugural standards in June 2023 and complements earlier webcasts released in May 2024. It emphasises how sustainability information should be integrated into general purpose financial reports to meet investor expectations and reinforce strategic transparency.

Defining Anticipated Financial Effects

The term "anticipated financial effects" refers to the expected impact of sustainability-related risks and opportunities on a company’s financial position, financial performance and cash flows over short-, medium- and long-term time horizons. These disclosures are forward-looking in nature and differ from "current financial effects", which relate to impacts already recognised in the reporting period.

Entities are required to define their time horizons and disclose how those definitions have been determined. The Standards specify that companies must provide at least one set of definitions for short-, medium- and long-term perspectives. These may vary by sector, business model or planning cycle.

Importantly, anticipated financial effects must reflect how sustainability risks and opportunities are embedded in financial planning. Examples may include capital investments, shifts in operating cost structures, or potential asset impairments related to climate transition.

Strategic Relevance and Investor Usefulness

Disclosures of anticipated financial effects are part of a broader requirement to explain how sustainability-related risks and opportunities influence a company’s business model, strategy and decision-making. Investors rely on this information to evaluate how such factors may affect future access to finance, cost of capital and enterprise value.

The ISSB stresses the importance of illustrating how anticipated financial effects connect with information in financial statements. This includes identifying specific line items, explaining potential adjustments to asset or liability carrying amounts, and referencing commitments that are not yet reflected due to recognition thresholds.

Disclosures should be structured in a way that supports a coherent narrative. Although ISSB Standards present disclosure requirements in sequence, preparers are not required to follow this order. Instead, they are encouraged to tell a consistent story across sustainability-related disclosures and financial statements, using cross-referencing where appropriate to avoid duplication.

Mechanisms Supporting Practical Implementation

To address challenges in quantifying forward-looking data, the ISSB Standards introduce proportionality mechanisms. These allow preparers to use all reasonable and supportable information available at the reporting date without incurring undue cost or effort. This concept is already familiar from other IFRS Accounting Standards and sets boundaries on the level of estimation required.

Preparers are expected to consider information already used in financial reporting, business operations, strategic planning and risk management. The effort required to obtain additional information should be balanced against its relevance and potential value to investors. The availability of internal resources, skills and analytical tools will inform how far a company can go in producing quantitative estimates.

Where the necessary capabilities do not exist, entities may rely on qualitative information, provided they clearly explain the reasons for omitting quantitative disclosure and identify affected financial statement line items.

Disclosure Reliefs and Limitations

According to the ISSB’s educational material, companies are not required to provide quantitative information about anticipated or current financial effects if the effects are not separately identifiable or if the level of measurement uncertainty is so high that the resulting information would not be useful. These situations are acknowledged as practical limitations, and the guidance clarifies that they are not transitional – they may persist depending on the nature of the risk and the company's internal systems.

Additionally, two exemptions are available. Entities are not required to disclose information that is prohibited by law or regulation. They may also withhold information about sustainability-related opportunities if it is commercially sensitive. In both cases, companies should still provide qualitative context to maintain the overall usefulness of the disclosures.

The ISSB highlights that entities cannot use lack of skills as justification for disclosure omission if they have the resources to acquire or develop the necessary capabilities. Over time, as capacity improves, the expectation is that disclosures will evolve to include more robust and quantified information.

Illustrative Applications Across Industries

The educational material includes illustrative examples to show how the proportionality mechanisms and reliefs apply in practice. These examples cover sectors such as mining, retail, agriculture, construction and information technology.

Source: Disclosing information about anticipated financial effects applying ISSB Standards

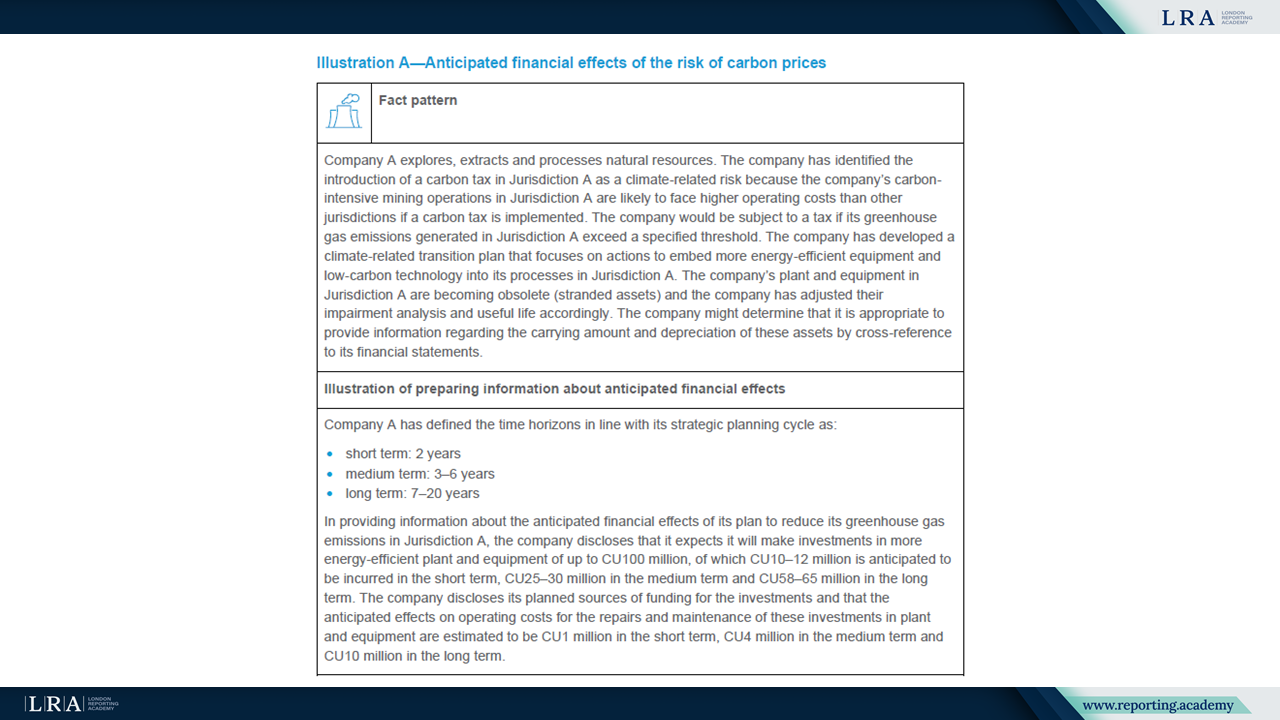

One scenario involves a resource extraction company anticipating carbon pricing impacts. The company discloses planned investments in low-carbon equipment and links these to depreciation charges and asset impairments. Another example shows a retailer quantifying projected increases in flood insurance costs by relying on historical data and internal risk assessments. In a third case, an agricultural firm provides medium-term estimates of rising input costs due to water scarcity, while noting that long-term impacts are too uncertain to quantify.

Other illustrations demonstrate valid use of qualitative-only disclosure when relevant information is not available, or when separating effects from broader economic drivers is not feasible.

Conclusion: Aligning Disclosure Practice with Strategic Intent

Disclosing anticipated financial effects is central to enabling investors to assess a company’s long-term resilience and strategic response to sustainability-related risks and opportunities. The ISSB’s guidance clarifies how preparers can meet this objective in a proportionate and transparent way, even when quantitative estimates are challenging.

Preparers are advised to start with available information, disclose underlying assumptions and provide sufficient narrative to explain expected financial consequences. Where estimates are not possible, qualitative explanations remain essential.

The ISSB does not require predictive precision but expects disclosures to be relevant, reliable and connected to the company’s broader financial reporting. As capabilities grow and data improves, disclosures are expected to become more sophisticated, enhancing investor understanding and supporting efficient capital allocation.