ASEDG: Simplified ESG Disclosures for SMEs in Supply Chains

The ASEAN Simplified ESG Disclosure Guide for SMEs in Supply Chains (ASEDG) sets out a voluntary approach for SMEs to track and disclose ESG information to customers, investors and financiers, including in response to ESG disclosure requirements set by stakeholders such as large companies and financial institutions.

On 6 November 2025 the ASEAN Capital Markets Forum (ACMF) unveiled key deliverables at its ACMF International Conference 2025, hosted by the Securities Commission Malaysia (SC). Alongside the ACMF Action Plan 2026–2030, ACMF launched Version 2 of the ASEAN Simplified ESG Disclosure Guide for SMEs in Supply Chains (ASEDG), stating that it had been refined following public consultation and that it serves to provide guidance to SMEs in preparing ESG disclosures.

Purpose and Intended Users

Within the Guide, the ASEDG is described as a voluntary resource that helps companies decide what ESG disclosures to track and report and to report voluntarily to customers, investors and financiers. The intended user groups are SMEs of all sizes in supply chains and stakeholders such as large companies and financial institutions that set ESG disclosure requirements for SME suppliers or customers. The Guide also notes that SMEs may need to disclose for inclusion in indices or to qualify for incentives where offered.

Scope, Limitations and Responsibility

ASEDG states that it covers ESG indicators to be tracked and disclosed to implement and illustrate good ESG practices, and that it does not cover strategic adoption of sustainability, assessment and mitigation of risks, or identification of business opportunities. The disclaimer notes that the guidance is aligned with international standards but is not exhaustive, and that SMEs are expected to exercise discernment and diligence when applying it to their operations, activities and ESG risk profiles.

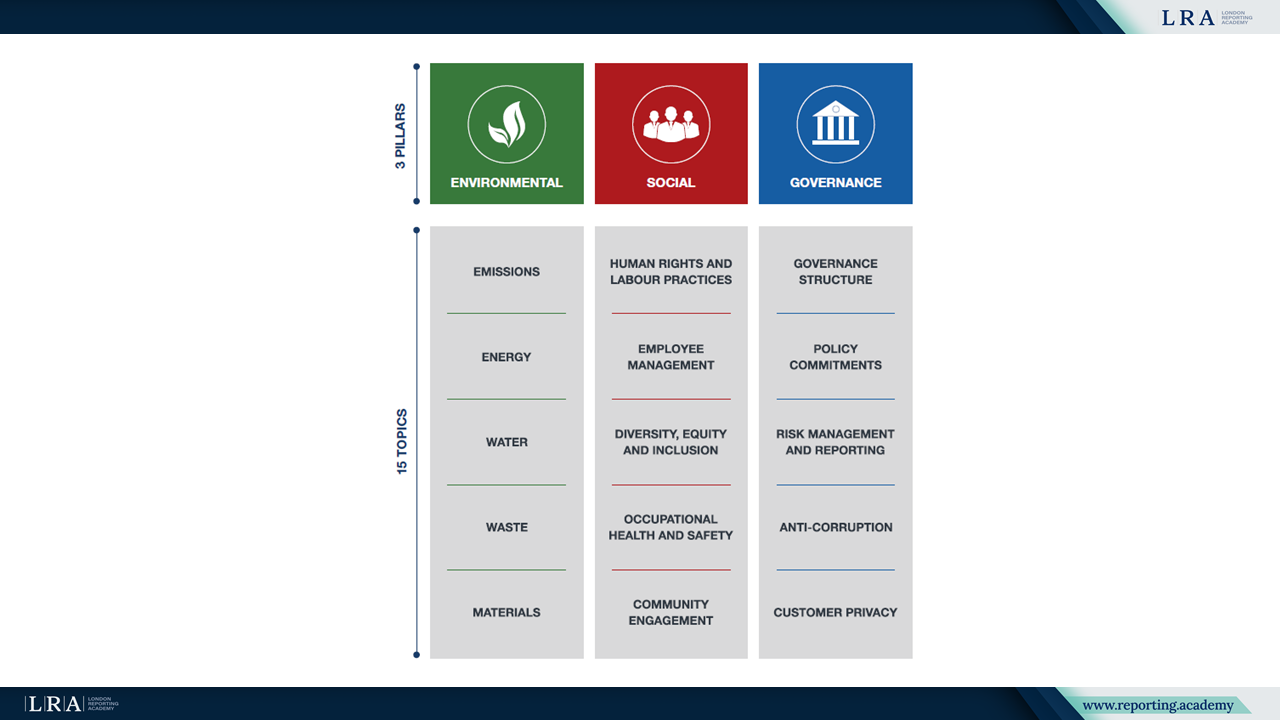

Disclosure Architecture

ASEDG is organised around 15 topics across three pillars, Environmental, Social and Governance. It states that the 38 disclosures are applicable across all industries, with different levels of importance and priority, and encourages companies to determine materiality for relevant topics and associated disclosures.

Source: ASEDG

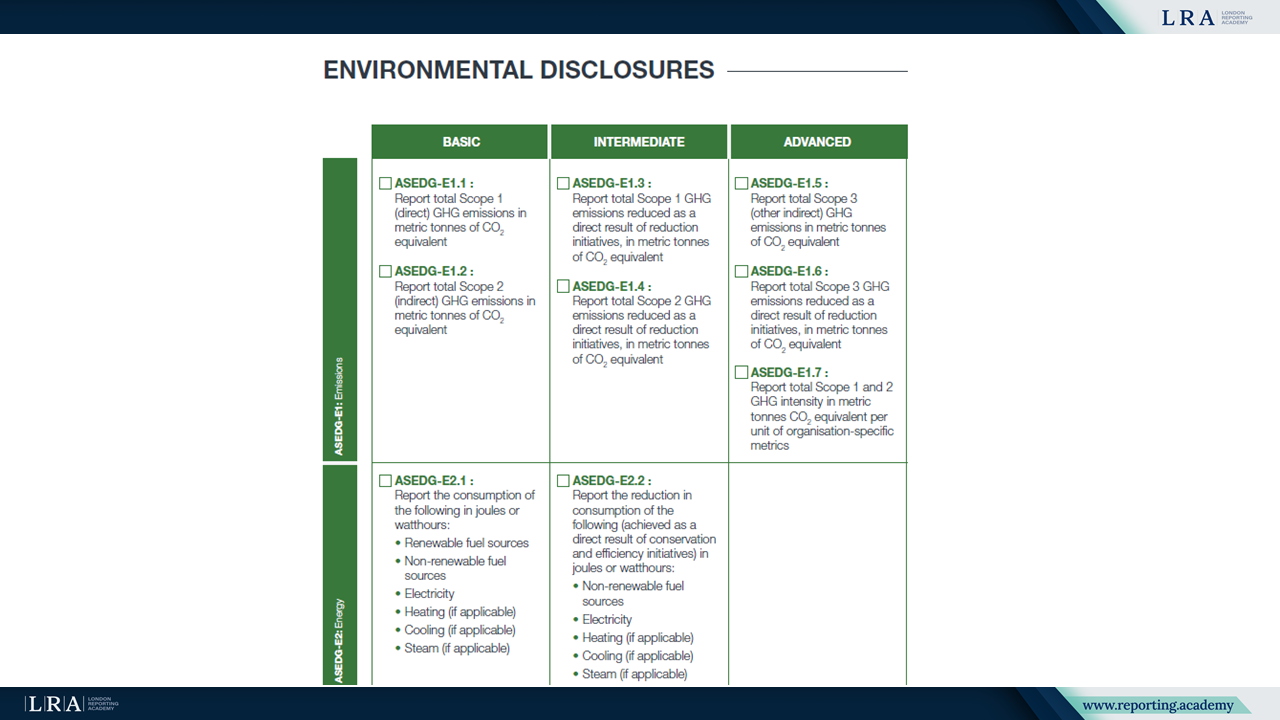

The 38 disclosures are divided into Basic, Intermediate and Advanced categories by topic. As guidance, the Guide describes the Basic disclosures as a starting point, suggests progressing to Intermediate disclosures if an SME has been on its sustainability journey for 1 to 2 years, and suggests progressing to Advanced disclosures if it has been on that journey for 3 to 4 years. It also clarifies that progression through the categories is not correlated to the size of the company, there is no mandatory timeline for disclosures, adoption is voluntary, and disclosures may be updated if stakeholder needs change.

Source: ASEDG

Links to International Standards and Frameworks

ASEDG v2 lists the standards and frameworks it references, including related reporting guidance of ASEAN Member States, IFRS S1 and S2, GRI, CDP and FTSäGood. It also notes that, in addition to the ASEDG, companies are to consider governing laws and regulations relevant to the company.

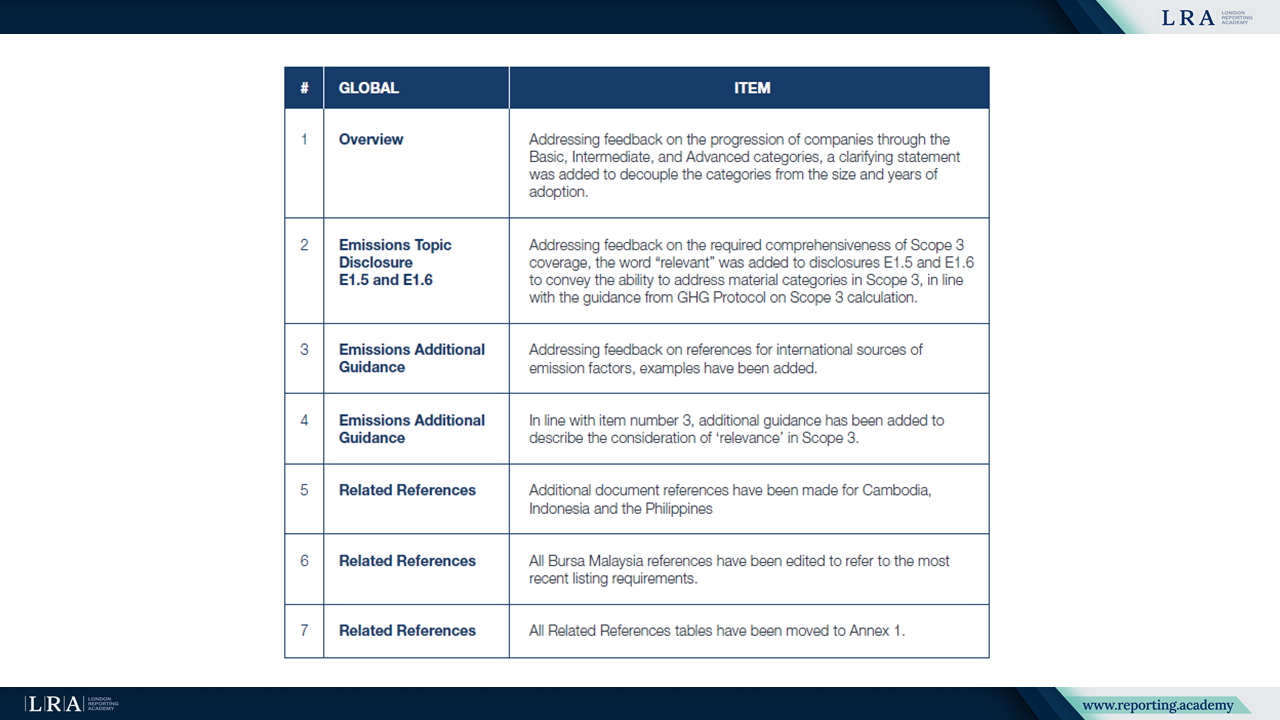

Version 2 Revisions and Emissions Guidance

The foreword states that ASEDG Version 2 has taken effect following a stakeholder consultation process from May to September 2025. Annex 2 summarises revisions, including clarifications that decouple the Basic, Intermediate and Advanced categories from company size and years of adoption. For emissions, Annex 2 notes that the word relevant was added to disclosures E1.5 and E1.6 to convey the ability to address material categories in Scope 3, in line with the guidance of the GHG Protocol on Scope 3 calculation. Annex 2 also records added examples for international sources of emission factors and additional guidance describing the consideration of relevance in Scope 3. Further changes include additional document references for Cambodia, Indonesia and the Philippines, updates to Bursa Malaysia references to reflect the most recent listing requirements, and moving Related References tables to Annex 1.

Source: ANNEX 2: Revisions in version 2.0, ASEDG

Summary

With its topic based structure and tiered disclosure levels, the ASEDG v2 provides a single reference point for SMEs in supply chains and for organisations that request ESG information from them, helping to identify which indicators to track and disclose in response to stakeholder needs. The Guide sets out the disclosures alongside related references and supporting detail in the annexes, including the revisions introduced in Version 2.